Picture by Simon Dawson / No 10 Downing Street.

The British pound is down as markets factor in growing political instability.

Keir Starmer is effectively done; the herd is moving against him and it's now a question of how the transition unfolds.

Six Cabinet ministers, including the Home Secretary Shabana Mahmood and Health Secretary Wes Streeting, were expected to tell the Prime Minister to consider his position at today's Cabinet meeting.

However, the push has been delayed as reports confirm they were not given the chance to do so and four Cabinet allies of Starmer briefed journalists on camera after the meeting that Starmer would stay.

The odds have therefore slightly swung back in favour of him staying in post, and the pound has consequently recovered from the day's lows.

However, it's far too early to suggest the Prime Minister is in the clear as rebels are growing in confidence: by the end of Monday, 79 Labour MPs publicly demanded his resignation, including six ministerial aides who quit the Government to back the mutiny.

Wes Streeting is tipped by some political commentators to be ready to make a go for it, but there's hope amongst many in the party that a contest is delayed long enough to allow Manchester mayor Andy Burnham to stand in a by-election, win, walk into Westminster and be coronated by his fellow MPs as next Prime Minister.

What Does This Mean for the Pound?

A long and drawn-out march towards the installation of a figure who has failed on multiple occasions to become the leader of Labour is hardly inspiring for markets.

Little wonder there's a heavy feel to GBP price action now, even if there's still no Truss-style panic. The currency market has been remarkably calm until now, with pound-euro dipping on Monday, but it's extending its selloff more forcefully on Tuesday, reaching 1.1506.

Pound-dollar retreats to 1.3515 on Tuesday, putting it 0.70% lower on the day.

Those with payment requirements must take action to protect their budget, and we suggest engaging a specialist who can give you access to the right tools and guidance as GBP volatility rises.

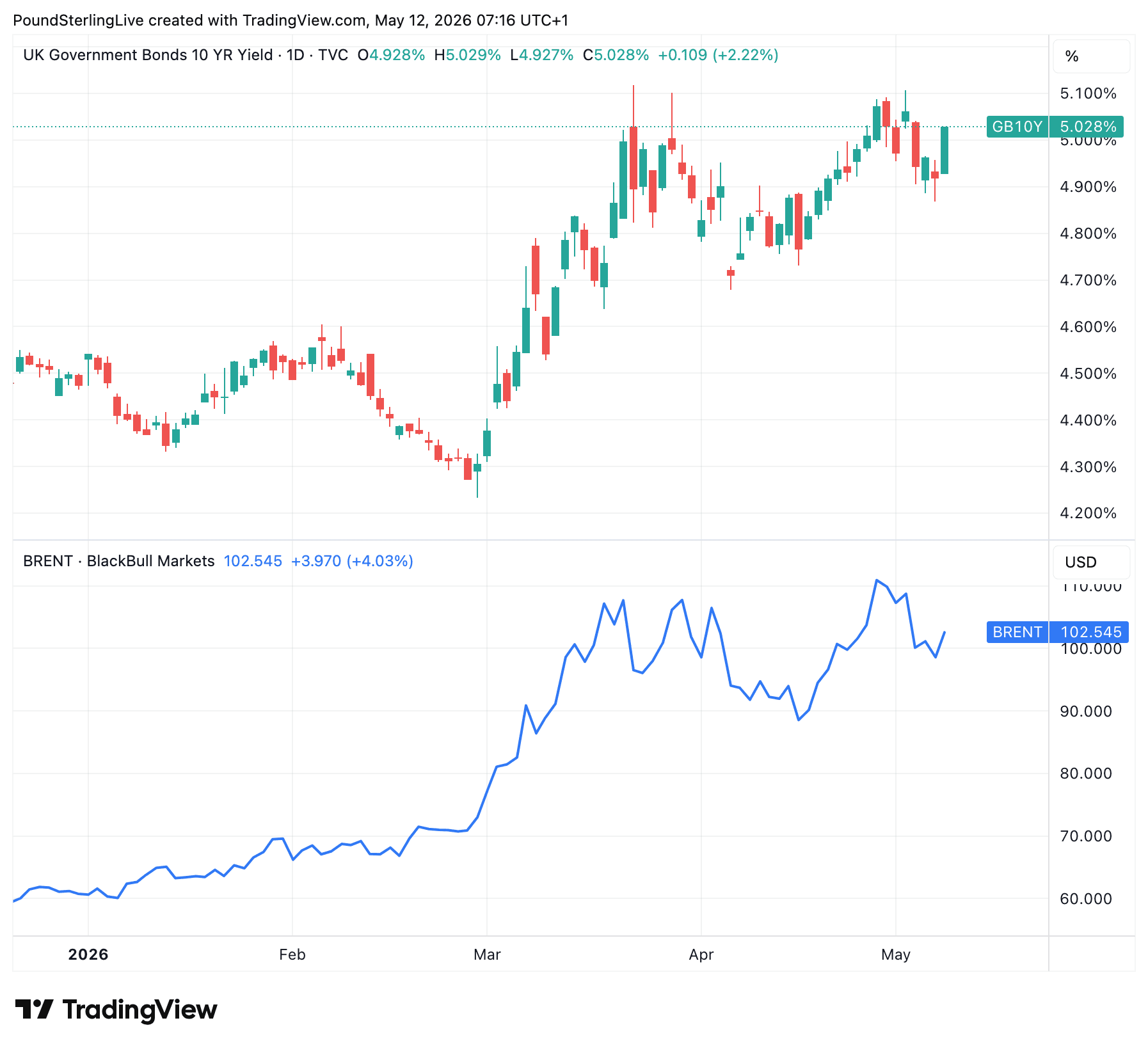

Bond markets are where there's a definite sense of unease: UK bonds, known as gilts, fell sharply on Monday and their yield shot up.

Consensus projections for the next four quarters, compiled from leading investment banks.

Access the full forecast →

Yields have risen in other countries too, owing to another rise in oil prices, but it's important to note that UK yields have easily outpaced their peers, suggesting a UK-specific premium is being demanded.

In short, politics does matter.

"The market’s main concern here, and the reason for this Gilt underperformance, is twofold – firstly, that a new PM would shift to the left, and loosen/scrap the UK’s current fiscal rules; and, secondly, that doing so would exacerbate the UK’s inflation problem. With political uncertainty likely to persist for a while, and the fiscal rhetoric only set to ramp up, those considering buying the dip in Gilts may be minded to wait a while," explains Michael Brown, Senior Research Strategist at Pepperstone.

Under Pressure, But It's No Fire Sale

GBP losses are now certainly reflecting developments in Westminster, but it's important to stress this isn't a market in panic mode. Here, I define panic as a repeat of a Liz Truss moment, which resulted in a severe GBP selloff.

We also saw smaller panics in January and July of 2025 when the market worried about the fiscal setup under Rachel Reeves and whether she would be able to get a grip on spending.

Stay Wary

Having covered pound sterling for many years it's important to stress the market can quickly shift and we would be very wary of a big drop in the pound in response to all this.

A sanguine FX market can suddenly change its tune, and when it does, it can be ugly.

So, for those with FX payments, be incredibly wary and plan accordingly.

Starmer's Replacement Will Matter

Political commentators say evidence suggests those around current Health Secretary Wes Streeting are on the move, suggesting he will confirm he's a contender before long.

We suspect the market would be relatively welcoming of a Streeting premiership as he is more likely to tack a centrist path and stick to the fiscal rules.

However, things might change under either a Burnham or Rayner premiership as these two candidates are left-leaning and have argued for a change to the UK's fiscal rules.

That means more spending financed by borrowing, which would pressure debt markets. The pound would likely fall significantly under such a shift.

Bond Yields are Providing The Currency Some Support

Bonds - the IOU that governments issue when borrowing - have fallen in response to a combination of elevated oil prices and building political concerns.

That means the interest rate they yield has risen. In normal times, a rise in yield would be supportive of sterling as international capital chases higher returns.

We suspect pound sterling's relative resilience until now could reflect some demand for UK bonds from international buyers who like the idea of superior returns.

If the putch against Starmer fades, that demand could come back and send Sterling higher.

Above: UK ten-year bond yields have jumped, largely thanks to rising oil prices (lower panel).

Of course, confidence matters: as long as these investors believe the ship will right itself after this period of political instability, they will be happy to buy.

If that confidence takes a knock, bonds and the pound will sell off in tandem and a real rout could ensue.

The Leftward Lurch

The concern for markets is that a new leader will be tempted to borrow more to fund more spending on welfare and social projects, increasing the country's debt burden and pressuring public finances even further.

The inevitable endgame is a bond buyers' strike that triggers a financial crisis.

On cue, Labour’s influential Tribune group of more than 100 MPs has called for less “caution” on fiscal policy in a new pamphlet that demands a change of direction to the left.

Louise Haigh, the Labour MP who chairs the group, says the current structure of the UK Treasury’s role in fiscal policy "resolved in favour of caution".

She says Britain’s "fiscal and institutional framework" is "unfit for purpose".

She also calls for major tax rises on wealth.

"A lurch to the left wouldn’t go down well with bond markets. In this scenario, we would likely see further downside pressure on sterling and a steepening at the long end of the yield curve amid concerns about increased public borrowing," says Marc Cogliatti, Head Markets Risk Strategies at Validus Risk Management.

Concierge Money Transfers

For high-value transfers, you need high-value service: dedicated account management, on-point pricing, insight into market conditions and trends, help with structuring your payment, and execution support at key moments.

Learn More →