Image © Adobe Images

The British pound may be drawing support from an unlikely source: widespread pessimism.

Traders remain heavily positioned for ongoing sterling weakness, political headlines remain gloomy and concerns about the UK's economic outlook continue to dominate market commentary.

Yet the data keep refusing to cooperate, and a heavy one-sided bet for pound sterling weakness could mean positioning is actually a tailwind for gains.

The latest CFTC figures show just how negative sentiment on the pound is: hedge funds and other leveraged speculators remain net short sterling futures, with bearish bets fluctuating between roughly 40,000 and 60,000 contracts during May.

That is unusual given sterling’s interest rate advantage over currencies such as the euro and Swiss franc. Only the Australian dollar - 2026's star performer - can compete on real interest rate advantage.

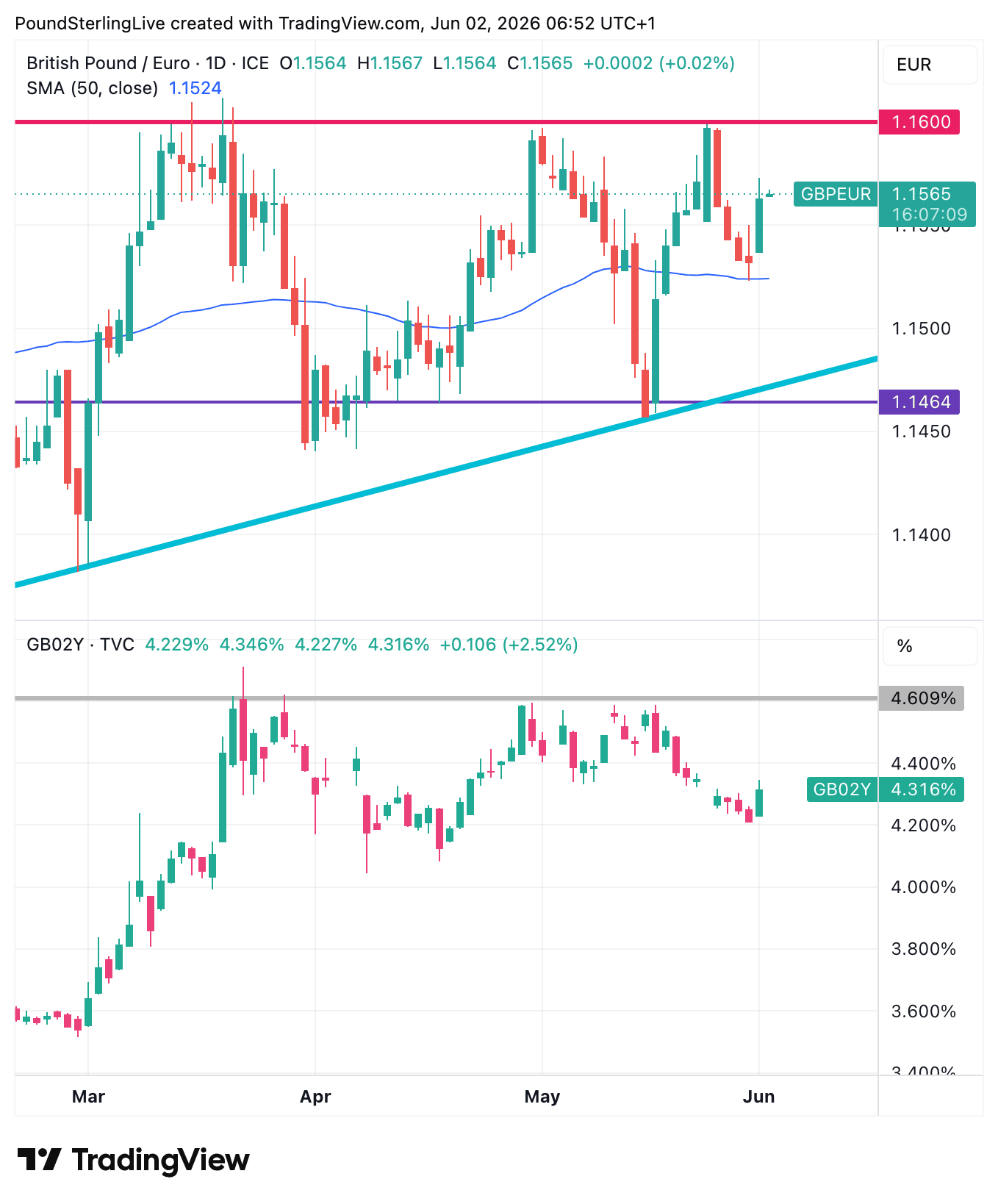

Above: An interest rate (via 2-year bond yield in lower panel) has supported pound-to-euro to the 1.16 level and underpins a steady uplift since November (blue trendline in upper chart).

FX markets are perennially inclined to favour 'carry', which is the pursuit of higher interest rate yields by foreign investors, a scenario that puts the pound in a robust position heading through the mid-year period.

However, investors look inclined to bearishness when considering the pound, focusing on UK political uncertainty, fiscal credibility concerns and expectations that economic growth will weaken later this year.

"There seems no end to the current "noise" surrounding the UK and markets and 2026 has been no different. Add to this an increasingly volatile geopolitical landscape and one would be forgiven for thinking that GBP has been buffeted by significant forces," says Kamal Sharma, FX strategist at Bank of America.

Yet, the problem for sterling bears is that the incoming data is refusing to cooperate with the sellers.

"In the UK we think pessimism may be overstated," says Andrew Sheets, a strategist at Morgan Stanley.

Sheets notes that first-quarter GDP growth was solid, manufacturing activity remains in expansion territory and productivity has surprised to the upside.

He also highlights comments from one of Britain’s largest commercial property operators. "Occupancy is now up to a 20-year high and rents are growing at their fastest pace in nearly two decades."

"Continued resilience in mortgage lending and housing market activity in April suggests the economic fallout from conflict in the Middle East has not yet hit household borrowing as hard as some feared," says Martin Beck, Chief Economist at WPI Strategy.

Mortgage approvals rose to a 15-month high in April, while gross mortgage lending reached its second-highest level since March 2025.

"Household borrowing is proving surprisingly resilient in the face of geopolitical uncertainty, higher inflation risks and tighter financial conditions."

Manufacturing is telling a similar story.

"The UK manufacturing PMI points to a sector still expanding in May, rising to a four-year high of 53.9 from April’s 53.7," says Beck.

"All five of the PMI sub-components - new orders, output, employment, suppliers’ delivery times and stocks of purchases - were in positive, plus-50, territory, the first time this has occurred since May 2022," he adds.

When Bearish Positioning Becomes a Tailwind

Importantly, these developments arrive at a time when investors appear primed for disappointment.

When positioning becomes heavily skewed towards a bearish outcome, it takes less positive news to force a reassessment.

The move in sterling shorts from around 60,000 contracts to nearer 40,000 during May suggests some investors have already started taking profit on bearish bets.

That process could have further to run - taking spot higher - if economic surprises continue to come in on the right side of expectations.

The irony for sterling is that many of the concerns weighing on sentiment are well known and already reflected in positioning.

"The pound has been resilient this year with EUR/GBP (the key proxy for UK political/fiscal risks) lower since the start of the year," says Bank of America's Sharma. "Further out, a higher productivity/capital intensive mix of FDI inflows should be seen as a medium-term positive for GBP valuation trends."