- Three potential GBP scenarios

- BoE has been a source of support for GBP since Feb.

- But rising gilt yields could prompt a cautious message

Image © Adobe Stock

- Market rates at publication: GBP/EUR: 1.1667 | GBP/USD: 1.3966

- Bank transfer rates: 1.1440 | 1.3675

- Specialist transfer rates: 1.1585 | 1.3868

- Get a bank-beating exchange rate quote, here

- Set an exchange rate alert, here

The Bank of England (BoE) today delivers its latest interest rate decision and updates investors with its updated expectations for the economy, an event that could spark a notable move higher or lower in the British Pound.

The BoE decision comes at a point of growing confidence in the economic outlook owing to the country's rapid covid-19 vaccination programme that is expected to allow for a sustained unlocking of the economy and improved growth rates over coming months.

While investors are not expecting any changes to interest rates they will be keen to hear the BoE's thinking on when that next move on rates might occur.

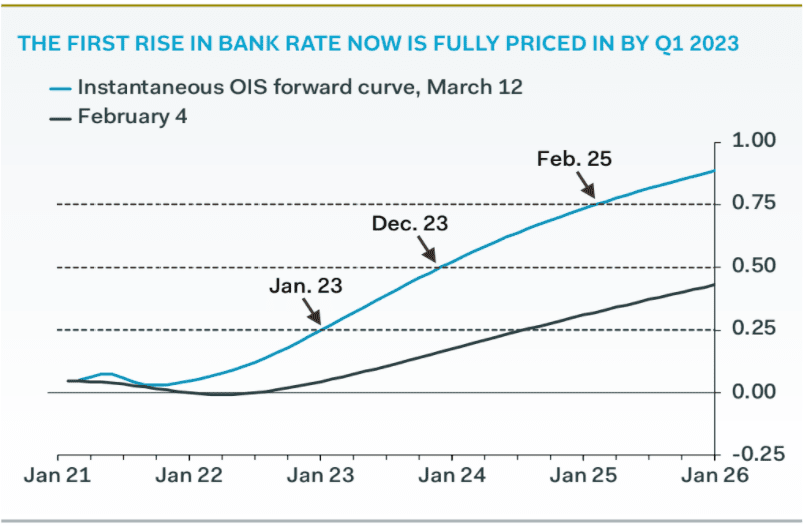

Currently money markets reveal investors to be pricing in a little over two rate hikes (over 50bps) by the end of 2023.

The rule of thumb from a foreign exchange perspective is that should this date come forward as a result of the BoE's communication today then the Pound rises, but should the BoE push back on this then the Pound would retreat.

The base-case assumption by one major foreign exchange analyst we follow is that the BoE event ultimately results in an extension of the current Pound Sterling rally, which could take the GBP/EUR exchange rate to as high as 1.1760.

And under another, albeit less-likely, scenario the rate could go as high as 1.1800, more details on this below.

Image courtesy of Pantheon Macroeconomics

A driving force behind the Pound's strong run in 2021 has been the rapid deletion of expectations for negative interest rates, something that accelerated following the February BoE meeting.

Now the assumption is the next move on rates will be to raise them which is a supportive development for the Pound, particularly when coming up against currencies where an interest rate rise remains a distant prospect.

This is particularly true of the Pound-to-Euro exchange rate given the European Central Bank's strong bias towards keeping monetary policy as supportive as possible for as long as possible.

Global financial markets have over recent weeks been caught up in an environment of rising bond yields, where the yield paid on government bonds rises as investors demand greater compensation for holding bonds as they eye strong inflation rates over coming months and years.

The rise in bond yields (or gilt yields) in turn pushes up the overall cost of finance in the economy and leans against any economic recovery.

Therefore the Bank of England will want to ensure they do not come across as being too hawkish and risk raising yields even further.

{wbamp-hide start}{wbamp-hide end}{wbamp-show start}{wbamp-show end}

A balancing act must be performed by the BoE which must somehow acknowledge an improved outlook, that could stoke higher inflation rates, while at the same time acknowledging such a message could be detrimental to current financial conditions.

"With many positives in the price of the GBP by now, we think that any concern about the latest rally in gilt yields and/or the GBP could be seen as a dovish surprise," says David Forrester, FX Strategist at Crédit Agricole.

Should the BoE push back on higher rates in its March statement the Pound could fall says according to Ned Rumpeltin, a foreign exchange strategist at TD Securities.

TD Securities say they envisage a 25% chance that the overall outcome of the event is 'dovish', whereby the statement raises concerns over the impact of tighter financial conditions of late.

Under such a scenario the BoE opts to keep the pace of Quantitative Easing (QE) unchanged but in its minutes reiterates that it can increase the pace of bond purchases under QE to safeguard the level of monetary stimulus if necessary.

Should this transpire the Pound-to-Dollar exchange rate is forecast by the investment bank to retreat to 1.3740 and the Pound-to-Euro exchange rate to 1.1590 (EUR/GBP 0.8630).

But the base-case assumption at TD Securities - given a 60% weighting - is that the forward guidance contained in the statement is left largely unchanged, though Governor Andrew Bailey and his team may mention the need to 'watch' or 'monitor' market interest rates.

"Risks around growth outlook are more balanced. Minutes should see 'some' or 'a few' MPC members more concerned about the premature rise in BoE market rate expectations on top of the GBP appreciation. At the same time, 'some' MPC members view the rise in longer-term rates as appropriate," says Rumpletin.

Under this scenario the GBP/USD exchange rate trades at 1.3865 and GBP/EUR rises to 1.1760 (EUR/GBP 0.8505).

A 'hawkish' scenario - given a 15% weighting by TD Securities - occurs where the BoE comes across as being optimistic about the outlook.

Rumpletin says the BoE expresses enough optimism for the statement to note that the rise in longer-term yields is appropriate given the diminishing downside risks to the growth outlook. The minutes would meanwhile reveal more concern from 'a couple' or even just 'one' MPC member.

Under this scenario the GBP/USD rises to 1.3940 and GBP/EUR to 1.1800 (EUR/GBP 0.8475).

The Bank of England might deploy a 'hawkish' stance if the thinking of its Chief Economist Andy Haldane hold sway.

Haldane has a track record for looking at the economy from a more optimistic standpoint than his peers, saying in February that central banks and markets might be too complacent in their expectations for future inflation levels.

"People are right to caution about risks of Central Banks acting too conservatively by tightening prematurely. But, for me, greater risk at present is of Central Bank complacency allowing inflationary (big) cat out of the bag," Haldane said in an online speech for the Bank of England.

Haldane said there is a significant amount of money sitting unused in bank accounts across the country owing to the covid-19 crisis, with households and companies now holding £400 billion of savings.

He said this money "will be seeking a new home, whether physical or financial assets or goods and services. This would provide a very significant degree of additional demand stimulus to an already rapidly-recovering economy."

"Inflation is the tiger whose tail central banks control. This tiger has been stirred by the extraordinary events and policy actions of the past 12 months. It is possible that, as vaccinations are rolled out and some degree of normality returns, inflation will return to a stable state of rest. Indeed, if risks from the virus or elsewhere prove more persistent than expected, disinflationary forces could return. But, for me, there is a tangible risk inflation proves more difficult to tame, requiring monetary policymakers to act more assertively than is currently priced into financial markets," he added.