Pound Sterling enters the mid-week session holding recent gains which have come on the back of a run of better-than-forecast UK economic statistics

- Pound to Euro exchange rate today: 1.1670, 24 hour best: 1.1680

- Euro to Pound Sterling exchange rate today: 0.8570, 24 hour best: 0.8578

- Pound to Dollar exchange rate today: 1.3181, 24 hour best: 1.3211

Recent data out of the UK economy has been good, and there was more of the same on Tuesday the 24th of August when the CBI has reported that their Industrial Trends survey for August read at -5, a beat on the -9 estimate economists had forecast.

The result ensured the recent gains made by Sterling extended a little further.

While the data would normally be considered second-tier in nature, this month's release was closely watch by markets hungry for signs of just how the UK economy has responded to the EU referendum.

The signs from the CBI are positive in this regard.

Of note, the survey of 505 firms found that export order books reached a two-year high, suggesting that the depreciation of Sterling since the end of last year may be feeding through to stronger overseas demand.

Despite the improvement in exports, total order books were largely unchanged but remained comfortably above the long–run average.

The forward-looking output expectations balance, which typically has a better relationship with the official measure of manufacturing output, rose from +6 to +11.

"It is probably too soon to call an export renaissance. After all, there are still big question marks as to what the future of the UK’s trade relationship with Europe will look like. But given that all of the existing arrangements (including free trade agreements) remain in place until after we actually leave the EU, the weaker pound should provide a much-needed offsetting boost for manufacturers," says Paul Hollingsworth at Capital Economics.

Hollingsworth says the latest survey evidence is another reason to think that the economy should avoid a deep recession. "That said, given its relative importance, it will be up to the services sector to ensure that the recovery maintains some momentum over the coming quarters."

The data helped Sterling maintain the key 1.16 support in GBP/EUR and 1.31 in GBP/USD.

Latest Pound/Euro Exchange Rates

| Live: 1.1703▲ 0%12 Month Best:1.1719 |

*Your Bank's Retail Rate

| 1.1305 - 1.1352 |

**Independent Specialist | 1.1539 - 1.1586 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

The 'Big Squeeze' Drives Pound's Recovery

Heading into the CBI data, Sterling was already being bid higher as a big 'short squeeze' higher in the currency continued.

This is a scenario whereby a market that is betting so heavily in one direction finds it can no longer sustain the move as there are not enough market participants available to enter the market and keep the train moving forward.

The move stalls as a result. Even worse, it can go into reverse as traders are forced out of the market when their stop losses are triggered. This in turn sees the price push even more traders out down the line, ensuring the market moves in GBP's favour.

“Sterling extended its gains versus the euro and U.S. dollar. The U.K. calendar is light this week, which means Brexit headlines could have a greater effect on the pound,” says Kathy Lien at BK Asset Management. “The lack of data has prompted more short covering in the currency.”

IMM statistics - which are considered the most reliable snapshot of how traders are betting - published late on Friday showed that the market is heavily positioned Sterling short, i.e betting on falls.

"The market, positioned short Sterling, prevented additional Sterling selling. EUR/GBP declined to trade currently in the 0.8630 area. GBP/USD rebounded to the 1.31 area," says analyst Piet Lammens with KBC Markets.

However, we would be nervous of suggesting the rally can continue untested as these kinds of moves are technical in nature and not necessarily fundamentally driven.

"The downside potential in the short to medium term still poses a strong risk to the value of the pound and profit taking around the $1.33 level could see any gains made this week quickly eradicated," says Joe Manimbo at Western Union.

The Pound Starts to Regain its Footing

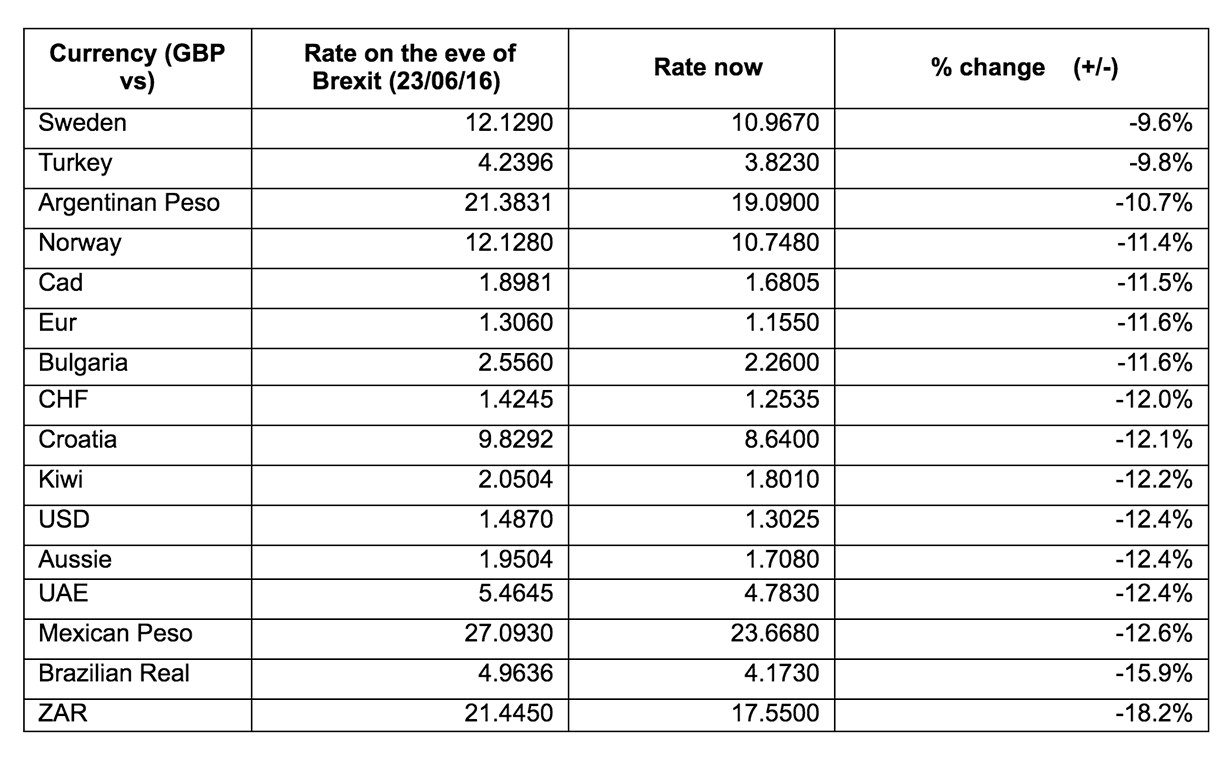

The rally in GBP does however remain limited in the context of the losses the currency has experienced since the Brexit vote:

However, the big theme for us at present is the discussion being had as to whether Sterling finally forming a base from which to mount a more sustained recovery.

“It is important to note that while Sterling trades on the back foot due to the Brexit uncertainty, we are starting to see signs of Sterling regain its footing and some lost territory. Its journey back to the levels of the evening of June 23rd is still distant; however it looks like we have already seen the ‘Brexit Bottom for Sterling’” says Andy Scott, an economist with HiFX.

That said, Scott believes consumers should spend time familiarising themselves with all available options to protect themselves against potential financial losses while also shopping around for the best currency deals and advice.

Some good pointers on the matter can be found in these recent pieces we have published:

- Nordea: British Pound has Bottomed, Better Exchange Rates Against Euro, Dollar Ahead

- Barclays Forecast Undervalued Pound / Euro Rate to Recover to 1.30 by Early 2017

- Lloyds Forecast GBP/EUR Exchange Rate Recovery Through 2017

With regards to the data agenda for Sterling, don't expect much until the new month gets underway.

We have a second revision to Q2 GDP due out later in the week, but Q2 is old news - markets want more insights into the state of the post-Brexit vote economy.

With that in mind, next week's PMI data for August will be closely watched.

US Dollar Gives Up Opening Strength

The USD has meanwhile come off the boil having started the week in formidable fashion.

The Dollar was boosted by further signs that the US Federal Reserve may be looking to raise interest rates at least once in 2016 in the latest installment of the "will they, won't they?" debate.

"It’s all about the Federal Reserve at the start of this week, as markets continue to grapple with comments from various Fed rate setters on when interest rates will next be raised," says Joshua Mahony at IG.

Over the weekend it was the turn of Stanley Fischer who said core inflation was closing in on the central bank’s 2% target.

"That’s given the dollar strength Monday morning, and commodity prices are down as a result. European stocks have started firmer, even after a mixed session in Asia which saw Japanese equities rise and Chinese indices fall," says Mahony.

As a result, Sterling is seeing hefty gains against the commodity complex which includes the South African Rand, Australian, New Zealand and Canadian Dollars.

While Fischer did not comments specifically on the timing of the next Fed rate increase, a number of Fed officials recently have been keen to keep alive the view that the FOMC may tighten policy this year.

Comments from San Francisco Fed President Williams last week suggested that September should “definitely be in play”, while Lockhart indicated that he is not ruling out two rate hikes this year.

Dudley also issued a hawkish viewpoint last week by commenting that jobs gains remains sturdy and the US is moving closer to full employment.

"The market’s assessment of the risk of a Fed rate hike this year remains very measured. The chances of a move in either September or December is seen to be limited and although the implied probably of a move in December is stronger, this still stands at just 51%," says Jane Foley at Rabobank in London.

The dovish expectations of the market with respect to Fed policy are in marked contrast with those held at the start of last year. Back then the market held the view that the Fed would start to tighten policy in June 2015 and move progressively after that.

It is this change in sentiment that has seen the USD fall back, allowing the GBP/USD to form a decent base that appears to have arrested declines.

As Dollar Rises, Oil and Commodities Fall, Hitting AUD, CAD, ZAR

The commodity dollar complex is the big underpreformer in global FX at the present time.

We have seen commodity prices fall, lead by oil, as the USD rises - the US currency is what these commodities are priced in.

Therefore a higher Dollar = more costly commodities = lower currencies for those countries which derive a notable portion of economic growth from commodity exports.

But, the fall in oil prices was partly driven by other factors - China increased exports of refined oil products, Iraq and Nigeria remain defiant about working with OPEC and possibly halting production of oil.

US added oil rigs for an 8th consecutive week. The losses snapped a previous 7 day streak of upward price pressure for oil.

The fall in the likes of CAD and AUD have allowed the British Pound to further cement a base here.