Image © Adobe Images

- Market rates at publication: GBP/EUR: 1.1680 | GBP/USD: 1.3940

- Bank transfer rates: 1.1450 | 1.3650

- Specialist transfer rates: 1.1600 | 1.3840

- Get a bank-beating exchange rate quote, here

- Set an exchange rate alert, here

Although the Pound failed to rally in the wake of the March Bank of England decision, the narrative surrounding the central bank and the economy over coming months will likely be supportive of the currency.

The British Pound rose sharply following the Bank of England's February meeting, but the currency's reaction to the March edition has proven to be decidedly less enthusiastic.

In February the Bank spurred Sterling higher by effectively banishing the prospect of negative interest rates in the UK, an expectation that contributed to the Pound's weakness for much of 2020.

But the negative interest rate story has now become a stale one and the foreign exchange market wants fresh fuel to drive the Sterling rally higher, which will most likely come in the form of rising expectations for an interest rate hike at some point in 2021 or 2022.

However, the Bank of England on Thursday emphasised interest rate hikes are still a long way away in the future, which appeared to deflate enthusiasm for Sterling.

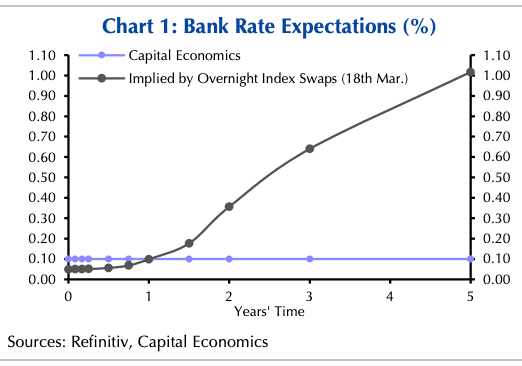

"Rates won’t rise next year as the markets expect. In fact, we think that rates could stay at +0.10% until 2026!" says Ruth Gregory, Senior UK Economist at Capital Economics.

This is an observation that will likely give those looking for a stronger Pound cause for thought as it suggests the market is too optimistic on its expectations for the economic recovery that lies ahead.

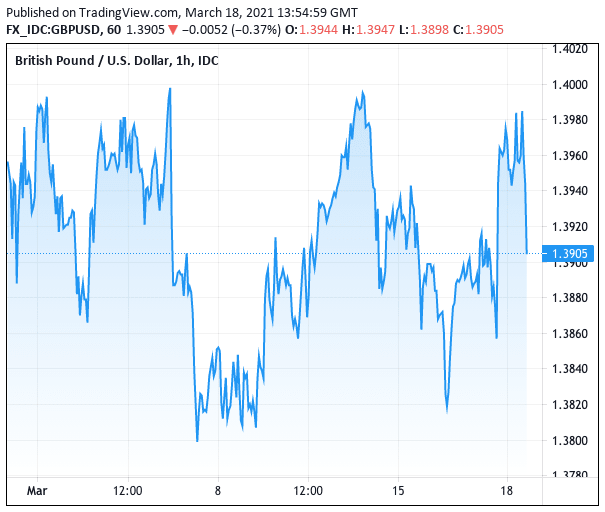

The Pound-to-Euro exchange rate had rallied to as high as 1.17 ahead of the meeting, a new one-year best. The Pound-to-Dollar exchange rate rallied back to 1.40, but both exchange rates turned softer following the release of the Bank's decision and guidance on the outlook.

Above: GBP/USD trade in March.

While the Pound did not rally, there are still however reasons to expect the Bank of England to remain a source of lingering support for the Pound, which will likely encourage Sterling buyers to remain invested.

"After the events of the past six weeks, the minutes had an upbeat feel to them," says Philip Shaw, an economist at Investec. "At this stage we are not inclined to shift our view that the next move in the policy rate will be a 25bp increase (to +0.35%) in Q4 2023."

A significant driver of global markets of late has been the rise in yields paid on government bonds, a sign that investors are factoring in higher inflation rates in the future.

Above: How the market thinks interest rates will move in the future vs. what Capital Economics think will be the case.

The rising yields can act against the objective of central banks by raising the cost of finance in an economy, therefore it is in the interest of central bankers to communicate and act in a way that keeps yields low.

A side effect of higher yields relative to those in other countries is a higher currency, therefore when central banks push back against higher yields the currency they issue can lose value.

In the case of the Bank of England, the desire to fight rising yields on UK government gilts is notably less urgent than might be the case at the U.S. Federal Reserve and European Central Bank, who have over the course of the past week also given their assessments.

"Crucially for markets, policymakers remained comfortable about the recent rise in gilt yields. Judging by the March meeting minutes, policymakers feel no urgency to lean against rising gilt yields with actions or words," says Kallum Pickering, Senior Economist at Berenberg Bank.

Why Yields Now Matter for Currencies: A Quick Explainer

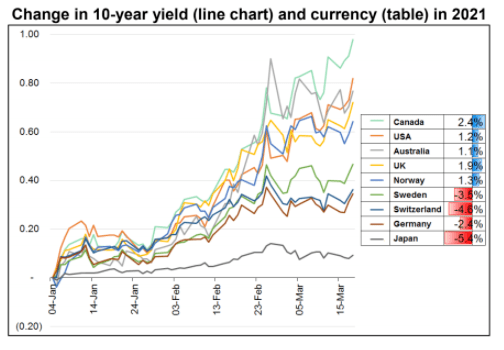

The chart below is from foreign exchange trader Brent Donnelly at HSBC. It shows the change in 10-year yields for the major developed countries (the main chart) alongside the performance of the associated currency (the blue and red table at right) for 2021.

The chart suggests the faster a country's ten-year yield rises relative to others, the stronger its currency is likely to perform. Therefore a central bank leaning against rising yields could act as a headwind to currency outperformance.

"One of the most notable developments in the six weeks since the MPC’s last meeting in early February has been a jump in global bond yields. In that time, UK 10-year gilt yields have risen from 0.35% to just short of 0.8% over that period. But unlike the ECB, which recently pledged to step up its asset purchases in response to higher long-term rates, the MPC took a hands-off approach in its latest policy statement," says Martin Beck, an economist at Oxford Economics.

Beck says the MPC remains "relatively nonplussed" and continues to see inflation returning "swiftly" to the 2% target in the spring, driven by base effects and recent increases in energy prices.

Crucially though, the Bank sees inflation expectations remain "well anchored" and expect the near-term pick-up in price pressures to be relatively short-lived.

"The monetary policy outlook continues, in our view, to be one of inaction for the next few years, with no rise in Bank Rate likely until 2024," says Beck.

The Bank of England might not have provided fresh impetus to the rally in Pound exchange rates, but they are unlikely to be a headwind over coming weeks given expectations for the UK economy to embrace a post-covid rebound.

"Growth hopes thanks to the UK’s aggressive vaccination strategy have driven the pound up recently," says David Alexander Meier, Economist at Julius Baer.

{wbamp-hide start}{wbamp-hide end}{wbamp-show start}{wbamp-show end}

The Bank of England acknowledged the UK's rapid vaccine rollout as being a driver of expectations for a rebound in economic activity, as well as the improved global picture.

Upside risks cited in the minutes to the meeting include:

- Improved global conditions relative to the February projections

- 'Substantial' new US fiscal stimulus

- Falling rates of Covid infections and hospitalisations in the UK

- Rapid vaccination progress;

- Faster easing of restrictions than had been assumed in February

- More near-term fiscal stimulus in the UK following the March budget

Should the UK economy outperform expectations over coming weeks and months and the impact of the crisis on jobs prove to be less severe than expected there is scope for the market to bring forward their expectations for an interest rate rise.

Such a development would likely prove supportive of the Pound, meaning foreign exchange markets will likely pay close attention to economic data releases over coming weeks and months.

However, Meier says he remains cautious on Pound Sterling due to Brexit headwinds, announced corporate tax hikes, and uncertainty surrounding the Scotland elections. "Therefore, we maintain our Neutral pound outlook for the time being".

Sterling will nevertheless likely find upside support if economic data outperforms expectations with employment and inflation data likely to prove the most important.

"While the MPC stopped short of explicitly saying that the markets had got ahead of themselves in expecting rate hikes from mid-2022, it once again stated that it won’t tighten policy until it is “achieving the 2% inflation target sustainably.” That means it’s not enough for the Bank to forecast inflation rising and staying above 2%, it needs to see that actually happen," says Gregory.

Capital Economics forecast inflation to undershoot the Bank's current forecasts, suggesting policy makers probably won’t contemplate reversing quantitative easing or raising interest rates until 2023/24.

"And even then, the Chancellor may be fretting about the effects of higher interest rates on the public finances and may come up with ways to convince the Bank to keep rates lower for longer," says Gregory.

She warns markets have gone too far in expecting interest rate hikes from mid-2022. "We think that rates won’t rise above their current rate of +0.10% until 2026. As a result, we doubt the 10-year gilt yield will increase much above 1.00% over the next two years."