Two prominent research institutions have reiterated their view that the British pound is too expensive owing to the UK’s continued inability to export more.

The British pound may rally on the outcome of a Remain victory to the EU referendum, but ultimately the move could prove fleeting.

This is according to two prominent research institutions - Morgan Stanley and Capital Economics.

“In our opinion, GBP is overvalued as GBP-supportive interest rate and yield differentials are inadequate to help to fund the UK’s 7% GDP current account deficit,” say Morgan Stanley in a brief to clients.

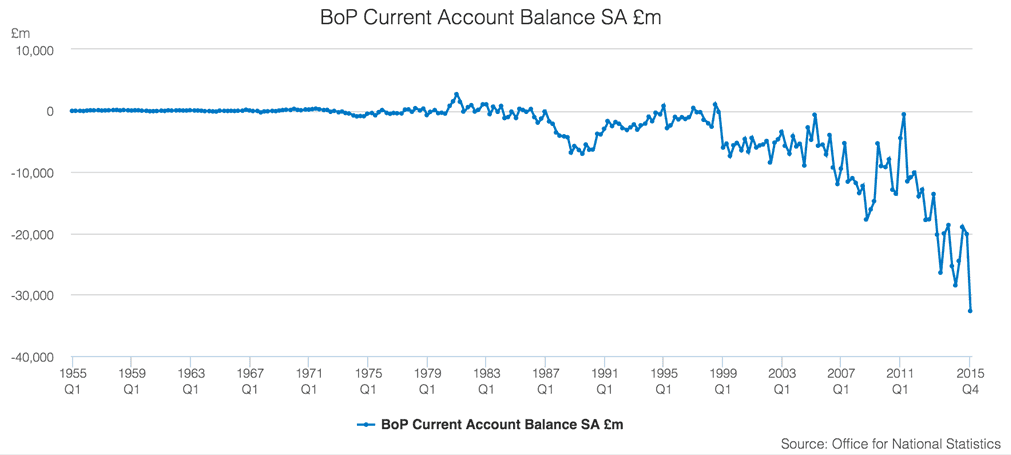

The current account deficit has been a concern for many economists who have been trying to forecast the value of the pound.

Typically an exchange rate between two countries is set according to the trade relations between them.

An importer would have demand for the currency of the exporting country - and if we look at the UK’s trade balance we can see the UK is clearly a net importer.

Therefore, it has a greater demand for foreign currency than does its counterpart which would mean the value of the currency must ultimately fall according to principles of supply and demand.

However, sterling is priced higher than this trade-based dynamic because foreign investors pour money into UK-based investment opportunities.

Thus, the exchange rate is higher than the level implied by trade dynamics.

But, what if this flow of foreign investments dried up? Surely the pound would have to fall to the level implied by its trade dynamics?

Analysts at UBS told us earlier this year that the pound could actually fall to parity against the euro on such an adjustment.

Now, Morgan Stanley have sought to remind us that the pound sterling is still at risk of its over reliance on foreign capital inflows drying up.

“For foreign investors to be attracted by the UK they need to have a yield advantage,” say Morgan Stanley in a note to clients. “Unfortunately this is not currently offered, with the 10y UK gilt yield being 39bp below that of the US Treasury.”

Therefore, argue Morgan Stanley, it may be difficult to fund the current account deficit via the yield angle, requiring FX weakness to make UK investments attractive.

A cheaper exchange rate would help boost UK exports as goods and services produced in the country are made cheaper on the global market place.

It will also offer a more attractive proposition to investors of all types based on the simple fact their currency buys them more of whatever it is they are seeking to invest in.

Capital Economics: Pound Will Fall Back to 1.40 Against the Dollar

Capital Economics have also taken the chance to restate their view that the pound is trading above where they believe it should be.

“Even if the exchange rate did climb a little more in the event of a vote to remain, we suspect that it would come back down again – and fall further – before too long, given the implications for monetary policy,” says Capital’s John Higgins.

Capital Economics’ existing end-2016 forecast is $1.40/£.

Hinggins is aware that a vote to remain would probably result in a rate hike coming back on to the agenda in the UK later this year.

This could well increase the yield that Morgan Stanley see as desperately lacking in the minds of foreign investors.

“But we still think that the Bank of England’s MPC would tread more carefully than the US FOMC, relative to investors’ expectations. Recall that the risk of a “Brexit” has also been a factor in the FOMC’s deliberations on when to tighten policy further,” says Higgins.

As is the case with Morgan Stanley, the current account deficit features heavily in Capital Economics’ thinking who disagree with a prominent research house who say fair value is actually above 1.50.

The “fundamental equilibrium” value of the GBP/USD exchange rate was around 1.52 in April according to the Peterson Institute for International Economics (PIIE), higher than its prevailing level of $1.43/£.

“The medium-term current account projections for the US and the UK that feed into this estimate could be wide of the mark – the PIIE projected that, by 2021, the current account deficit would increase to 4.1% of GDP in the US, but decrease to 3.1% of GDP in the UK.

“Even if the projection is accurate for the US, we are not convinced that it is for the UK, where we suspect the ratio will be bigger without a sizeable decline in sterling’s value.”

However, it is worth noting that it is the view of PIIE that the US dollar is about 7% overvalued.

According to PIEE, divergent phases of monetary policy in the United States, on one hand, and the euro area and Japan, on the other, and a collapse in commodity prices drove the stronger dollar.

As Brexit fears fade the debate on sterling’s longer-term fair-value will become increasingly important, and investors will start paying attention to these arguments once more.