Image © Adobe Images

But, this tailwind can very quickly turn into a headwind.

The British pound trades near weekly highs against the euro and dollar following another jump in UK bond yields as investors account for a future of elevated inflation and rising political risks.

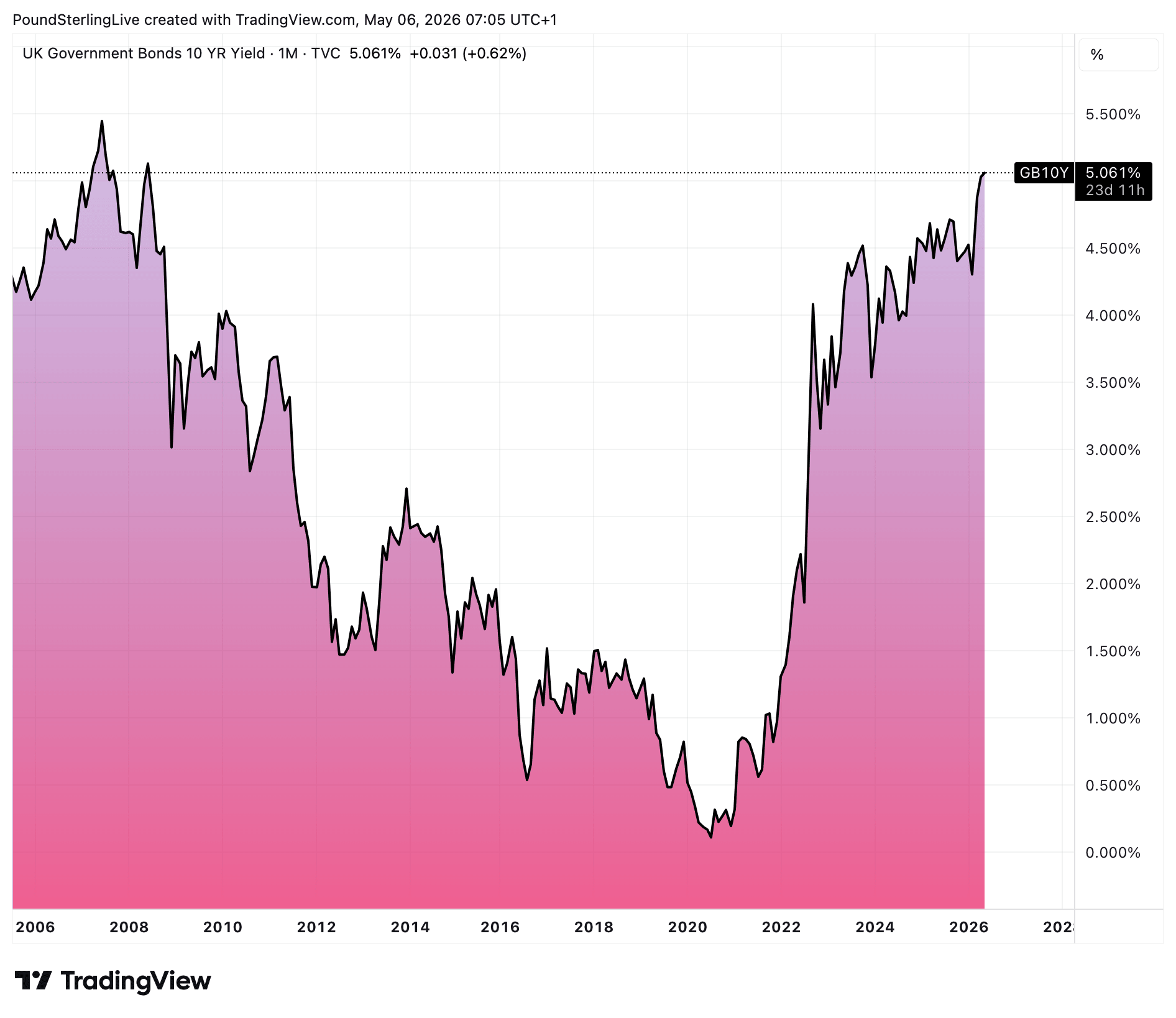

The yield on British bonds, of all tenors, rose notably on Tuesday, outpacing the rise in yields in other G10 nations. The bonds rose because investors sold the underlying bonds.

That relative outperformance on yield translated into another robust performance by GBP, although no fresh highs were recorded.

The pound-euro exchange rate once again bumped its head on the 1.16 ceiling, a level it will struggle to cross, while pound-dollar rose back to the ceiling at 1.36.

Two-year bond yields rose as investors continued to account for a future of higher inflation levels and a higher Bank Rate at the Bank of England. Longer-term yields accounted for these expectations, but also reflected some building anxiety about the risks of holding British debt in light of a potential period of political instability (this is known as the term premium: a higher bond yield simply means lenders demand a higher return for exposure to this debt).

The UK two-year yield rose to 4.522%, the ten-year went as high as 5.10%, a joint high with March and, before that, a level last seen in 2008.

"With the 30 year gilt yield having reached a 28 year high at 5.78%, this forces the Treasury into absorbing higher interest costs at a time when they may also be asked to fund additional giveaways by a possible new leadership team. This could result in weaker fiscal rules or substantially higher taxes, with implications for growth," explains Lindsay James, investment strategist at Quilter.

Above: UK two-year yield minus German 2-year (top) and GBP/EUR.

Consensus projections for the next four quarters, compiled from leading investment banks.

Access the full forecast →

Although yields also rose in Germany, the EU, U.S. and across the spectrum, Britain saw a much more notable move.

"The yield gap between UK and German 10-year government bonds is now nearly two full percentage points. While global yields are up across the board," says Mohamed A. El-Erian, advisor to Allianz and former CEO of Pimco.

International capital tends to flow from lower yielders to higher yielders, which is why this dynamic can support GBP exchange rates as long as there's enough confidence floating around in the system. Surely helping sterling in these tricky times are confident global investors who have sent U.S. stocks to fresh records over recent hours.

And that's the rub for the pound: bond yield outperformance is supportive of the currency until all of a sudden it's not. Triggers like a drop in global investor confidence can reframe the approach to the UK's rising yields. If confidence wanes a bond selloff can morph into a firesale at which movements become unruly and the pound tanks.

Above: GB 10-year bond yields are at levels last seen in 2008.

We saw such an episode when Liz Truss tried to pass her mini budget, and again on a couple of occasions last year when Rachel Reeves' spending and tax plans were called into question.

Despite the rise in yields the pound is unable to break to fresh highs against the euro and dollar, which signals to us that there's definitely some concern in markets that prevents the currency from engaging an outright rally.

The looming test for markets is the impending local election in England and the devolved administrations of Scotland and Wales. Prime Minister Starmer's Labour Party is set to lose thousands of seats and Westminster is awash with talk of leadership contenders.

"Another asymmetric movement higher in UK bond yields - speaks to the double jeopardy of events in the Gulf and (post election) political risk in the UK at the end of the week. Spread of UK 10-year Gilts over rG7 max up to 64bp - a new high.... Not a great look," says Simon French, Chief Economist at Panmure Liberum.

"This UK premium creates a bigger headwind for domestic growth and puts more pressure on the Treasury compared to Eurozone peers and the US," says El-Erian.

Concierge Money Transfers

For high-value transfers, you need high-value service: dedicated account management, on-point pricing, insight into market conditions and trends, help with structuring your payment, and execution support at key moments.

Learn More →The market worries that the UK is heading for another bout of political instability. Former Vice Prime Minister Angela Rayner is said to be on manoeuvres and her policy platform reads like a socialist's dream. As does that of Andy Burnham. Both would likely require the government to break the fiscal rules that ensure borrowing is kept in control.

The market is asking whether the UK can afford these projects. And even if Starmer stays, he will likely change policy to please would-be supporters of Rayner and Burnham. Indeed, it's reported Wednesday that the PM will deliver a major 'reset' speech next week once the results of Thursday's vote is fully known.

"Renewed challenges to Prime Minister Keir Starmer's leadership, particularly following the May 2026 local elections, represent a major risk of political instability. A leadership change could unnerve markets and lead to a sell-off in sterling," says Sergio Capaldi, Fixed Income Strategist at Intesa Sanpaolo.

However, Kallum Pickering, Chief Economist at Peel Hunt, sees some silver linings emerging from the murmurings of the bond markets.

"The bond market sell-off is a gift to Starmer and Reeves - yet again! Whichever duo wishes to replace them needs to put forward a coherent plan for growth and fiscal sustainability which also does not increase inflation pressures - otherwise it’s lettuce time again," he explains.

"Lettuce time" refers to the Truss premiership that had a shelf life shorter than that of a supermarket lettuce.

With Truss in mind, the Labour Party might be inclined to think their chances of survival are even worse under a new leader whose fiscal policy triggers true market pandemonium.