The UK's current account deficit widened substantially in the final quarter of 2020 as the demand for goods imports increased and earnings on investments abroad were hit by the covid-19 crisis, confirming a fundamental achilles heal of Pound Sterling valuation remains resolutely intact.

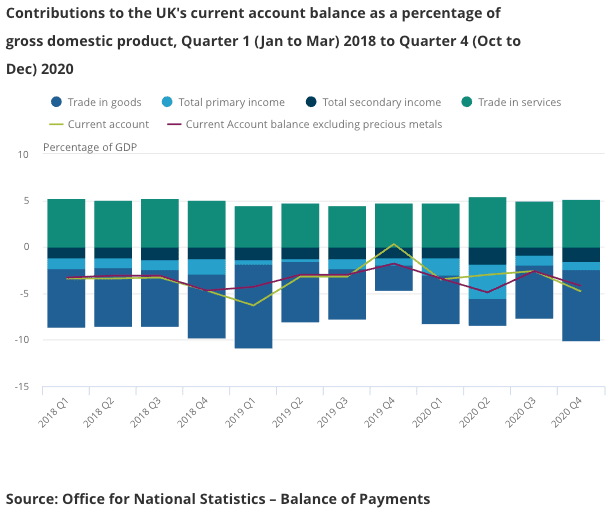

In the fourth quarter of 2020, the UK's current account balance excluding non-monetary gold and other precious metals widened "substantially" says the ONS, from a deficit of £13.8BN in Quarter 3 (July to Sept) 2020 to a deficit of £22.8BN in Quarter 4 2020 or 4.2% of GDP.

On an annual basis the current account deficit widened to £73.9BN in 2020 from £68.6BN in 2019. The UK's current account balance is a measure of the country's balance of payments with the rest of the world in trade, primary income and secondary income.

The ONS says the wider trade deficit was driven by a recovery in the import of goods into the UK as global trade started to recover from the lows of early 2020 and there was continuing evidence of stockpiling in preparation for EU exit after the end of the transition period on 31 December 2020.

The UK continues to maintain a surplus in the trade of services, but this surplus was diminished by government restrictions to combat the coronavirus pandemic, specifically in transport and travel services.

A current account deficit places the UK as a net borrower with the rest of the world, indicating that overall expenditure in the UK exceeds national income.

It means that the value of the Pound is to a degree reliant on the flow of capital into the UK from foreign sources, putting it at risk of shifts in global investor sentiment.

"The implication is GBP/USD will continue to trade at a discount to its fundamental equilibrium (around 1.5500) to attract long term investment flows and finance the UK’s current account deficit," says Elias Haddad, Senior Currency Strategist at Commonwealth Bank of Australia.

This contrasts to a country - for example Australia - which exports and earns more than it imports and spends abroad, thereby providing a solid fundamental base for the Australian Dollar.

"The UK must attract net financial inflows to finance its current (and capital) account deficit, which can be achieved through either disposing of overseas assets to overseas investors or accruing liabilities with the rest of the world," explains the ONS.

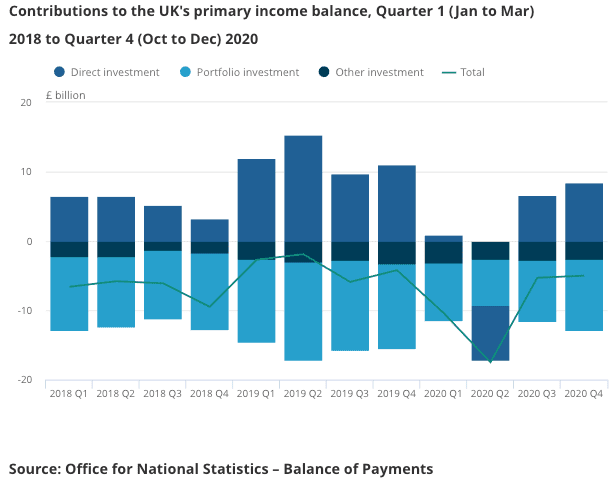

The UK's income accounts were meanwhile impacted in two ways in the final quarter:

1) earnings on investments abroad were more impacted by economic uncertainty because of the coronavirus (COVID-19) pandemic.

2) Payments to EU institutions increased as the UK reached the final year of the Multiannual Financial Framework (MFF) and to support the EU’s coronavirus response increasing the secondary income deficit to £28.2 billion in 2020.

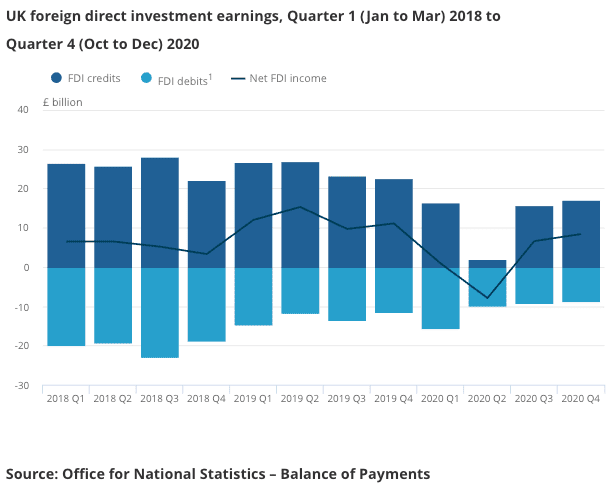

UK earnings on foreign direct investment abroad continued to recover in the fourth quarter of 2020 following a significant decline in the second quarter of the year, a time that coincides with the covid crisis market panic.

The ONS reported that money found its way into the UK as overseas investors returned to equities in the fourth quarter, as markets rallied and deposits from overseas banks increased.

The financial account component of the Balance of Payments recorded an increased net inflow of £38.7BN in the fourth quarter from a net inflow of £25.0BN recorded in the third quarter.

The ONS says the increase in the net inflow was because of foreign investors in the UK increasing their assets by £166.8BN while UK residents increased their foreign assets by just £128.1BN.

UK foreign direct investors meanwhile reduced their overseas equity holdings, leading to a net inflow of £13.1BN in Quarter 4 2020.

Looking ahead, a recovery in the UK economy from the covid-19 pandemic in 2021 is expected to ensure the country's current account deficit remains intact.

"We expect the current account deficit to widen to about 4% of GDP this year, from 3.5% in 2020," says Samuel Tombs, Chief UK Economist at Pantheon Macroeconomics.

Demand for imports is expected by Tombs to remain robust and therefore a persistent driver of the deficit:

"The U.K. economy likely will recover at a faster rate than the Eurozone’s this year, thanks to the accelerated rollout of vaccines. In addition, U.K. demand for imports is relatively insensitive to price rises - note that there was no import substitution after sterling’s big depreciation in 2016 - suggesting that higher prices for manufactured goods and raw materials will boost the value of imports."

Furthermore, he says a gradual recovery in global travel later this year will lead to the re-emergence of the U.K.’s trade deficit in tourism.