- Negative reaction to Kwarteng's fiscal statement

- But Sterling crisis unlikely says Oxford Economics

- Although gradual fall to record lows still likely

Above: The Chancellor Kwasi Kwarteng leaves 11 Downing Street to deliver The Growth Plan to parliament. Image source: Gov.uk.

The British Pound tanked in the wake of the significant tax cuts announced by the UK government, and although record lows are possible, a full blown 'Sterling crisis' is unlikely says Oxford Economics.

The call from the independent research providers comes after the UK government announced the biggest package of tax cuts since 1972 in an effort to push UK trend economic growth to 2.5%.

The Pound fell sharply in response to the announcement as UK government borrowing rates surged higher as investors bet the government would struggle to fund the moves.

"Initial market reaction has been negative across a range of assets, reflecting concerns about the lack of a credible long-term strategy for the public finances," says Andrew Goodwin, Chief UK Economist at Oxford Economics.

The radical shake up of the UK's tax code is an acknowledgment by the new government of Liz Truss' government the consensus of previous conservative governments on how to drive growth has failed.

Headline announcements include the cutting of the basic rate of Income Tax from 20p to 19p, from April 2023.

The top rate of income tax was cut from 45p to 40p, while this year's hike to National Insurance Contributions would be cancelled in November.

A planned corporation tax hike has meanwhile been panned while first-time house buyers will see notable easing of the Stamp Duty burden.

The government estimates the cost of all the announced tax cuts to amount to £45BN.

But it is the government's decision to cap energy bills that will cost far more than the tax cuts, with some estimates going as high as £130BN over the next two years.

Put together, this means the government will have to borrow more, increasing the supply of gilts to the market.

This as the Bank of England starts selling its own stock of gilts acquired via quantitative easing.

The increased supply means investors are demanding greater compensation for holding UK government debt, raising the overall cost of borrowing.

The fall in the Pound is a further signal of investor concerns the government will struggle to fund its plans.

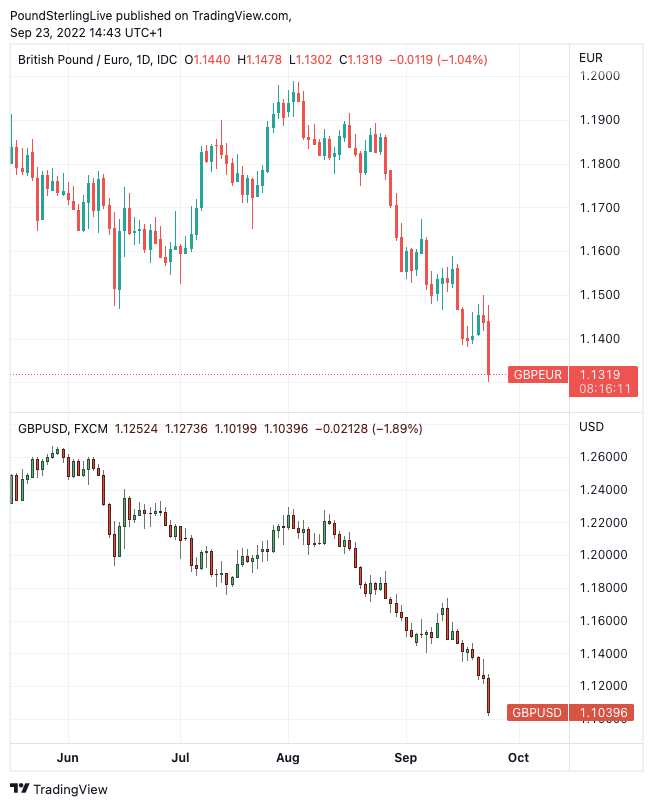

Above: GBP/EUR (top) and GBP/USD (bottom) at daily intervals. To better time the market, set your free FX rate alert here.

The decline came at the same time global markets were experiencing a significant sell-off, which even in normal times creates headwinds for Sterling.

"There has been a very negative reaction in the markets, Sterling is very much under pressure," said Jane Foley, Senior FX Strategist at Rabobank.

Foley said some of her clients were "panicking".

The Pound to Dollar exchange rate fell to a new post-1985 low at 1.1021 in the wake of the chancellor's statement. The Pound to Euro exchange rate fell by a percent to 1.1340.

The sharp declines have lead some to speculate whether a 'Sterling crisis' is evolving.

"Though the market reaction has been negative, we think it's unlikely that the government's approach will cause sterling to collapse or create problems in selling gilts," says Goodwin.

Oxford Economics assesses Kwarteng's package as being more likely to be effective in generating a short-term boost to demand than actually delivering the intended boost to supply.

"Given that the economy is flirting with recession, demand-supporting tax cuts are not necessarily a bad idea. But these tax cuts are designed to be permanent, not temporary," says Goodwin.

Goodwin adds the absence of a credible long-term economic and fiscal strategy does leave UK assets vulnerable, with Sterling the most obvious release valve.

Even though Oxford Economics does not expect a Sterling crisis, they do anticipate an ongoing decline in valuation.

"Despite the likelihood of more aggressive monetary tightening, we expect sterling to continue to drift lower to around $1.05 in the short-term," says Goodwin.

This would line the Pound up for record lows.

Oxford Economics meanwhile anticipates the Bank of England will have little option but to increase the size of its interest rate hikes, something the Bank alluded to in the minutes to September's Monetary Policy Meeting.

"With the package being towards the upper end of expectations, we think the BoE will react aggressively. We now expect a 75bps hike at November's meeting and will raise our forecast for the peak in Bank Rate to 4%, from 3%," says Goodwin.