The GBP is likely to struggle as deteriorating data suggests to markets that the Bank of England will have to cut interest rates on Thursday

Pound Sterling was seen trading in mixed fashion a mere two days ahead of what promises to be an incredibly important Bank of England event on Thursday the 4th August.

Four times a year the Bank of England releases its Quarterly Inflation Report, where inflation and growth forecasts are updated while the Bank typically uses the event to communicate and explain major changes in monetary policy.

OIS markets are presently seen quoting a near-100% chance of a 0.25% cut to the interest rate.

"Despite the near-guarantee of a rate cut sterling has been remarkably lateral in its movements recently; since mid-July it has reliably bounced away from 1.30 against the dollar, tending to hover somewhere between 1.31 and 1.32," notes Connor Campbell, a commentator at spread betting company Spreadex.

However, Campbell warns that the strain of the next few days, with this morning’s construction PMI and tomorrow’s services reading all leading to the main event on Thursday, could see it drop out of that trading bracket.

Latest Pound/Euro Exchange Rates

| Live: 1.1673▼ -0.02%12 Month Best:1.1828 |

*Your Bank's Retail Rate

| 1.1276 - 1.1323 |

**Independent Specialist | 1.151 - 1.1556 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

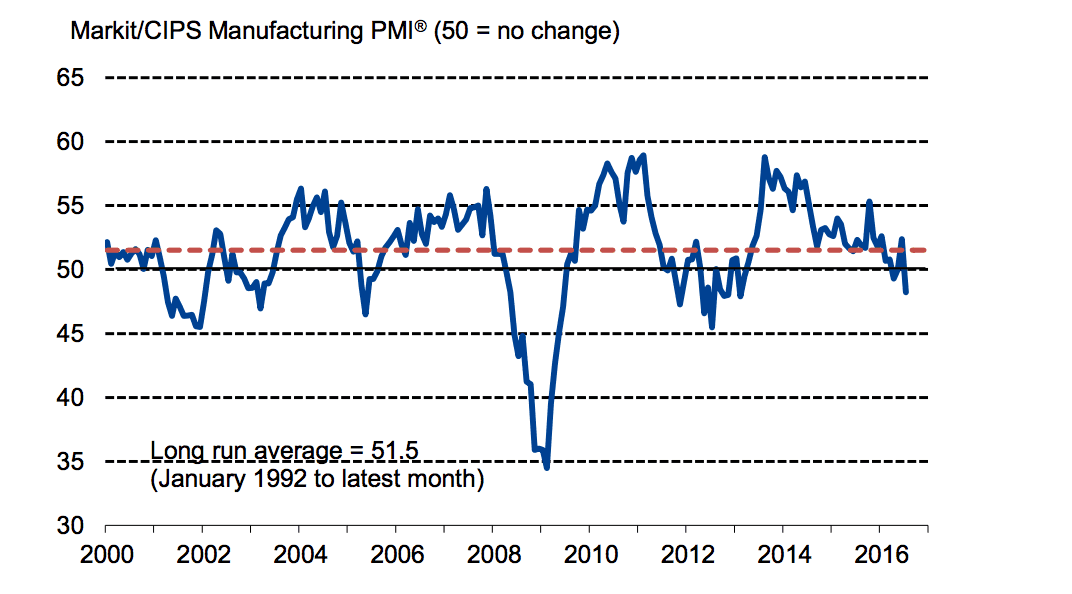

Manufacturing Sector Contracts

The GBP was seen lower right across the board following the release of July Manufacturing PMI data which missed analyst expectations by reading at 48.2.

Markets had forecast a reading of 49.1 to be delivered by the survey's compilers CIPS and IHS Markit.

The miss comes as the manufacturing sector sufffers a fall to its lowest point since early 2013 amidst signs levels of production and incoming new orders have slipped on increased business uncertainty, predictably stemming from the EU referendum outcome.

“Though these falls were not as marked as those seen during the Great Recession in 2007-2008, the drop was harsher than expected. The overall index was at its lowest since February 2013 and lower than reported by the recent flash PMI, which measured the effect of continuing uncertainty and the immediate impact of the EU referendum on the UK economy," says David Noble, Group Chief Executive Officer at the Chartered Institute of Procurement and Supply.

Not even the weaker GBP exchange rate could aid the sector.

However, the level of incoming new export orders in the UK manufacturing sector was seen to have risen for the second successive month in July.

"Admittedly, the new export orders balance only fell 0.3 points from June, suggesting that the boost to competitiveness from the fall in the pound is already providing some support to manufacturers," says Scott Bowman, UK Economist at Capital Economics.

This suggests there is some downside protection being offered by the weakened exchange rate that could grow in influence over coming months as it tends to have a delayed effect on activity.

The PMI data, released by Markit and the CIPS, is regarded as one of the more accurate sources of flash data - i.e this is data that is more timely than the more accurate figures from the Office for National Statistics which tends to have a delay.

It therefore gives a good snapshot of how businesses have been faring over recent weeks.

Traders will be interested in finding out the degree to which the shock of the Brexit vote has translated into negative business activity as this could well influence the all-important Bank of England policy decision due out on Thursday the 4th.

"The overall negative tone of the survey reinforces the case for a monetary loosening on at Thursday’s MPC meeting," says Bowman.

Technical Snapshot for GBP vs EUR and USD

- Sterling-Dollar

The GBP/USD pair continues consolidating in an interim 1.30-1.35 range as USD selling in the aftermath of the weak US GDP release triggered a rally to above 1.33.

Resistance remains at 1.3315, with a break above here opening up a move towards highs at 1.35.

"Given that a 25bp cut is already fully “priced-in” and CFTC suggest GBP shorts are extreme, disappointment from the BoE could see a re-test and possible break of that area. To trigger bearish momentum, support at 1.3060 needs to be broken. If that occurs, the move is likely to accelerate, with 1.2945 and 1.2798 providing further support," notes Robin Wilkin, a technical strategist with Lloyds Bank.

- Euro-Sterling

EURGBP briefly broke above its interim range high at 0.8450, printing a high of 0.8478, but has subsequently retreated.

"Short-term technical studies suggest that further sideways trading is most likely. On the day, congestion and Fib resistance are at 0.8480-0.8500," says Wilkin.

Wilkin believes that a break here could initiate a gradual rally towards recent range highs at 0.8627.

Intra-day, support should be found at 0.8420-0.8390, followed by 0.8360/40. Important Fib and congestion support lies below there at 0.8250/00.

The Euro was little changed Monday, though below five-week peaks notched Friday against its U.S. counterpart.

The Euro has suddenly found a bit more room to the upside in the wake of lackluster U.S. growth data Friday that reduced already low odds of the Fed bumping lending rates higher in coming months.

Europe’s weak fundamentals suggest meaningful gains could continue to elude the euro.

Moreover, upside for EURUSD could get undercut if this week’s fresh look at U.S. consumer spending, inflation and employment suggest the world’s largest economy is starting to accelerate from its soft patch.

Uncertainty as to Just How Bad the UK Economic Slow-Down is

Initial post-vote flash PMI data showed the economy had in fact slowed down dramatically, these observations were echoed by other surveyors who noted a sharp downturn in confidence in both businesses and consumers.

This has lead many institutional analysts to forecast recession through the second half of 2016.

However, subsequent confidence data have shown that confidence has started picking up amongst businesses once more as they realise Britain hasn’t imploded.

The Lloyds Bank Business Barometer showed business confidence had risen 23 points in July, while a similar reading from the ICAEW showed that their Index fell drastically after the EU Referendum but confidence has crept up since that point as businesses take stock.

The ICAEW findings are of particular interest as it was noted that, “exports are expected to improve, albeit modestly, due to the falling pound and businesses expect domestic sales to be weaker.”

Could the weaker Pound play a role in delivering better-than-forecast manufacturing PMI statistics on August 1st?

If so then we could well see the British Pound catch a bid as markets anciticpate such an outcome could play into a pared back policy response at the Bank of England on Thursday.

Some analysts have argued that the 25 basis point cut that is expected by markets may not actually happen were the Bank to be data dependent.

If the Bank believe that the initial shock of the Brexit vote would be followed by a business-as-usual approach, then the Bank could well stay on hold.

This would shock the Pound Sterling higher.

However, others warn that regardless of the data, the Bank of England will be intent on taking out insurance with premeditative action.

"We don't yet know precisely how much the UK's Brexit vote has hurt demand and we won't know for probably many months yet. Hard data for July will be available only by late August and a first pass of 3Q GDP not until late October. That first pass will have nothing to say about business investment or household saving behaviour. In our view, the BoE cannot wait that long," says Robert Wood at Bank of America Merrill Lynch Global Research.

However, Wood also acknowledges that the effect of cutting rates and boosting quantitative easing are negligible saying both policy channels are impaired.

"With interest rates close to zero along much of the curve there is limited room for monetary policy to help. Moreover, unlike the financial crisis, the problem this time round is one of credit demand rather than supply.

"The BoE has room to cut its base rate a little. Banks are better capitalised so the BoE does not believe it is currently at the zero lower bound. But a rate cut will help only a little. It may not be fully passed through to borrowers, or banks appetite to lend could be harmed."

Indeed, other countries that have pushed rates to or below zero have seen negative effects.

However there is likely to be some passthrough, meaning rate cuts will help a little suggests Wood.

While there are undoubted problems with rate cuts Bank of America think those issues are larger for Quantitative Easing. Many of the channels through which QE works are likely to be blocked at present.

Confidence effects from QE are hard to detect, market liquidity is not impaired currently, and there is no evidence that QE boosts bank lending argues Wood and his team.

"In 2009 QE could shift the front end of the curve by signalling to the market that Bank rate would not be raised in the near future. But there is little room for those effects now that the market is already pricing front end rates to remain close to zero for years," says Wood.