- UK economic rebound cools sharply show PMIs

- GBP/EUR softer as Eurozone PMIs look better

- But global factors allow GBP/USD higher

Image © Adobe Stock

- Market rates at publication: GBP/EUR: 1.1640 | GBP/USD: 1.3652

- Bank transfer rates: 1.1414 | 1.3370

- Specialist transfer rates: 1.1560 | 1.3550

- Get a bank-beating exchange rate quote, here

- Set an exchange rate alert, here

The British Pound started the new week in decidedly mixed fashion amidst signs that the country's economic rebound slowed in August.

The Flash PMI reading from IHS Markit showed a greater-than-expected slowdown in UK economic growth rates with the Services PMI reading at 55.5 against the market's expectation for 59.0. This marks a slowdown on July's reading of 59.6.

UK private sector companies experienced a sharp slowdown in output growth during August, said IHS Markit.

While any reading above 50 suggests growth, the disappointment ultimately has implications for currency market sentiment.

There was some better news from the Manufacturing PMI which read at 60.1 vs. expectations for 59.5 and a previous reading of 60.4.

But the better-than-expected outcome for the manufacturing sector will prove minimal given the heavy weighting of services in the UK economy.

The Composite PMI - which calibrates the two readings to give a better shot of the overall economy - read at 55.3, which is down on the expected 58.4 and July's 59.2.

Survey respondents widely reported constraints on business activity due to staff shortages and supply chain issues.

Analysis of comments provided by survey respondents to IHS Markit suggested that incidences of reduced output due to shortages of staff or materials were fourteen times higher than usual and the largest since the survey began in January 1998.

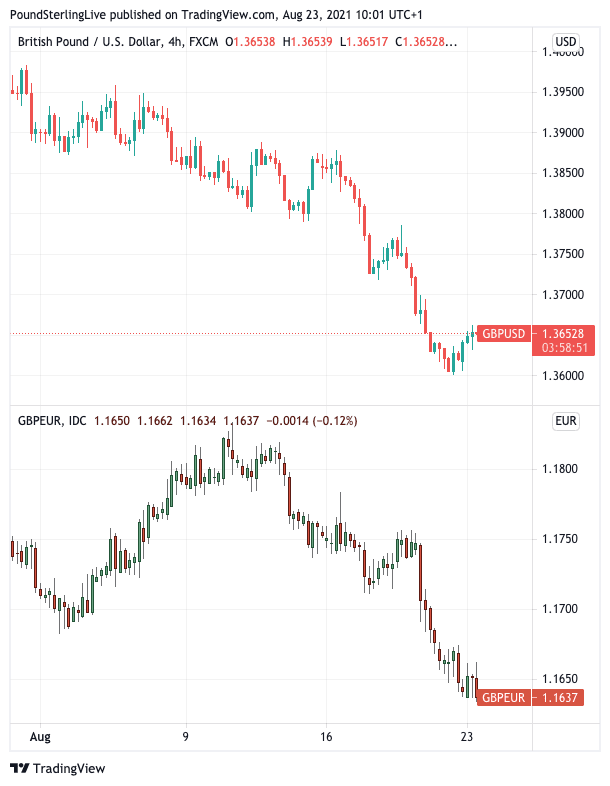

Following the data the Pound was seen to be holding a daily gain on the Dollar, reflecting the slight improvement in global investor risk sentiment a the start of the new week.

The Pound-to-Dollar exchange rate rose to 1.3657 despite the disappointing domestic data, confirming global factors will remain of importance to the wider currency market over coming days.

"GBP/USD rebounded to 1.3650. However, GBP/USD risks falling further this week if USD strength remains a dominant theme in currency markets," says Kevin Xie, Senior Asia Economist at Commonwealth Bank of Australia. "GBP could test its 20 July low of 1.3572 this week and so hit our end Q3 21 forecast of 1.3600 slightly early."

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

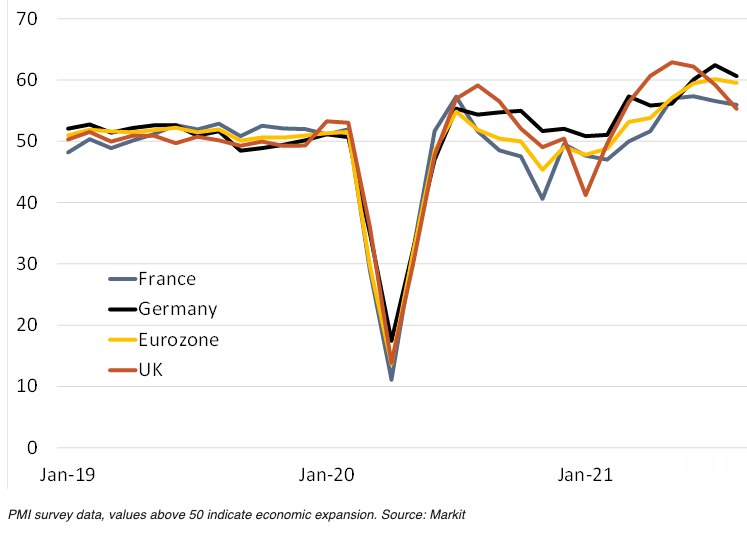

The market does however appear to be taking some notice of the PMI data with regards to the Eurozone vs. UK dynamic.

Eurozone PMI data came out half an hour ahead of the UK release and showed the bloc to have outperformed the UK in August, an outcome that might be keeping the Pound-to-Euro exchange rate under some pressure.

The pair is unchanged at 1.1642 at the time of writing, meaning the Pound has been unable to recover any of the losses suffered over the previous two weeks despite an uplift in global investor sentiment.

Here is how the UK and Eurozone's PMIs compare:

Above: Composite PMIs compared, image courtesy of Berenberg Bank.

Composite:

United Kingdom 55.3 vs. Exp. 58.4 (Prev. 59.2)

Eurozone 59.5 vs. Exp. 59.7 (Prev. 60.2)

Germany 60.6 vs. Exp. 62.2 (Prev. 62.4)

France 55.9 vs. Exp. 56.3 (Prev. 56.6)

Services:

United Kingdom 55.5 vs. Exp. 59.0 (Prev. 59.6)

European Union 59.7 vs. Exp. 59.8 (Prev. 59.8)

Germany 61.5 vs. Exp. 61.0 (Prev. 61.8)

Flag of France 56.4 vs. Exp. 57.0 (Prev. 56.8)

Manufacturing:

United Kingdom 60.1 vs. Exp. 59.5 (Prev. 60.4)

European Union 61.5 vs. Exp. 62.0 (Prev. 62.8)

Germany 62.7 vs. Exp. 65.0 (Prev. 65.9)

France 57.3 vs. Exp. 57.3 (Prev. 58.0)

In response to the data, Samuel Tombs, Chief UK Economist at Pantheon Macroeconomics says the PMI data might not be giving a complete picture of how the economy performed in August.

"Most high frequency indicators suggest that the recovery stalled in July but has regained some modest momentum this month. PMIs feel about a month out of date," he says.

While the UK economy has seen growth rates start to come down there are still some positives to latch onto, with IHS Markit saying efforts to rebuild capacity and strong optimism towards the business outlook contributed to the fastest rise in employment numbers since the index began in January 1998.

And backlogs of work increased for the sixth month in a row as businesses struggled to keep up with customer demand.

Given demand is there should serve to limit some of the negativity implied by the headline misses reported for August.

New order growth eased only slightly in August, with stronger export sales helping to cushion a slower recovery in domestic demand.

Resilient new business volumes contributed to another accumulation of unfinished work, although the latest rise in backlogs was the weakest since April.

But it is the job creation that will offer a significant source of support to the Pound going forward in that it suggests the economy is using up any of the slack created by the shock of the Covid crisis.

The utilisation of this slack suggests wage pressures might continue to grow over coming weeks amidst falling unemployment and strong demand for staff.

This could maintain pressure on the Bank of England to raise interest rates in 2022, which is some two years ahead of when the market expects a similar move from the European Central Bank.

This fundamental dynamic could offer the Pound ongoing support against the Euro.

With regards to the Dollar the outlook is less assured given the U.S. currency is showing a tendency to win in all market conditions.

"The USD has re-emerged as a high-yielding safe-haven currency that tends to outperform during bouts of risk aversion thanks to its superior liquidity but also does well during risk on thanks to the relative resilience of the US economy," says Valentin Marinov, Head of FX Research at Crédit Agricole.

The Federal Reserve is expected to announce it will start reducing its quantitative easing programme in either September or November, which will pave the way to a rate hike in late 2022.

With the Bank of England and the U.S. Federal Reserve both likely to raise rates in the same year there is no immediate advantage to either the Dollar or Pound on the basis of interest rates alone.