What happened? The Pound fell sharply

Why? Markets appeared to have been expecting more from the BoE

Will the weakness last? It could be short-lived

Why? Some investors got ahead of themselves expecting an unrealistically 'hawkish' set of guidance. What was delivered was no 'game changer' to broader expectations.

Image © Adobe Stock

- Market rates at publication: GBP/EUR: 1.1660 | GBP/USD: 1.3922

- Bank transfer rates: 1.1430 | 1.3630

- Specialist transfer rates: 1.1580 | 1.3825

- Get a bank-beating exchange rate quote, here

- Set an exchange rate alert, here

The British Pound was sold in the wake of the June Bank of England decision that signalled little fundamental change in direction in UK monetary policy, but a number of noted foreign exchange analysts we follow say the currency will unlikely suffered a significant and enduring setback as a result.

The Bank of England (BoE) upgraded their GDP growth and inflation forecasts but offered little tangible evidence policy makers were itching to hike interest rates, and this apparently disappointed some participants in the currency market that were looking for a 'hawkish' shift.

Indeed, sifting through the substantial post-BoE analysis that has since become available it is clear the Monetary Policy Committee (MPC) did not stray to far from the expectations held by economists and analysts ahead of the event.

But the decline of the Pound on what was an essentially steady-as-she goes policy event suggests some in the foreign exchange market were looking for clear signs that a rate rise will be delivered at some point in the next 12-18 months.

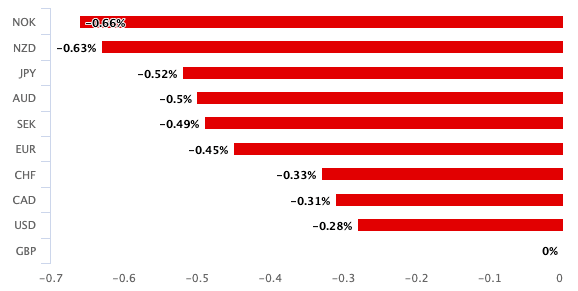

Above: GBP lost ground against all its major peers on June 24.

Kamal Sharma, a foreign exchange market strategist with Bank of America, says the Pound had lofty expectations heading into the BoE event.

"Price action immediately following the BoE rate decision suggests that the bar for a hawkish surprise was high," says Sharma. "MPC member Haldane duly delivered his opposition to a continuation of asset purchases, but markets clearly wanted more members to follow suit."

The drop in the value of Sterling therefore looks like a reality adjustment by an out of kilter section of the market and there is little suggestion that a 'game changer' from a currency perspective has been delivered.

"That GBP is lower in the aftermath of the decision is symptomatic of a market that perhaps expected too much, too soon from the Bank of England," says Sharma.

Despite the initial sharp drop, "the pound remains relatively well bid," says Paul Spirgel, a Reuters market analyst. "Sterling could hold within its recent ranges".

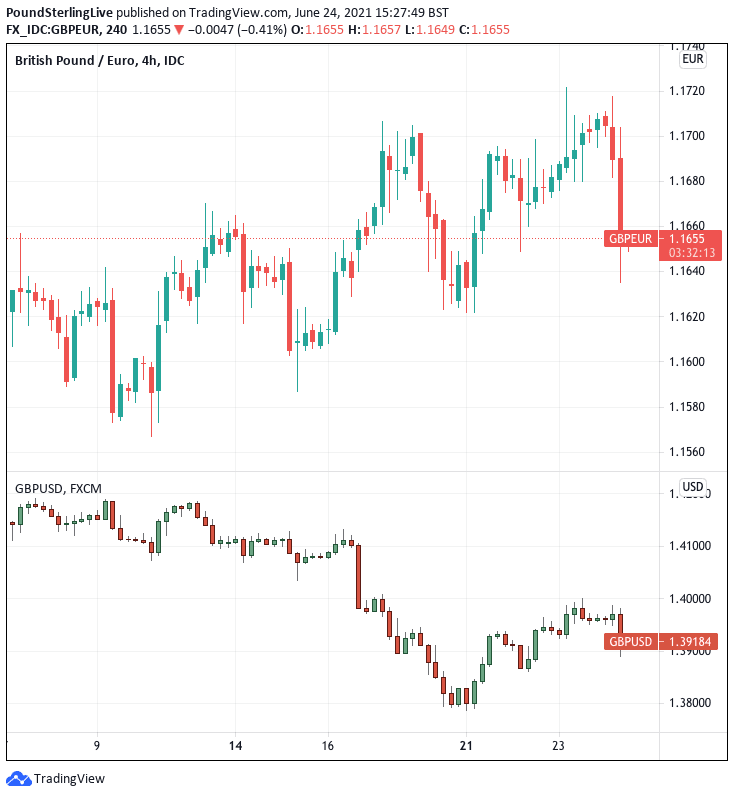

Above: Four hour chart showing dip in wake of BoE event (GBP/EUR top pane, GBP/USD lower pane).

The Pound-to-Euro exchange rate (GBP/EUR) dropped to a low of 1.1635 in the wake of the event before consolidating, having been as high as 1.1717 in the preceding hours.

The Pound-to-Dollar exchange rate meanwhile post a low at 1.3889 having been as high as 1.3986 earlier in the day.

Sharma sees no change in stance from the MPC and as such, "the post-BoE decline in sterling should not be seen as somehow existential".

Indeed, there were a number of supportive developments such as the upgrade to 2021 GDP forecasts.

The BoE now estimates that total economic output will be only around 2.5% below the level prevailing at the end of 2019, despite the economy having contracted 9.9% last year when ‘non-essential businesses’ spent around four months with their doors closed in an effort to contain the coronavirus.

The BoE also said inflation could rise above 3% in the near term, although they hastened to add that rise would ultimately prove temporary.

"The MPC now thinks CPI inflation could exceed 3% this year, with the risk of an even bigger overshoot of the BoE’s 2% target," says Martin Beck, Lead UK Economist at Oxford Economics, "However, the majority on the committee maintained the view that higher inflation will be transitory."

{wbamp-hide start}{wbamp-hide end}{wbamp-show start}{wbamp-show end}

The MPC says the direct impact of rises in global commodity prices will be the main driver of higher inflation, and they expect this to be a temporary phenomenon.

The MPC’s central expectation is that the economy will experience a temporary period of strong GDP growth and above-target CPI inflation, after which growth and inflation will fall back.

"The position that inflation will likely prove transitory and the lack of any shift in the guidance on asset purchases deflated the mild buildup of hawkish expectations and took sterling back lower in the wake of the meeting, as it is clear we’ll need to wait for more incoming data to get a more notable adjustment in the bank’s guidance," says John Hardy, Head of FX Strategy at Saxo Bank.

But economists at Barclays say they read the BoE as maintaining an outright cautious stance designed to ensure they avoid strangling the economy's recovery with an unintended tightening of monetary conditions.

"While acknowledging the recent, mostly upside, surprises to its short-term outlook, the MPC appears firmly cautious regarding the outlook for monetary policy, arguing that "Policy should both lean strongly against downside risks to the outlook and ensure that the recovery was not undermined by a premature tightening in monetary conditions," says Fabrice Montagné, Senior European Economist at Barclays.

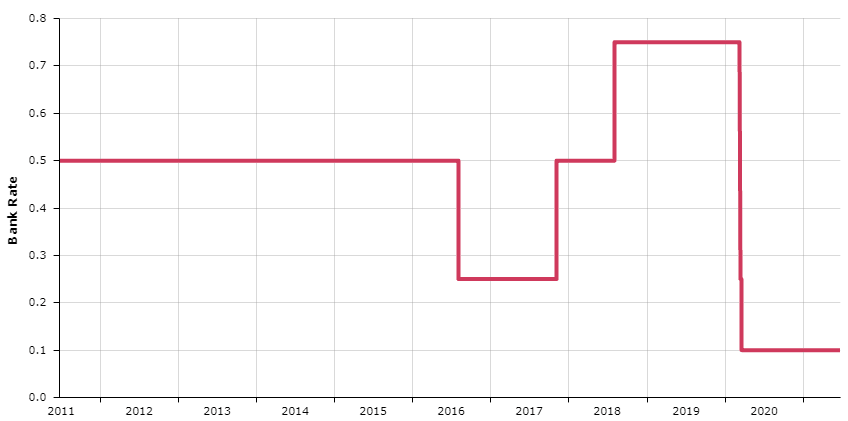

Above: BoE's Bank Rate and changes since 2011.

Barclays believe that today's balanced rhetoric is well aligned with their expectation of unchanged interest rates through 2022.

Capital Economics says the MPC can run the economy hotter for longer (i.e. provide easy money to boost growth) without generating a sustained rise in inflation.

"As such, we think the MPC may not tighten policy until well after the mid-2022 date assumed by the markets, perhaps even as later as 2024. And at that point, we think it will tighten by unwinding some QE before raising interest rates. So interest rate hikes may still be a couple of years away," says Dales.

Economists at ING Bank meanwhile expect the first interest rate rise to come in 2023, "at the earliest".

Should the BoE align with the above views and only deliver a rate rise in 2023 then at some point there will be an adjustment lower in expectations given the market is currently primed for a 2022 hike.

This readjustment would necessarily see the Pound move lower.

Any readjustment would ultimately be the consequence of disappointing data, most likely softer-than expected inflation data and/or softer-than-expected employment figures.

Therefore the Pound will likely remain highly reactive to the monthly data releases through the second half of the year.