- UK economic growth disappoints

- Means UK is now the underperformer amongst G10 peers

- GBP hugs bottom of recent ranges

Image © Adobe Stock

The British Pound struggled to recover the substantial losses of the previous week, finding little support from a slew of UK economic data released Thursday November 11 that confirmed the economic rebound continued to disappoint against economists' expectations.

The British Pound struggled to recover the substantial losses of the previous week, finding little support from a slew of UK economic data released Thursday November 11.

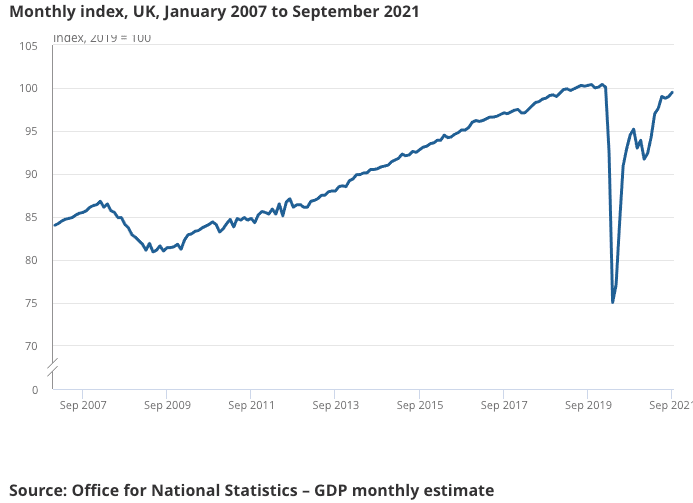

The ONS reported the UK economy grew 0.6% in September as economic activity recovered further from August's 0.40% growth. The market was looking for a reading of +0.40%.

Growth does appear to be picking up somewhat again after a poor summer: construction output grew by 1.3% in September 2021, following two consecutive months of contraction.

The all-important services sector saw output increase by 0.7% following broadly flat movements in July and August 2021.

But August's growth rate was revised down by 0.2 points, and July's by 0.1 points.

- Reference rates at publication:

GBP-EUR: 1.1678 \ GBP-USD: 1.3395 - High street bank rates (indicative): 1.1450 \ 1.3120

- Payment specialist rates (indicative: 1.1620 \ 1.3328

- Find out about specialist rates, here

- Or, set up an exchange rate alert, here

"The economy regained some momentum in September, but continued shortages and the drag on real incomes from higher utility prices probably mean it will soon fizzle out," says Paul Dales, Chief UK Economist at Capital Economics.

The data were largely softer than analysts had been expecting: the economy grew 1.3% in the third quarter, which is softer than the 1.5% the market was looking for and below the 1.5% the Bank of England had forecasted.

Annual GDP read at +6.6% which was softer than the +6.8% anticipated.

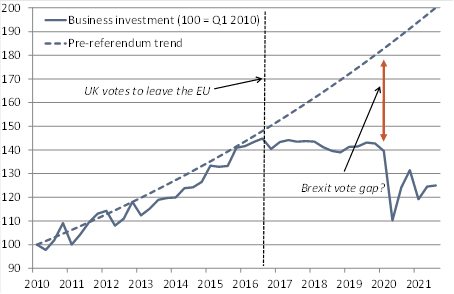

Worryingly, business investment was very week coming in at just +0.4% quarter-on-quarter in the third quarter, the market was expecting a reading of +0.2%.

"Despite rising business confidence, profit expectations and investment intentions, the gain in business investment remained worryingly weak in Q3," says Kallum Pickering, Senior Economist at Berenberg Bank. "Business investment stalled after the Brexit vote before collapsing during the pandemic".

Pickering says a combination of factors are likely responsible: the UK’s unique Brexit-related issues, higher non-tariff barriers with the EU, port and transport challenges and continued political uncertainty linked to the ongoing UK-EU dispute over the Northern Ireland protocol.

Above: Business investment trends UK. Image courtesy of Berenberg Bank.

Industrial production contracted 0.4% month-on-month in September, which is worse than the +0.2% the market was looking for while manufacturing grew 0.1% month-on-month in September, which is softer than the 0.2% the market was looking for.

The country's trade balance slipped deeper into deficit with -£14.74BN being reported, worse than the -£14.30 the market was expecting.

In short, it is hard to see a firm argument for Sterling upside amongst these disappointing data.

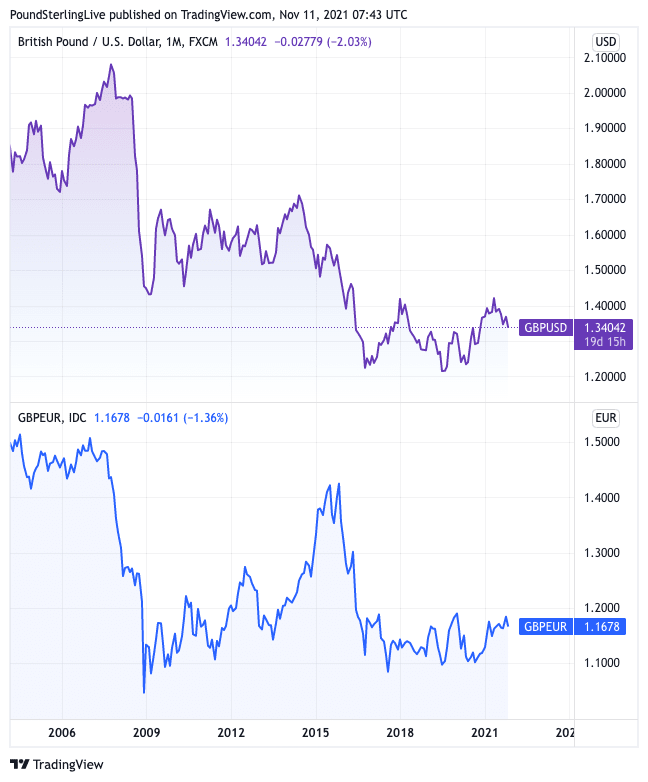

The Pound to Euro exchange rate is quoted at 1.1682 having started November at 1.1839, the Pound to Dollar exchange rate is at 1.3408 having started the month at 1.3681.

Above: Decades worth of trade deficits have taken their toll, ensuring the Pound hugs the bottom of a multi-year range against the Euro and Dollar.

"The pound was lower after this morning’s GDP release with GBP/USD trading below 1.34, down from around 1.3650 a week ago," says Hann-Ju Ho, an economist at Lloyds Bank.

The ONS says GDP remained 0.6% below its pre-coronavirus pandemic level (February 2020) in September 2021.

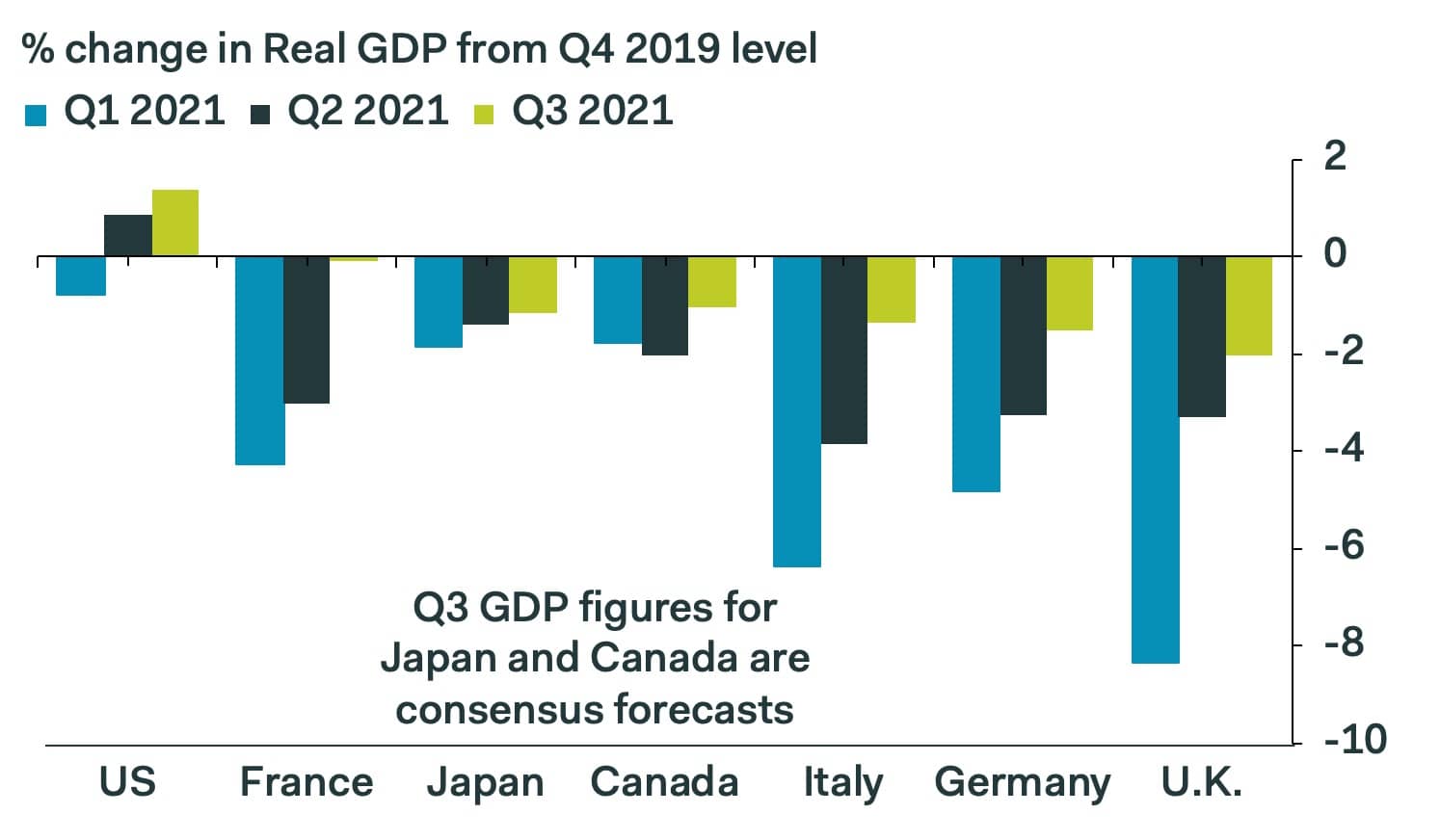

"The UK economy has reclaimed its status as the G7's laggard," says Samuel Tombs, Chief UK Economist at Pantheon Macroeconomics.

Third quarter GDP was 2.1% below its fourth quarter 2019 level, whereas it was 1.4% above in the U.S. and only 0.1% below in France, 1.4% in Italy and 1.5% in Germany. Japan & Canada haven't released third quarter data, but saw smaller shortfalls in the second quarter says Tombs.

Above: How the UK compares to its major rivals in the post-Covid rebound stakes. Image courtesy of Pantheon Macroeconomics.

Looking ahead, Capital Economics says "the best of the recovery is now behind us," and that shortages combined with the hit to the real spending power of businesses and households from higher taxes and rising utility prices will mean that GDP growth is sluggish over the next six to nine months.

"We doubt that the Bank of England will raise interest rates above 0.50% next year," says Dales.

For the Pound this matters: raising interest rates is a potent source of support to a currency when those interest rate rises are a response to an economy that is enduring such strength that it risks overheating.

But the UK is not displaying any signs that such economic outperformance is on the horizon, meaning the Bank will feel it can sit on lower rates for longer.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

Economists are broadly of the view that the UK will soon return to pre-Covid levels of GDP, with some saying this could be achieved as early as year-end.

Berenberg's Pickering says the economy is on track to achieve this milestone in the first quarter of 2022.

"While the slight miss in Q3 highlights the downside risk to our 2021 projection of 6.9%, it does not alter our mostly positive medium-term view on the UK. We continue to project robust real GDP growth of 5.0% in 2022 and 2.3% in 2023. Our calls are likely to be in line with consensus over the three years once the market’s projections are updated for the Q3 miss," says Pickering.

"Admittedly the economy faces a number of well publicised headwinds. Higher inflation risks constraining household purchasing power, while supply shortages remain a constraint in a number of areas. That said, it is likely that consumer spending will be cushioned by levels of excess savings across households in aggregate," says Shaw.

Investec expect the Bank of England to raise interest rates in December to 0.25%, although next Tuesday's labour market data will contain important information on the impact of the ending of the furlough scheme for the Bank to mull over before making a final call.