The pound’s outlook will ultimately rest with whether or not the UK can continue convincing investors to keep plugging the hole in the UK’s bank account with the world.

- Current account deficit to be revealead at £32.6BN, far greater than the forecast £27.1BN

- Huge uncertainties about the ability to fund the UK’s current account deficit should keep GBP under pressure

Why are banks like UBS and HSBC forecasting the euro and pound to hit an exchange rate at parity on the event of a Brexit?

Because of the country’s current account deficit; which has on Thursday June 30th been revealed as standing at £32.6BN in the first quarter of 2016.

Worryingly the previous quarter's reading was updated to show an even larger gap at £34BN.

The current account is one of two components that make up the Balance of Payments (BoP) - the BoP is best described as the country’s bank account with the rest of the world.

The value of the BoP depends on:

1) how much the UK earns from the export of goods and services (current account) and

2) how much it is investing in other countries, and how much foreign investors are investing in the UK (financial account).

The current and financial accounts are therefore counterparts.

A country that imports more than it exports naturally puts pressure on its its current account via running a negative trade balance.

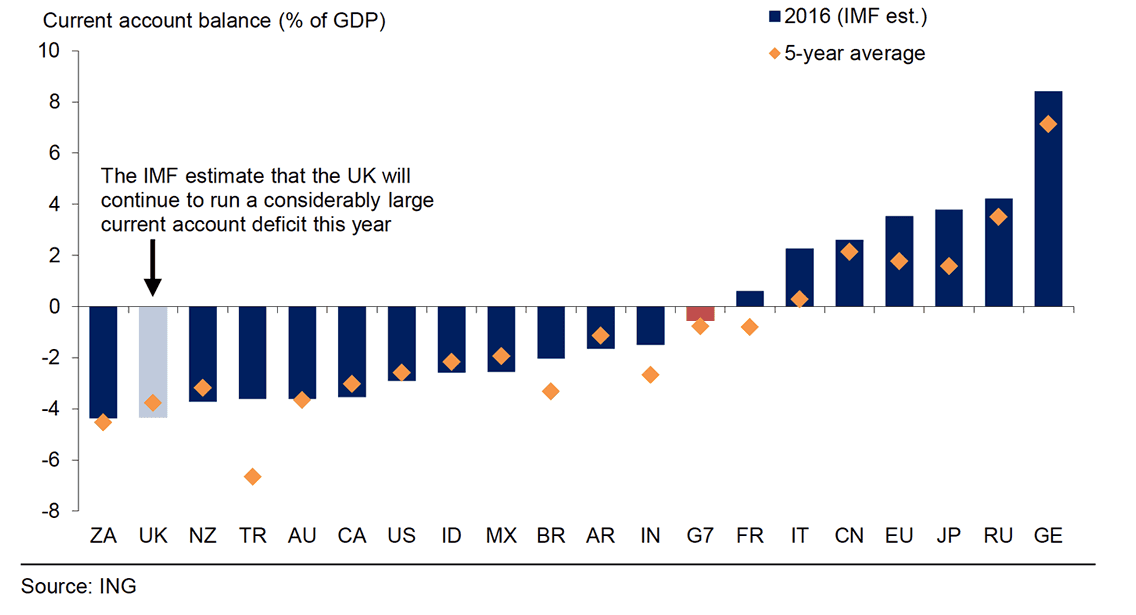

The UK’s current account is overdrawn - it is in deficit - to the tune of 7% of national GDP. It is at a record high.

A current account in deficit betrays a country that is spending more than it is earning on the global marketplace, it therefore has a higher demand for foreign currency.

Basic supply and demand dynamics state that rising demand pushes up prices - a greater demand for foreign exchange therefore pushes up the price of the UK’s partner country’s currency, at the expense of the pound.

Latest Pound/Euro Exchange Rates

| Live: 1.1676▲ + 0.02%12 Month Best:1.1701 |

*Your Bank's Retail Rate

| 1.1279 - 1.1326 |

**Independent Specialist | 1.1513 - 1.1559 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

BUT - as we said, the pound is not exclusively driven by the current account, there is also the financial account which must balance out the deficit in the current account.

Because the pound has for a long time been relatively stable this tells us that the foreign investors are funding the current account deficit via the financial account.

The financial account is therefore key to the pound's outlook and must keep on growing as the corresponding hole in the current account keeps on growing.

Sterling is therefore propped up by foreign exchange inflows from global investors seeking out the UK’s vast array of investment opportunities.

What would happen were that inflow of foreign exchange from investors to dry up, say in the case of Brexit?

“When a country runs a current account deficit, it is building up liabilities to the rest of the world that are financed by flows in the financial account,” point out Atish Ghosh and Uma Ramakrishnan at the IMF in a paper addressing the potential problems associated with a trade deficit.

The two authors warn that should the inflows dry, a big downward shock to both the country's economy and currency are in order.

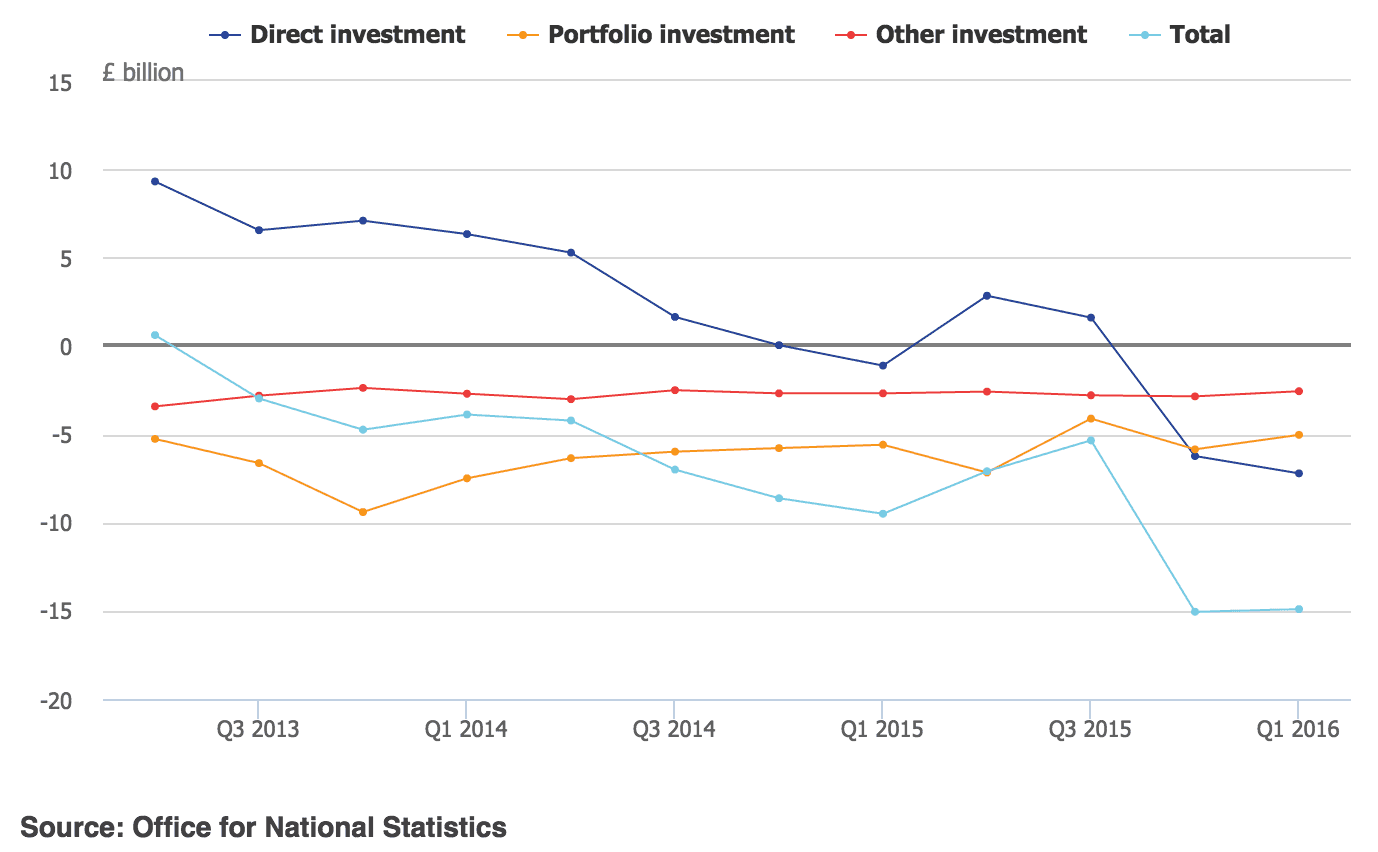

The latest data from the Office for National Statistics show direct investment into the UK has been in decline since 2013:

The exchange rate is losing an important source of support and it will therefore need to adjust lower.

“Huge uncertainties about the ability to fund the UK’s current account deficit should keep GBP under pressure particularly through 3Q16 and probably into 4Q16 as well,” says Chris Turner at ING.

A falling British pound is not necessarily a bad thing, as basic economic theory would suggest that a lower exchange rate encourages the purchase of more British goods, helping the UK to start improving its trade balance with the world once more.

Thus, the UK could fund its current account deficit by an organic improvement in our trading position.

What is problematic though is the speed at which the move could happen; too fast and the economy is destabilised. It will take years to build up our export industry to the level that it can prop up the currency.

S&P Cut UK Ratings as they Worry About the Current Account

The current account deficit is a big deal for ratings agencies like Fitch, Standard and Poors and Moody’s.

It is their job to communicate to investors what products are safe and will continue to offer a good return.

The UK has been hit by a confidence-sapping sovereign debt rating downgrade by S&P following the decision by the electorate to quit the European Union.

What ratings agencies say about government bonds matters - if they are graded highly then foreign investors will continue to pump money into the UK to take advantage of a safe source of return.

This is why the UK manages to run a surplus on its financial account.

Following the Brexit result and subsequent downgrade, S&P expressed concerns with regards to the deterioration in external financing conditions.

“With the current account in what can only be described as the danger zone the appetite of external investors for UK paper will remain crucial over the medium run. The need to attract foreign investment, to fund the current account shortfall, remains the UK’s major Achilles heel,” says Jeremy Stretch at CIBC.

Fitch also downgraded the UK’s credit from AA+ to AA, saying:

"Fitch believes that uncertainty following the referendum outcome will induce an abrupt slowdown in short-term GDP growth, as businesses defer investment and consider changes to the legal and regulatory environment," the agency said in a statement.

"Medium-term growth will also likely be weaker due to less favourable terms for exports to the EU, lower immigration and a reduction in foreign direct investment. An adjustment in the value of sterling and changes in the business environment could also affect growth."

The Pound Could Fall to Parity Against the Euro as a Result of the Current Account Deficit

As mentioned, for foreign exchange forecasters, Brexit is a big deal for the current account, the financial account and therefore for the pound.

HSBC are amongst those investment banks who warn that the pound could par the euro on Brexit owing to the UK’s chronic current account deficit.

HSBC say Brexit raises questions over the future health of UK export growth, not least for financial service exports.

HSBC’s David Bloom says the UK can ill afford any additional widening of the deficit

“At the same time as markets would fear a wider current account deficit, there would be questions over its funding,” says Bloom.

HSBC point out that amongst the ten worst-performing currencies of last year there are only two countries with worse current account deficits than the UK (Turkey and Colombia) and only one country with a worse fiscal balance (Brazil).

“These structural shortcomings have been ignored by the FX market when it was obsessed with the interest rate outlook. Brexit would bring the twin deficits to the centre of the market’s thinking,” says Bloom.

UBS also warn of the pound hitting a 1:1 exchange rate against the euro on Brexit thanks to the current account.

“The currency could bear the brunt of the adjustment if markets focus even more on the imbalance. A range of outcomes is possible, but one risk is that GBP could then depreciate by a cumulative 30% on a trade-weighted basis,” says Themos Fiotakis, Strategist at UBS.

UBS say it is a “reasonable assumption” that the GBP could par the EUR on Brexit.

Don’t Rely on a Boost in Exports to Patch the Hole

As mentioned, the one positive to come out of a depreciating currency is the the boost to competitiveness of UK goods on the global market.

When exchange rates fall, prices fall for foreign buyers and they buy more goods.

However, this may take a while.

“While the cheapening in the currency may ultimately prove to benefit trade prospects, that is far from certain, at least in the short term. What is clearer is that the near term slide in Sterling will negatively impact the trade shortfall and hence the current account deficit,” says CIBC’s Jeremy Stretch.

As a result there is still the chance that the pound has some way to go before the economy can reap the benefits of the fall in value of the currency, which in turn starts to strengthen again.

“Despite the recent stabilisation in GBP we cannot downplay ongoing political and macro-economic uncertainty detailing the risk of Sterling testing further fresh 31 year lows, key support comes in at 1.3040,” says Stretch.

HSBC also point out that while a falling rate of exchange could aid UK exports, the nature of the UK’s trade relationship with Europe may be in doubt, ensuring positives are overshadowed.

Meanwhile, The Eurozone Runs a Current Account Surplus

With regards to the pound / euro exchange rate, it must be noted that the Eurozone has a surplus on its current account i.e it is a net exporter and its exchange rate is not as exposed to falling investor inflows as is the case with Sterling.

“EUR appears to be finding better support via the euro zone’s EUR30bn current account surplus and flows out of sterling,” say Citigroup in a recent research brief to clients.

The euro is therefore forecast to maintain a position of strength going forward based on the large current account surplus the Eurozone maintains, largely thanks to German exports.

This is why the pound will struggle over coming months, and even years, against the euro unless confidence amongst foreign investors can be maintained.

Of course, Eurozone policy makers will desperately try to keep their exchange rate from strengthening too much, lest they lose their export advantage.

That is why the euro will face headwinds from the ECB which may try and contain the currency through further interest rate cuts and quantitative easing.

Indeed, ECB President Draghi recently warned that if the UK goes into recession, the effects would be immediate on the Eurozone and that banking vulnerabilities loom large and need to be addressed now.

Take this as a sign that the ECB will act and put in place measures aimed at devaluing the euro at a future date.

However, even this is unlikely to keep the euro low for long as the ECB is seeing diminishing returns on its interventions.

The next release of UK balance of payment data is out on the 30th of June.

The current account deficit is forecast to read at 26BN pounds.