The Euro has been a force to contend with in 2017, rising from rock-bottom lows of 1.06 against the Dollar up to its peak around 1.21, but is it now a busted flush as some are saying or has it still got a joker to play?

The single currency could still go higher despite much ado over concerns that it's rapid rise could hamper economic growth, says Credit Suisse's Alvise Marino.

In fact, the recent pullback in EUR/USD from its 1.21 peak to around the 1.18 level has helped ease fears that Euro-strength might force the ECB to "swerve in a more dovish direction" in its monetary policy statement Thursday, writes Marino.

Unusually the Euro's rally following the French election coincided with a rise in Euribor futures and this decoupling from the usual relationship, which is negative relationship with bond prices, suggests rate hike expectations have been kicked down the road well into the future.

"We think this is consistent with the “lower-for-longer” bias in rates that emerges from recent ECB rhetoric," says Marino, by which he is alluding to the view that the ECB is nowhere near ready to raise rates, even if it is contemplating removing some stimulus from the table.

Marino recommends buying the Euro on "politically inspired dips" and although Italy's new electoral law was marginally negative for EUR/USD, and an Italian election looms at the start of 2018, one of the effects of the new electoral law is that it makes it much more difficult for an anti-EU party to come to power and implement a policy agenda in Italy's two houses of government.

This is as a result of an amendment to the rule relating to the 'majority premium' - now taken out -, which makes it harder for one party to gain an overall legislative majority.

"By removing the majority premium of its previous incarnation it improves the outlook for political forces willing to be parts of large coalitions," he says. "This, in turn, reduces the likelihood of a 5 Star Movement government, given the party’s stated aversion to coalition arrangements. We view this as a positive development for EUR/USD."

A lack of system-wide significance of the Catalan independence push means it will probably remain a side-show, at most, unless it begins to impact significantly on Spanish or Eurozone growth.

Current Account Surplus

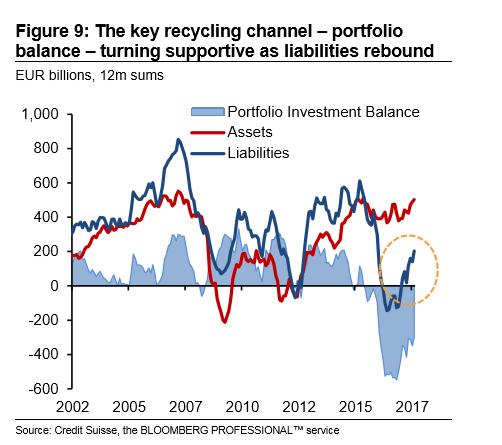

Marino notes how the current account surplus and demand from investors for European equities continues to drive the Euro higher, and this is reflected in the increase in EU firm's foreign liabilities which come from investment inflows.

"Specifically, foreign demand for European securities by foreign investors appears to have picked up sharply, as suggested by the surge in liabilities causing the net outflow in the portfolio balance to tighten considerably," he says.

The ECB's tapering of its scheme is likely to increase the current account surplus as QE led to a lot of purchases of assets outside of the EU and therefore was euro-negative from a flows perspective, yet that will not be a major driver anymore.

Choice of next Fed chair has pushed EUR/USD down since only two of the five candidates in contention (Warsh and Taylor) are hawks, so simply from a basic-probabilities point of view, there is less chance of one of them being picked.

It is also improbable that the President will want to appreciate the Dollar more than necessary given his desire to boost US export competitiveness, so he is probably not likely to choose a hawkish candidate for that reason if no other.

Scotiabank Notes European Equity Demand as Primary Driver for Euro

Analysts at Scotiabank meanwhile say the Euro is performing surprisingly well against the USD despite negative yield spreads and European political risk factors, yet knowing how highly correlated the two are, ask, how can this be?

"All else being equal, short-term—2-year—bond yield spreads between the Eurozone and the US reaching –228bps this week, the widest (most negative) differential since the EUR got underway, would represent a significant disadvantage for the EUR and grounds for expecting the EUR to weaken," says Scotia's Shaun Osborne in a recent research note to clients.

Yet these fair value models using spread regression as a core component all broke down after the French election as politics contaminated their purely quantitative basis.

"2017 was billed as a year of high political risk for the Eurozone, with key elections in the Netherlands, France and Germany seen as potential stumbling blocks for the European Union amid a rise in populist politics. To a very large extent, however, the political center in Europe has held and another crisis passed," says Osborne.

In short, the Eurozone has proven extremely resilient.

"The institutional strength of the Eurozone has been seriously tested in the past few years and has not buckled," says the analyst.

Much like Marino, he sees little disturbance to the Euro coming from Catalonia, and, we "suspect, and arguably, the EUR is now just one national election (Italy) away from a much smoother political ride," he says.

Investors piled into the Eurozone stock market after the risk of far-right party dominanting in Paris was subdued.

"With the risk of an anti-EUR President in Paris eliminated, investors clearly reassessed the Eurozone (and EUR) outlook. International investors piled into European equity markets and returns for foreign investors were turbo-charged by the rising EUR (+23% YTD in USD terms for Stoxx50 index versus +17% for the DJIA)."

Continued inflows from investors are expected to support the Euro, especially versus the Dollar, looking ahead.

"We note that broader trends in Eurozone net portfolio and foreign direct investment flows started to turn less negative through the turn of the of the year and (average) flows are strengthening again. Trends appear to support the recent rebound in the EUR versus the USD," says Osborne.

In fact overall there is more slack to be eaten up on this front as Osborne says international Investors are in still somewhat underexposed to the Euro.

"We think that international investors are perhaps somewhat under-exposed to the EUR, given the focus on this year’s round of elections and are starting to rebuild positions in EUR assets which will help support the EUR’s advance in the medium term," concludes Osborne.