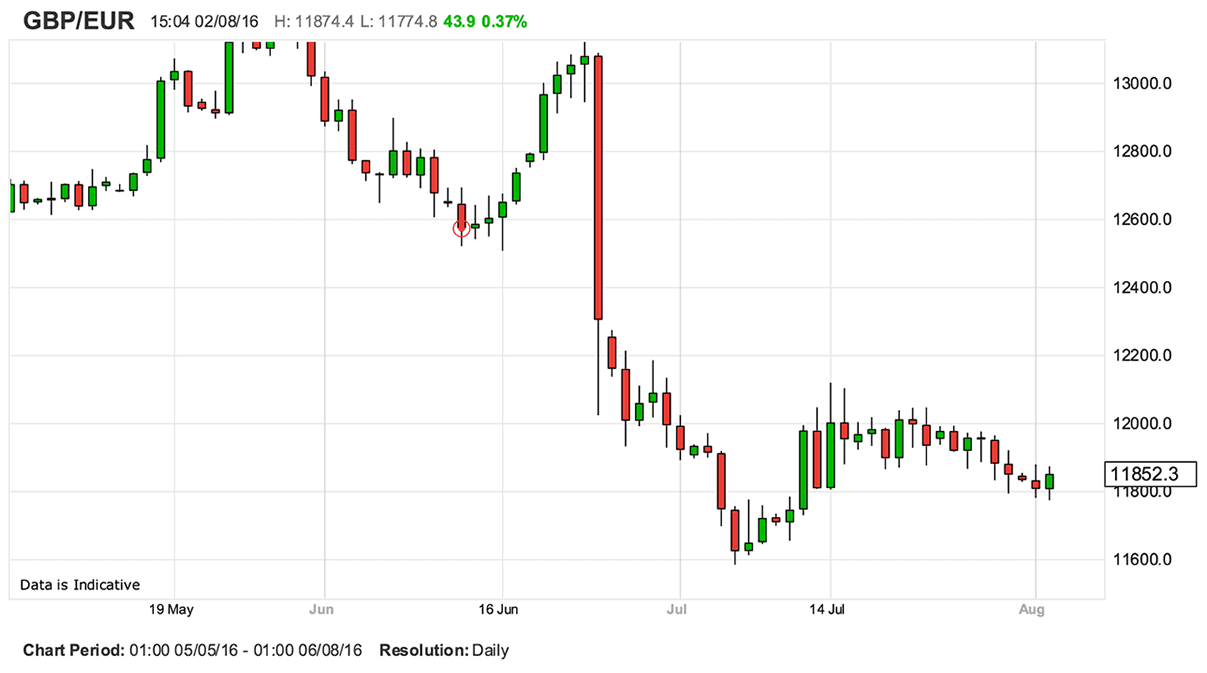

Pound Sterling has moved notably higher against the Euro in a move that will surprise many when we consider the path ahead is strewn with risks.

- Pound to Euro exchange rate today: 1.1844, 0.30% higher on the day's opening level

- Euro to Pound Sterling exchange rate today: 0.8444

- Strategists target levels ranging from 1.1592 through to 1.17

- Underwhelming data confirms an interest rate rise at the Bank of England is likely on Thursday

- Big upside risks to GBP were the Bank to underwhelm

The UK currency has bounced off a key support level against the Euro in a move that confirms the pair is likely to track a sideways move into the Bank of England's Thursday policy event.

With no obvious triggers to the Pound's strong performance, a mere two days before a massive, high-risk event, we are left with conclusion that the currency is being driven higher by a classic short-covering move.

Short-covering refers to the process whereby markets are so heavily invested in a single direction that the trade becomes prone to a strong reversal.

If the majority of the market is selling Sterling, a bout of Sterling strength can quickly force traders to exit the market as their protective stop-loss orders are triggered.

This increases demand for the Pound, which in turn drives the exchange rate higher, in turn taking out more traders.

In essence this is a 'wildfire effect' that is not necessarily indicative of a fundamental shift in fortunes towards the currency.

The move higher can also be explained by the structure of the market, evident in the charts.

GBP/EUR had fallen below 1.18 at one stage, but subsequent buying action suggests to us that markets would be comfortable taking on exposure to the unit between the 1.18-1.20 levels.

This suggests upside could well extend towards, but not above, 1.20 in the lead up to the policy meeting.

Clues to the immediate outlook can be found in the daily chart which shows the €1.18 has been tested four times over the past month, and on all occassions Sterling closed above this point:

This tells us there is good demand for Sterling in this vicinity.

However, the period of consolidation could well be symptomatic of a market that is coiling like a spring and we would expect the outcome of the Thursday policy meeting to unleash the pent up energy.

Which direction would a potential break take?

Our studies of the GBP/EUR chart reveals a pair which is in the final stages of a down-cycle which started at the late May highs.

With the down-cycle yet to complete those with an interest in GBP/EUR should be prepared for further losses in value.

Analyst Karen Jones, at Commerzbank, sees the move down from the May highs as an Elliot Wave, which is a type of market cycle.

Elliot Waves are composed of five smaller waves. The most recent sub-wave was a wave 4 which ended in the formation of last week’s triangle pattern.

The pair is currently breaking out of a triangle in a probable final thrust lower - an Elliot Wave 5.

This final move down will probably reach the 1.16 lows eventually, however, a closer target is 1.17.

Others are a little more bearish on GBP/EUR's prospects.

"On the day, congestion and Fibonaci resistance are at 1.1792-1.1765. A break here could initiate a gradual decline towards recent range lows at 1.1592. Intra-day, resistance should be found at 1.1876-1.1919, followed by 1.1961/1.1990. Important Fib and congestion resistance lies above there at 1.2121," notes Robin Wilkin, a technical strategist with Lloyds Bank.

Latest Pound/Euro Exchange Rates

| Live: 1.1674▼ -0.01%12 Month Best:1.1828 |

*Your Bank's Retail Rate

| 1.1277 - 1.1324 |

**Independent Specialist | 1.1511 - 1.1557 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

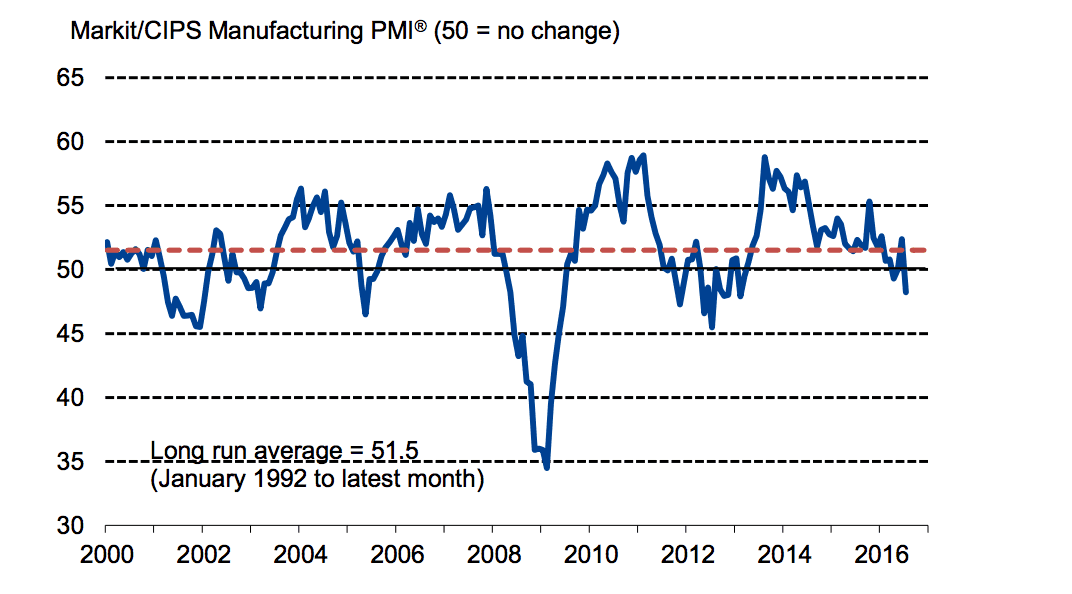

Soft Data Points to an Interest Rate Cut

Sterling slipped a quarter of a percent against the Euro in the wake of the release of Manufacturing PMI figures for July from IHS Markit and the CIPS, released on the 1st of August.

Data showed the sector slipped into contraction with the release of a reading of 48.2, analysts had forecast 49.1.

"Levels of production and incoming new orders both contracted, as the impact of increased business uncertainty on the domestic market offset an exchange rate supported increase in new export business," says a report from IHS Markit on the matter.

The decline in production was the steepest since October 2012:

However, there is a chance that a weaker Sterling could provide some support to manufacturing going forward.

"Admittedly, the new export orders balance only fell 0.3 points from June, suggesting that the boost to competitiveness from the fall in the pound is already providing some support to manufacturers," says Scott Bowman at Capital Economics.

Nevertheless, "the overall negative tone of the survey reinforces the case for a monetary loosening on at Thursday’s MPC meeting," says Bowman.

Indeed, the data could well set the tone for GBP/EUR over the course of coming days and weeks.

Sterling could be set to devalue further when the Bank of England (BoE) unveil a host of monetary easing measures at its Thursday August 4 meeting, designed to help support the economy in its post-Brexit bad-patch.

An interest rate cut of 0.25% is priced at 100% by money markets while questions exist as to whether the Bank may go further.

Questions also exist as to whether the quantitative easing programme will be broadened.

"With the OIS market currently factoring in a 100% probability of a rate cut on Thursday, it is clear that the base case scenario is for further easing this week. With the UK now only 50 basis points above zero and a governor who has publicly denounced negative rates, it seems a matter of time before the QE bazooka comes out once more," says Josh Mahony at IG in London.

The Big Risk: Beware no Action at the Bank of England

We even hear some analysts warning that the Bank may opt to sit on the sidelines for a while longer.

This would unquestionably be a positive for GBP which has sunk over recent weeks in anticipation of some kind of action being announced.

Ultimately, we would suggest to those with outstanding FX payments that they are protected agaisnt downside moves as the balance of risks are to the downside - i.e any downside moves will likely outweigh any upside moves.

The euro, in contrast, is likely to retain its positive tone in the absence oftier-one data releases on the economic calendar for the currency.

The most important release will be the Economic Bulletin from the European Central Bank (ECB), which will provide a further insight into how the ECB views current economic conditions.

The euro was supported after the ECB rate meeting last Thursday revealed policymakers cautious of using more stimulus as the outlook remained balanced, and financial markets had righted themselves after the brief leeward yaw following Brexit.

The single currency was also supported by stronger-than-expected inflation data for June, which came out marginally higher than the 0.1% forecast - at 0.2%.

It may well be the case that the ECB will not feel it is necessary to increase stimulus measures at its next meeting in September.

Nevertheless, some analysts are still clinging to expectations the central bank will expand its policy measures in September despite the encouraging data.

Nordea bank’s Jan Von Gerich, for example, said the data was, "not good enough” to preclude more action from the ECB:

“Euro-area GDP and inflation numbers could have looked much worse. However, continued growth and another small uptick inflation are not enough to convince the central bank that it is doing its job well enough. The more uncertain growth outlook, falling commodity prices and too low inflation still point towards more stimulus.”