The Bank of England's quantitative easing programme is in full swing with the bond buyback programme likely to keep a lid on Sterling strength.

The Bank of England successfully injected a further £1.169BN into the economy via its quantitative easing programme on Tuesday the 16th August.

The latest stage of the programme saw the Bank snap up long-dated Gilts with £3.123BN being offered to the Bank suggesting the reverse auction was oversubscribed by a multiple of 2.67.

In short, when these events go well the GBP comes under pressure, when the Bank struggles to find sellers, as was the case this time one week ago, Sterling finds relief.

The Tuesday events are notable in that they are aimed at Gilts with maturities of over 15 years - and it appears that pension funds don't part easily with such assets.

On Monday Sterling declined to fresh three year lows against the Euro as the Bank of England successfully purchases £1.17BN worth of government bonds (Gilts) with a maturity set between 3 and 7 years:

- Total offers received: Stg 4,140.8mn

- Total offers accepted: Stg 1,169.8mn

- The auction was therefore 3.54 oversubscribed

As a result, the yields on those Gilts remain near record lows which in turn help ensure funding costs right across the Sterling system remain low.

However, falling yields in turn diminishes currency inflows as global investors opt to seek higher yield elsewhere in the world, thereby placing downward pressure on the UK currency.

Therefore, bond purchases and the success of the multi-billion Pound quantitative easing programme will continue to be closely watched by currency traders.

“While the BoE’s planned QE purchases failed to elicit sufficient willing sellers on only the second day, raising the prospect of implementation challenges, Gilt yields were pushed down to record lows, a sign that the policy for now appears to be achieving the intended result,” says Michael Sawicki at Lloyds Bank.

Latest Pound/Euro Exchange Rates

| Live: 1.1703▲ 0%12 Month Best:1.1719 |

*Your Bank's Retail Rate

| 1.1305 - 1.1352 |

**Independent Specialist | 1.1539 - 1.1586 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

How it Works

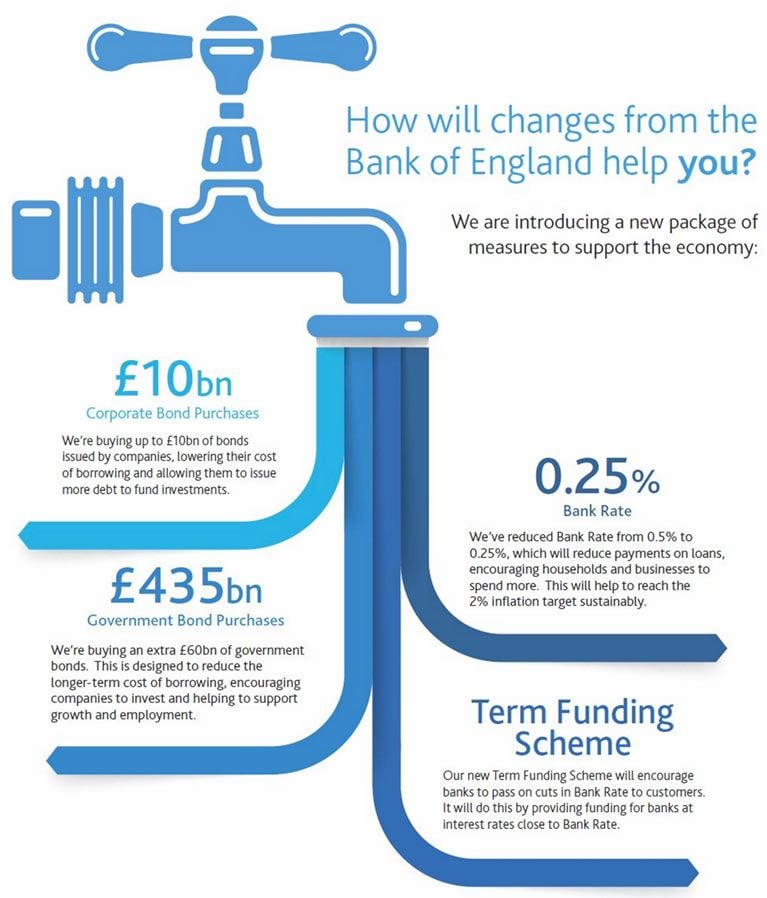

This August the Bank of England announced it would aggressively expand its support to the UK economy through the implementation of a number of measures:

The moves, it is hoped, will force down the cost of borrowing in the economy, thereby stimulating investment.

A strong desire by the likes of pension funds to offload bonds to the government was seen last week when the programme started, and the Pound fell as expected.

Asset Purchase Facility transactions are undertaken by a subsidiary company of the Bank of England – the Bank of England Asset Purchase Facility Fund Limited (BEAPFF).

BEAPFF borrows from the Bank to pay for the assets it purchases (under the Gilts and Corporate Bond Purchases Schemes) and the loans it makes under the Term Funding Scheme.

This loan to BEAPFF appears on the Bank's balance sheet as an asset.

The corresponding liability is the increase in central bank reserves which have been created to fund the loan to BEAPFF.

The increased supply of money to the economy should help stimulate increased activity as the cost of borrowing is expected to fall.

The problem for those wanting a stronger Sterling is that the extra supply of currency results in a dilution of value in the currency on a unit basis.

Therefore, we would not expect a sustained appreciation in the Pound exchange rate complex until the taps are switched off.

Beware that Short-Squeeze Higher in Sterling

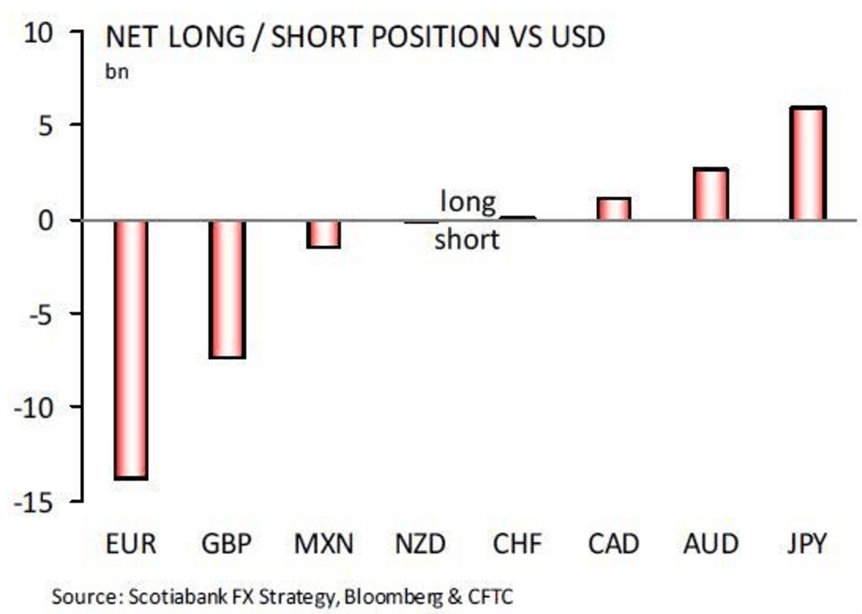

FX market data from the CFTC shows a record number of bets being made against Pound Sterling.

Short positions are now shown to be at a record level having been building for six consecutive weeks now.

The net short GBP position stands at a notable $7.3BN, sellers now outnumber buyers by a ratio of 3.5:1.

“Everyone is bearish GBP, and I get it,” says Aurelija Augulyte, analyst with Nordea Bank. “Short term, global equities falling is GBP negative. And there is no particular reason to expect a miraculous UK recovery.”

On this basis, Augulyte warns that the prospect of a sharp squeeze higher in the Pound is becoming increasingly likely.

“But every single person I talk to is GBP bearish. Every. So I am afraid, we end up on the road of GBP-short squeezes like during the European crisis, should e.g. UK data turn out NOT as ugly, the BoE does NOT cut rates in August, oil does NOT collapse like in 2015 or 2014…” notes Augulyte.

It is for this reason that should this week’s data prove better-than-forecast, we could see GBP rally.

Likewise, should the Bank's bond-buying programme also hit the buffers, GBP could rally, and rally quite sharply.