Above: File image of Jonathan Haskel. Image copyright: Pound Sterling Live, Still Courtesy of Imperial College Business School.

- Market rates at publication: GBP/EUR: 1.1630 | GBP/USD: 1.3690

- Bank transfer rates: 1.1410 | 1.3408

- Specialist transfer rates: 1.1550 | 1.3595

- Get a bank-beating exchange rate quote, here

- Set an exchange rate alert, here

A member of the Bank of England has said he believes it is too soon to consider raising interest rates in the UK in what amounts as a pushback to those colleagues who say rates might soon need to rise.

Jonathan Haskel, External Member of the Bank's Monetary Policy Committee (MPC) said the rise of the Delta variant of Covid-19 combined with the ending of government support schemes means the Bank must remain risk averse and keep its generous settings in place.

"The risk of a pre-emptive monetary tightening curtailing the recovery continues to outweigh the risk of a temporary period of above-target inflation. For the foreseeable future, in my view, tight policy isn’t the right policy," said Haskell.

In an online webinar to the University of Liverpool Management School Haskel was however optimistic in that he believes the economy would not suffer lasting damage due to Covid-19 restrictions and the labour market outlook has improved considerably in 2021.

Haskel's views are just the latest to come from the Bank over the course of the past week, with fellow MPC members Michael Saunders and Dave Ramsden both making the case for the timing of the first interest rates rise to be brought forward.

The views of Saunders and Ramsden triggered gains in the Pound exchange rate complex in the previous weeks as investors reacted to a potential shift in Bank of England stance.

Both Ramsden and Saunders fear levels of inflation above 2.0% could become entrenched if the Bank kept current settings in place for too long.

The Bank is tasked with ensuring inflation remains near 2.0%, but with inflation already running above this target and the Bank expecting inflation of 3.0% this year, it risks missing its target by a wide margin.

Indeed, Saunders last week said inflation could go as high as 4.0%.

Haskel does acknowledge that the labour market outlook has improved considerably in 2021 and the measures of labour market mismatch are falling.

"The anticipation of improved supply brings demand forward now and might add to inflationary pressure," he said.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

However, Haskel seems intent to push back against any call for higher interest rates and the imminent ending of quantitative easing, a view that on balance dampens support for the Pound.

Haskel did however sound an upbeat tone on the outlook saying his calculations suggest impact of the scarring lefty on the economy by the pandemic crisis is small and indeed there could be "no scarring at all and even a boost to potential output relative to pre-pandemic."

"Of course, these calculations rely on all manner of assumptions. But the comparatively low numbers are founded on the observation that the pandemic has been combatted not only by the vaccines but also highly accommodating fiscal and monetary policy," says Haskel.

"Had there been no such response, it seems highly likely that scarring would have been much worse," he adds.

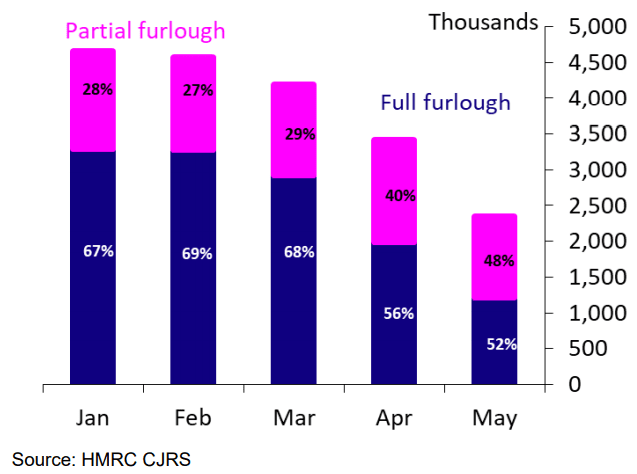

Above: The numbers on job support continues to fall.

Haskel maintains an upbeat view on the outlook for the economy saying economic output is expected to recover faster than economists had previously expected and he acknowledged forward-looking data is consistent with a continuation of the recovery.

But he says inflation is unlikely to remain at elevated levels, in part because the 'base effect' would ultimately pass.

The base effect refers to the jump in inflation when compared to the year prior: recall prices fell sharply as economic activity declined in response to lockdowns.

This therefore tends to over-exaggerate headline inflation figures.

He says high inflation will prove to be a temporary phenomenon as was the case following the Brexit referendum and the spike in 2011 when inflation rose in response to high global oil prices.

Finally he says there is a case to keep monetary policy settings as 'easy' as possible owing to the surge in the Delta variant of Covid-19, a clear sign that he will be amongst those arguing for settings to remain unchanged until the pandemic fades.

"It is important to remember that even if the future looks brighter, we are at the moment fighting to get back to where we were and we are not there yet. The Delta variant currently spreading exponentially in the UK

has an R number of 1.5," says Haskel.

Haskel also picks up on the number of workers being taken out of the economy by the NHS Covid-19 application that requires people to isolate if they have been around a person who has since tested positive for Covid-19.

"New variants can knock us off course. The possibility of further mutant strains, pressures on the NHS and many “pinged” workers make our path to recovery fragile," says Haskel.

Haskel would also like to see how the economy responds to the removal of government assistance over coming weeks, most notably the ending of the jobs support scheme.

"The economy is fully not recovered yet and faces two headwinds over the coming months: the highly transmissible Delta variant and a tightening of the fiscal stance," says Haskel.

"Against this backdrop, risk-management considerations lean against a pre-emptive tightening of monetary policy until we can be more sure the economy is recovering in a manner consistent with the sustained achievement of the inflation target. For now, tight policy is not the right policy," he adds.