Image © Adobe Images

The British pound has surprised with its outperformance through mid-2026, here's why.

The pound is the best-performing G10 currency when viewed over a one-month timeframe, a spell of outperformance that reflects the recent strengthening in demand for the currency that's led to breakouts in a number of key non-USD pairs.

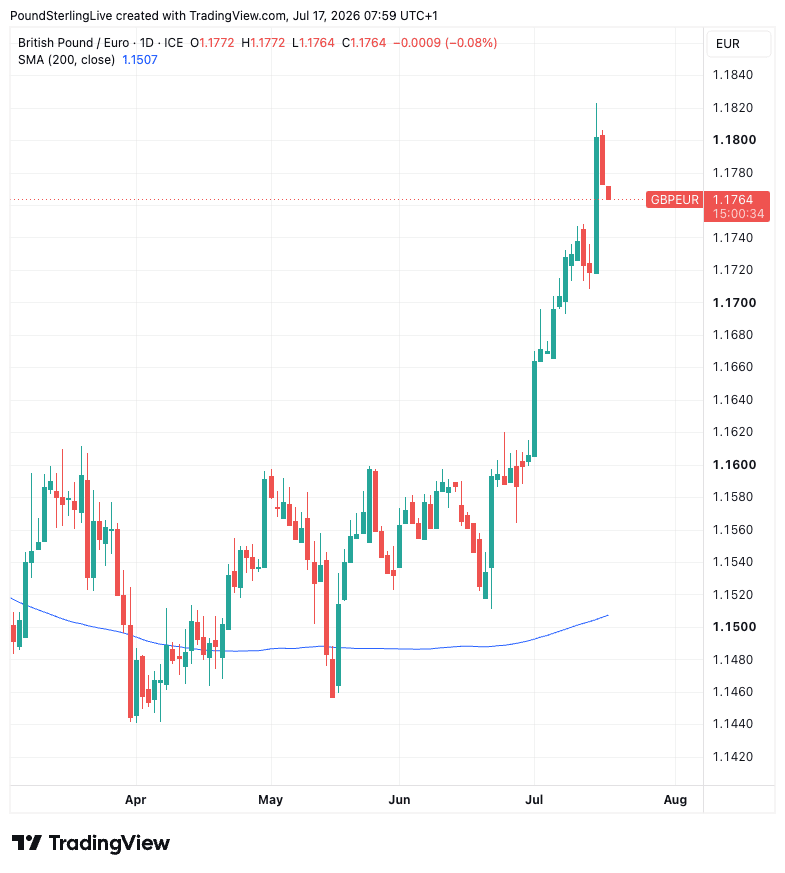

Most prominent of which is pound sterling's rise against the euro, where a breakout from a one-year range resulted in a rise into 1.18 by Wednesday, a performance that has defied consensus analyst expectations for a steady grind lower in the GBP/EUR exchange rate this year.

This points to real demand, as the GBP/EUR cross is the most heavily traded 'deliverable' FX sterling pair, a testament to the dominant role of EU trade and retail demand.

Why has the Pound Strengthened?

Analysts we follow say the pound has risen due to a combination of factors: market positioning, subsiding political risks and steady economic data outcomes, which in turn props up the pound's 'real' interest rate advantage.

Brent Donnelly, strategist at Spectra Markets, says GBP demand is proving relentless, and he spies an opportunity for the outperformance to extend.

"GBP is particularly interesting as demand is relentless and the worst case for Chancellor (Miliband) is already priced in. If Burnham were to select someone more market friendly early next week, GBP could rip even more," he explains.

A Market Friendly Chancellor

Donnelly's call was spot-on and came just ahead of unofficial reports that Shabana Mahmood was likely to become the UK's next Chancellor, meaning someone considered a centrist is lined up for the important role.

"The pound has continued to trade at stronger levels after strengthening sharply yesterday in response to media reports that Home Secretary Shabana Mahmood is set to become Britain’s next chancellor. While it has not yet been confirmed, the report provides further reassurance to market participants over the outlook for fiscal policy under new Prime Minister in-waiting Andy Burnham," says Lee Hardman, Senior FX Analyst at MUFG Bank.

File image of Shabana Mahmood. Picture by Andy Taylor / Home Office

Until the news broke, the favourite had been Ed Miliband, who would also have been viewed as less supportive for economic growth, according to Hardman.

He explains Miliband's environmental agenda can increase costs, delay projects, or redirect investment away from traditional growth sectors.

There's More to the GBP Story: M&A Demand

Analysts at Goldman Sachs say Sterling outperformance has accelerated in July thanks to "premium compression", short-GBP positioning unwinds, and an exceptionally strong pace of cross-border merger & acquisition inflows.

The pound looks to have benefited from a $202 billion (£153 billion) wave of inbound investments that has pushed regional dealmaking to a 19-year high.

In one of the largest consumer-sector corporate carve-outs in UK history, British consumer goods giant Unilever agreed to sell its extensive global food business to US spice maker McCormick & Company.

GBP/EUR has surged through the summer period.

In June, US-based ingredients giant Ingredion launched a blockbuster cross-border takeover bid for historic British food ingredients manufacturer Tate & Lyle.

Crédit Agricole says it's data shows a reacceleration of equity market inflows into the UK, which coincides with a "lack of significant inflows into the Eurozone, according to our ETF-tracker."

That has clearly created a wedge between GBP and EUR that allowed the exchange rate to power through the 1.16-1.1630 resistance barrier.

Amidst the resultant GBP demand, Goldman Sachs raised its GBP/EUR forecasts "to look for more modest Sterling underperformance ahead."

The Great Positioning Squeeze

Crédit Agricole is another institution that reckons market positioning has played a role in boosting the pound, noting the unwinding of the still considerable EUR/GBP longs in FX markets.

Markets were clearly positioned for the euro to outperform the pound in 2026 and built up considerable bets to take advantage of the outcome.

But the euro has flailed, and that's forced these bets to close out. When they do, the pound is bought.

Paring the Shorts

Analysis from CIBC Capital Markets shows 'real money' players pared net GBP shorts for the second week in a row, with the fastest reduction in eight weeks for the period ending 7 July.

In fact, according to data, the net short skew has corrected from levels last seen in March 2017.

That solid technical buying that's benefited the pound and will have contributed to range breakouts in the likes of GBP/EUR and GBP/CAD.

CICB also thinks politics has played its part in providing a narrative for the respositioning underway in the global foreign exchange space.

"Markets have reduced excessive GBP negativity as PM designate Burnham, expected to become Labour leader on Friday and PM on 20 July, has ruled out immediate changes to the fiscal framework," says a recent note from CIBC.

The Outlook for the Pound: Reasons to be Cautious

The summer recess in Parliament potentially lowers the prospect of political trap doors that might catch the pound in the coming days and weeks. But, that timing also suggests risks fall into the late summer period.

Burnham won't be able to avoid scrutiny indefinitely and will have to make real decisions in preparation for the Autumn budget.

He will try to avoid leaking any potentially negative policies to ensure the economy doesn't freeze in anticipation.

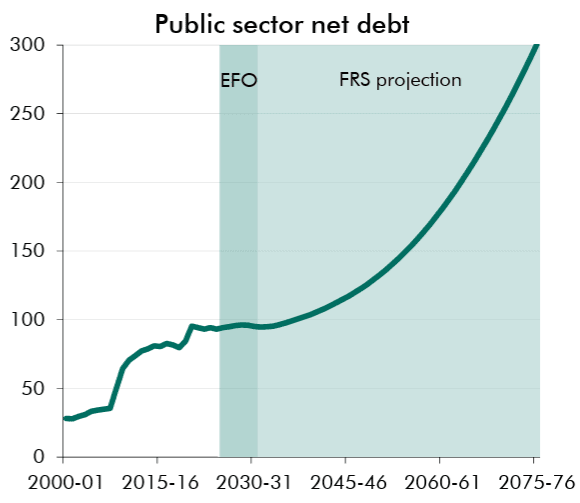

The OBR's forecasts show UK debt accumulation is on an unsustainable path.

Nevertheless, that means the budget will be a major moment for the pound as negative surprise would hit all the harder.

"Ongoing political uncertainties, including the UK heading for its seventh PM in a decade since Brexit, contribute to GBP downside risks," says CIBC.

Goldman Sachs also warns that Sterling’s gains in recent weeks have been at odds with shifting interest rate differentials, "which we think raises the risk of a reversal weaker in the near term."

CIBC agrees, saying the UK fixed income market remains uniquely vulnerable due to the continued uptrend in foreign debt holders.

Goldman Sachs also continues to see key challenges to Sterling in the longer-term, most notably overvaluation and a Bank of England that will likely be unwilling to raise interest rates.

However, "a procyclical global backdrop and the potential for closer UK-EU ties push in the opposite direction."

Free Report · Worldwide Currencies

Where Next for the Pound? Get the Quarterly Forecast Report

Consensus exchange rate projections from eleven global banking partners, including Barclays, JP Morgan and Citigroup: point forecasts, highs and lows for each quarter through to early 2027.

Delivered by email. Produced by Worldwide Currencies; for information purposes only and not investment or financial advice.