Above: ECB President Mario Draghi is expected to oversee the end of quantitative easing in the Eurozone in 2018, a move that has prompted the Euro higher. Image (C) ECB.

The Euro has exceeded last year's highs and it's outlook has shifted positively following the release of the last ECB meeting minutes.

The Euro jumped against the Dollar in the wake of the release of the minutes to the European Central Bank's (ECB's) December meeting.

The Euro-to-Dollar exchange rate breached the key 1.2092 September high in decisive fashion on Friday, November 12, hitting a three-year high of 1.2115 against the Dollar at the time of writing.

Now the market has broken into new territory above the September high how much higher is is expected to go?

Commerzbank's analyst Karen Jones expected a break above 1.2092 to herald a continuation of the exchange rate higher to a target at 1.2168 initially:

"A rise above 1.2092 will target the 1.2168 50% retracement of the move down from the 2015 high and then the 1.2414 200 month ma," says Jones in a report this morning.

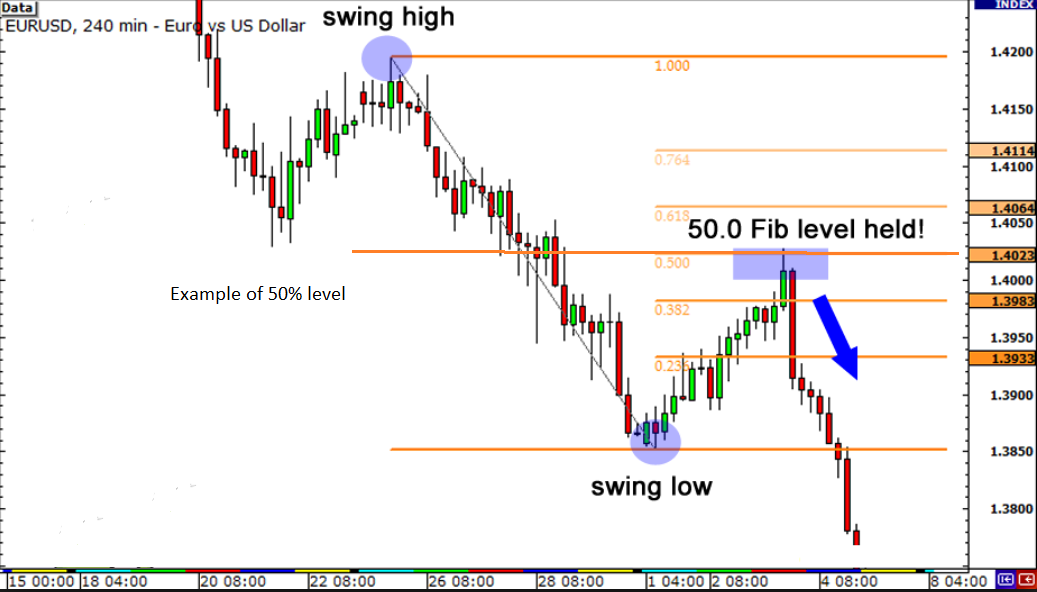

The 50% retracement refers to the midpoint of the previous rally which analysts consider a level of heightened significance.

"For reasons that are unclear, these ratios seem to play an important role in the stock market, just as they do in nature, and can be used to determine critical points that cause an asset's price to reverse," says Investopedia on the subject of Fibonacci retracements.

A break above the 50% level is also important because of the "overwhelming tendency for an asset to continue in a certain direction once it completes a 50% retracement," continues Investopedia.

(Example of a reversal happening at a 50% retracement level)

Too Strong for its Own Good

As the Euro goes from strength to strength analysts are already raising concerns it could be creating headwinds for its own advancement.

For example, the exchange rate has gone up so much in recent weeks it is quite a bit higher than when the ECB met in December.

"The greatest risk for the euro is how much those views reflect the ECB's current sentiment," says BK Asset Management's Managing Director Kathy Lien.

Indeed, the Euro's strength could in itself be a concern to the ECB.

When policy makers at the central bank last met, EUR/USD was trading at 1.18.

"This 4-cent rally in the currency could undermine the ECB's confidence especially as it coincides with a rise in German yields. Between the December 14th policy meeting and today, 10-year bund yields have risen from 0.3% to .57%. The stronger currency and rising yields is in many ways akin to a rate hike," notes Lien.

As market dynamics are very different today than 4 weeks ago, Mario Draghi's eagerness to change their guidance could be diminished as well.

Yet, "with that in mind, the near term trend for EUR/USD is higher and not lower as all of this is speculation until we actually hear from the Draghi," says Lien.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

What the European Central Bank Said

The ECB minutes come at a time of growing economic growth in the Eurozone which has the central bank confident that inflation will soon start rising to their 2.0% target.

This observation has seen the ECB indicate it will soon pare back its stimulus programme which has over recent years helped the Eurozone's economy but kept the Euro under pressure.

Two of the most notable points supporting a bullish EUR outlook were:

(1) “Incoming information and the December 2017 staff projections indicated a significant improvement in the growth outlook and continued economic expansion at a pace exceeding potential. Risks to the growth outlook continued to be balanced, with some upside risks in the near term.”

(2) “Looking ahead, the view was widely shared among members that the Governing Council’s communication would need to evolve gradually, without a change in sequencing, if the economy continued to expand and inflation converged further towards the Governing Council’s aim. The language pertaining to various dimensions of the monetary policy stance and forward guidance could be revisited early in the coming year. In particular, as progress was made towards a sustained adjustment in the path of inflation, the relative importance of the forward guidance on policy rates would increase.”