![]()

Image © Adobe Images

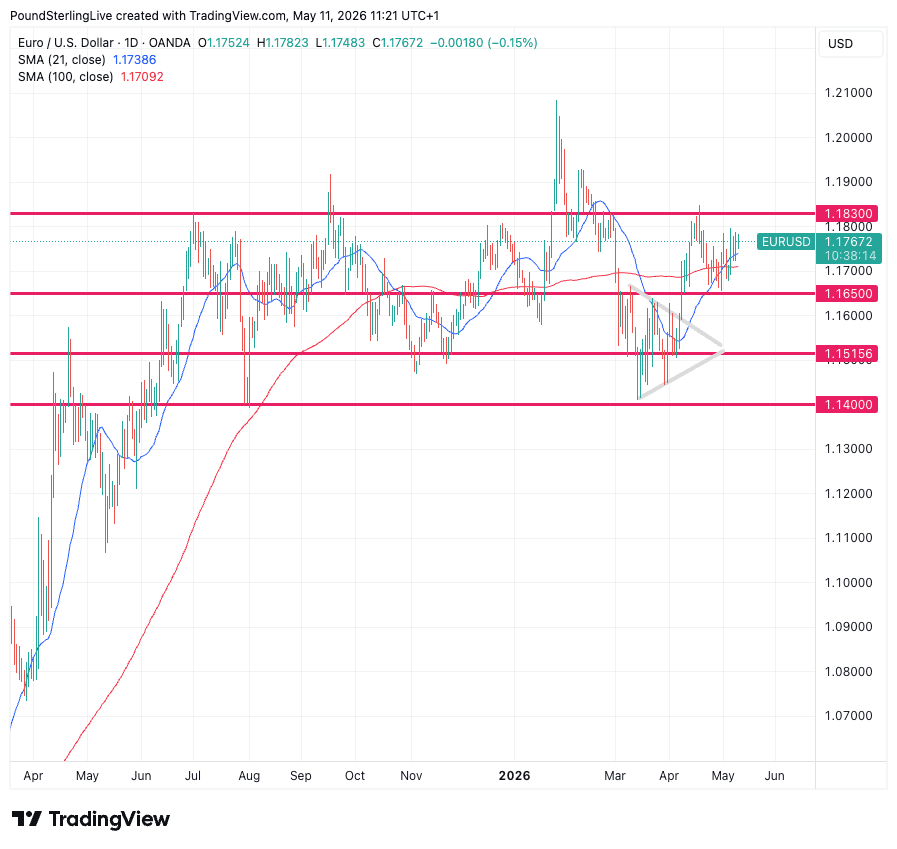

The euro-to-dollar exchange rate rises to 1.1767 on Monday following a nervous start for the pair thanks to unhelpful headlines stemming from the Middle East at the weekend.

Having opened the new week at 1.1752, we're seeing a bit of a recovery, albeit the market is still some way off Friday's peak of 1.1788 and Wednesday's test of 1.18.

So it's a tetchy start for the world's most important currency pair, but the important point to note amongst the to-and-fro of daily movements is the near-term pattern is still one of 'higher lows' where pullbacks close out at sequentially higher levels.

That, in short, is what an uptrend looks like.

EUR/USD is drawn to the 21-day moving average (MA), currently at 1.1738, which is rising and consistent with our expectations for further gains.

Based on this, a move to 1.1830 could be a reasonable target in the short-term (1-2 weeks) while weakness could extend as low as the 100-day MA at 1.17.

The dollar is softer at the start of the new week despite another move higher in oil prices owing to ongoing uncertainty as to whether or when the Strait of Hormuz will fully reopen to traffic.

Although higher oil prices boosted the dollar during the early stages of the Middle East conflict, the same is no longer apparent.

In fact, the drift lower in USD comes despite no real indication of a credible breakthrough being at hand.

That's instructive as it betrays a market that is comfortable with the steady depreciation of the dollar that's been in place since 2025.

"There is no doubt that, so far, President Trump’s desire for a weaker dollar is being rewarded by markets, despite the relative out-performance of the US economy, heightened global uncertainty and a dollar-friendly global terms of trade shock. Part of this is down to relative monetary policy shifts, with European policymakers’ hawkishness in the face of inflation contrasting with US insouciance," says Kit Juckes, an analyst at Société Générale.

It's no surprise then that euro-dollar is closer to the top end of the range it has occupied since July 2025 than the bottom.

Risks look assymetrically balanced to the upside and we wouldn't be surprised to see 1.19-1.20 coming into play later in the year once a feasible Middle East agreement has been reached.