"Whether or not that response needs to be as large as the shift in market interest rates, since our last set of forecasts, remains to be seen. For one thing, there is now some uncertainty about the prospective scale and nature of the government’s energy subsidies," - Deputy Governor Ben Broadbent, Bank of England Monetar Policy Committee.

Image © Adobe Stock

Pound Sterling's early gains melted away to leave behind widespread losses in what could remain volatile trade on Thursday following 'dovish' commentary from one Bank of England (BoE) official and amid what is increasingly banana republic style dysfunction in government and Westminster.

Sterling had climbed back above 1.12 against the U.S. Dollar and was trading higher against many comparable currencies in early trading on Thursday but these gains were quick to melt away and left behind in their wake widespread losses against most other easily comparable currencies.

Thursday's reversal followed a speech in which a member of the BoE's Monetary Policy Committee warned an audience at Imperial College London of the damage that would likely be done to the economy if the bank raises interest rates in line with some market-implied measures of expectations.

"If Bank Rate really were to reach 5¼%, given reasonable policy multipliers, the cumulative impact on GDP of the entire hiking cycle would be just under 5%," Deputy Governor Ben Broadbent said.

"The MPC is likely to respond relatively promptly to news about fiscal policy. Whether official interest rates have to rise by quite as much as currently priced in financial markets remains to be seen," he later said in conclusion.

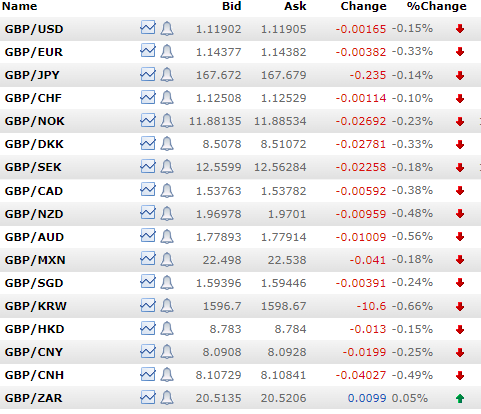

Above: Selected interbank reference rates for Sterling. Source: Netdania Markets.

Ahead of those particular remarks Broadbent had explained how spending commitments contained in late September's budget would be likely to draw an interest rate response from the BoE before outlining the significance of October's reversal of those plans.

"Whether or not that response needs to be as large as the shift in market interest rates, since our last set of forecasts, remains to be seen. For one thing, there is now some uncertainty about the prospective scale and nature of the government’s energy subsidies," he said.

The new government's earlier budget proposals were perceived as a source of added inflation risk because they would support demand in the economy at a time when inflation is in the double-digit percentages and the BoE is looking to reduce that demand in order to meet its 2% inflation target.

However, the replacement of the earlier chancellor Kwasi Kwarteng with former health secretary Jeremy Hunt has seen many of the earlier proposed measures reversed and leaves the economy heading into a steep downturn in which fiscal 'austerity' will be a partial instigator of the wreckage.

These kinds of economic circumstances should mean the BoE has less reason to raise interest rates though it's not clear the market sees it the same way.

Ben Broadbent's full speech can be accessed here.

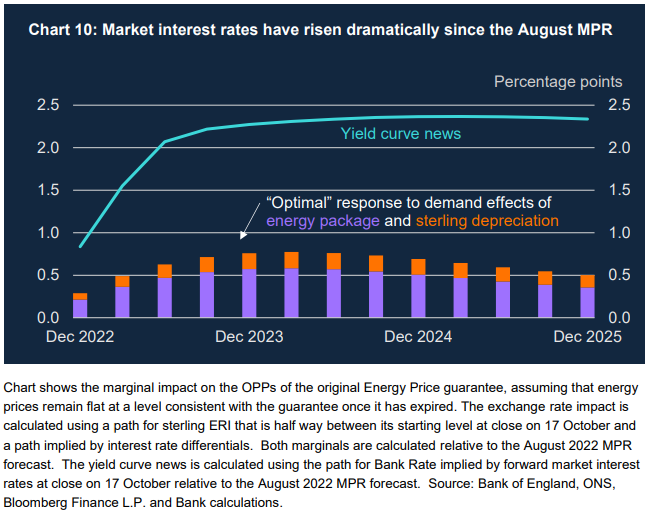

Source: Bank of England.

Source: Bank of England.

Thursday's trading marked a second consecutive day of widespred losses for Sterling exchange rates that were driven lower on Wednesday by a further increase in UK inflation, broad strength in the U.S. Dolllar and Westminster's descent deeper into the realm of the banana republic.

Wednesday's losses reached a crescendo after the departure of now-former Home Secretary Suella Braverman, which was followed by chaotic scenes in parliament and comes toward the tailend of a month in which there have been widespread reports of 'rebellion' against the newly selected Prime Minister.

"Both as a Brit and a global strategist this a farce; a tragicomedy; embarrassing; and a coup by any other name. Obviously it’s a political coup; resigning over an email in this day and age?! Braverman’s angry out-the-door letter made that clear," says Michael Every, a global strategist at Rabobank.

"Worse, the cash-strapped UK Treasury is going to give the Bank of England £11bn to cover the operating losses made via QE!. An institution that can literally print money is taking a sum of cash that could cover the cost of four aircraft carriers just when the UK needs to be building them," Every said on Thursday.

Readers should note that it is HM Treasury and not the BoE who determines if losses stemming from the reversal of BoE quantitative easing are reimbursed from the public finances or left on the BoE balance sheet.

Not all national treasuries and central banks operate in the same way: For instance, in Australia, the above described arrangement works in reverse with losses remaining the responsibility of the Reserve Bank of Australia.

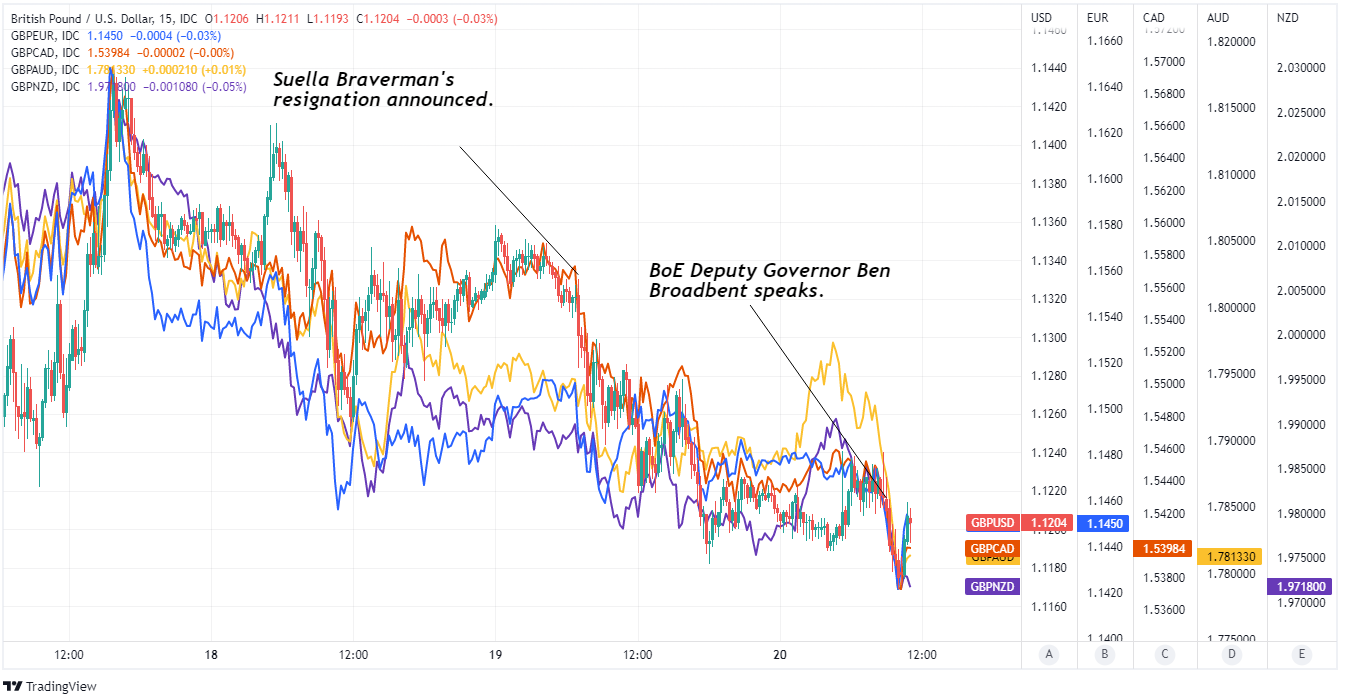

Above: Pound to Dollar rate at 15-minute intervals alongside other Sterling exchange rates.

Above: Pound to Dollar rate at 15-minute intervals alongside other Sterling exchange rates.