Image © Adobe Images

Political news and economic data underpin the pound's ascent.

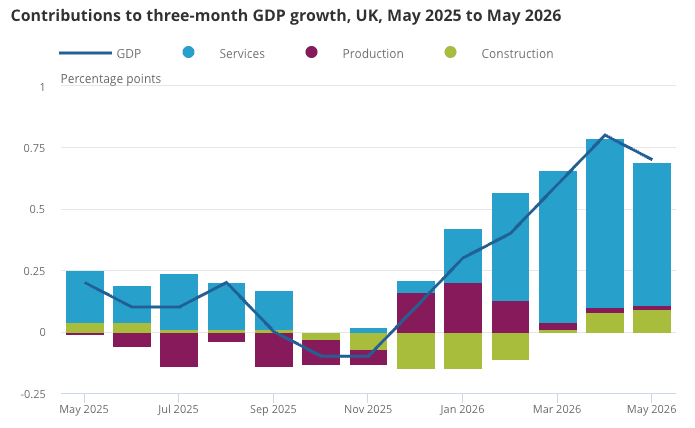

Pound sterling's blistering rally has been underscored by news that the British economy grew 0.1% m/m in May, defying consensus expectations for a negative reading.

The three-month run rate for growth now sits at an impressive 0.8%; for context, economists at Deutsche Bank judge the UK's GDP growth speed limit to be around 0.35% q/q.

"It's likely that the UK will continue to sit at, or near the top, of the G7 league table when it comes to GDP growth in the second quarter of the year. In short, PM Starmer hands over the economy to his successor on much better footing," says Sanjay Raja, Chief UK Economist at Deutsche Bank.

The strength in the economy will limit the need for the Bank of England to lower interest rates, and if anything, raises the prospect of a future hike. Growth-inspired rate hikes are exactly the kind that the pound can benefit from going forward.

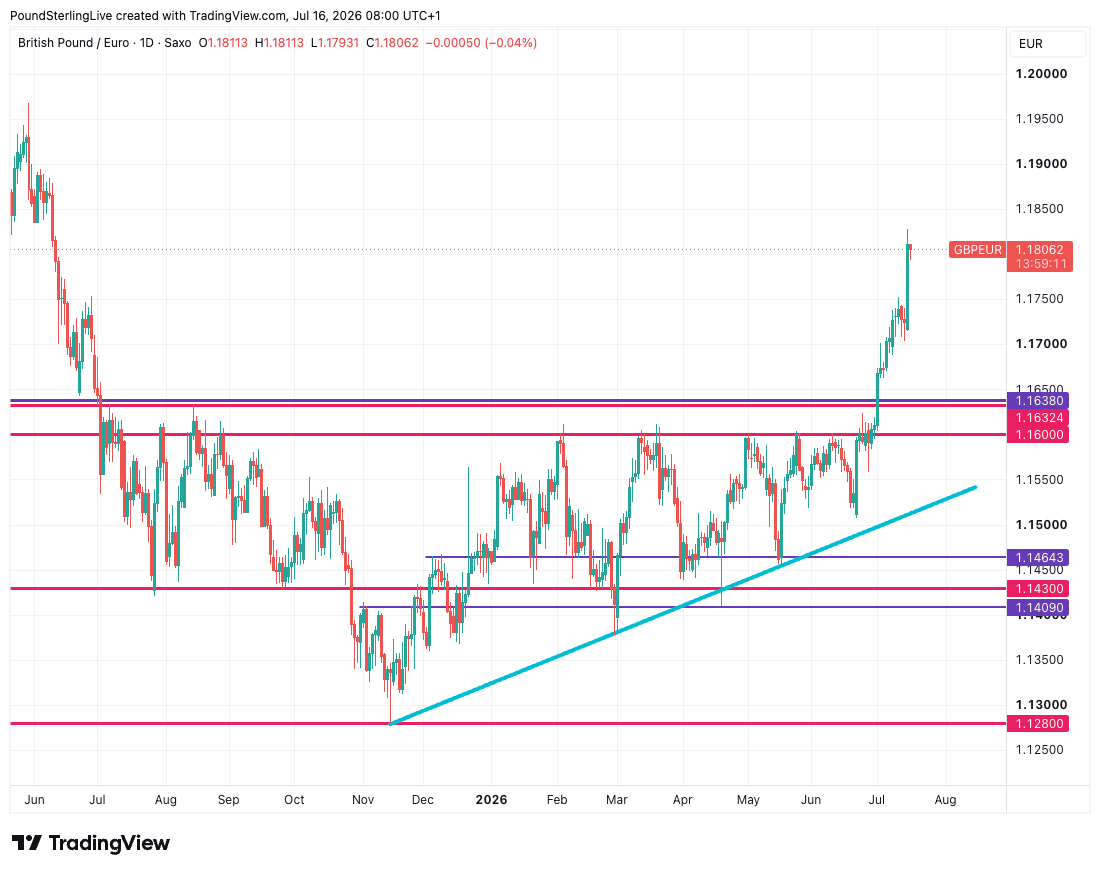

These growth data come amidst a streak of gains for the pound, which has risen to its highest level in more than a year against the euro and is up against all its G10 peers over the course of the past 24 hours.

"Barring a significant fall in monthly GDP in June, the economy will expand by 0.3% or 0.4% in the second quarter. That would be well above our prediction that output would flatline in Q2," says Andrew Wishart, UK Economist at Berenberg Bank. "The UK’s dominant services sector (which accounts for 80% of output) remained the main engine of growth."

Gains were triggered in the midweek session when political journalists reported that incoming Prime Minister Andy Burnham had settled on centrist Shabana Mahmood as his next Chancellor.

The pick means Ed Milliband, a left-leaning figure in the party, won't take the reins of the most important financial role in government.

Markets are hoping that Mahmood will be able to stand up to the left-wing contingent in Labour's parliamentary party and drive through necessary spending reforms to keep the country's growing debt pile at a manageable level.

Above: Burnham inherits an economy that's growing at impressive rates.

Burnham has already signalled that he intends to respect the existing fiscal rules that are designed to ensure the country's borrowing rates remain manageable, and his pick of Mahmood for Chancellor reinforces that commitment.

"Burnham has reassured investors. He has recommitted to the government’s current fiscal targets of covering all day-to-day spending with tax revenue," says Andrew Wishart, economist at Berenberg Bank. "If achieved, this would keep the UK on a path of fiscal consolidation that sets it apart from most other advanced economies."

Growth Still Set to Slow

Although the British economy delivered a GBP-helping headline on Thursday, economists agree that growth should steadily slow into year-end.

"Looking ahead, we expect momentum to dampen a bit," says Raja. "Indeed, the Iran energy squeeze will eventually catch up with households and businesses, constraining spending and investment."

Nevertheless, the economy enters the squeeze better poised than many had been expecting, and for the pound, that's constructive given many other countries will be facing an Iran war-linked squeeze.

"The UK will very likely see a temporary bump in GDP over July (given extended trading hours). And second, the UK is not the G7 laggard that many regard it to be," says Raja, adding:

"The latter will be important for the new Prime Minister, as it will likely offset some of the potential downgrade to the economic outlook coming as part of the OBR’s fiscal update in autumn."

The Autumn budget is considered by analysts to be the next major potential risk hurdle for the pound. Should it prove to be a benign event, the pound could even carry its outperformance into year-end.

Free Report · Worldwide Currencies

Where Next for the Pound? Get the Quarterly Forecast Report

Consensus exchange rate projections from eleven global banking partners, including Barclays, JP Morgan and Citigroup: point forecasts, highs and lows for each quarter through to early 2027.

Delivered by email. Produced by Worldwide Currencies; for information purposes only and not investment or financial advice.