Until quite recently EUR/USD has been seen in a strong uptrend after breaking above the 1.10 watershed before stalling towards the end of the previous week.

Analysts are now a little more positive on the Dollar than they are on Euro for the week ahead, as they expect robust payrolls data to cement the outlook for the US economy.

Moribund inflation data is meanwhile tipped to reinforce the sluggishness of Europe.

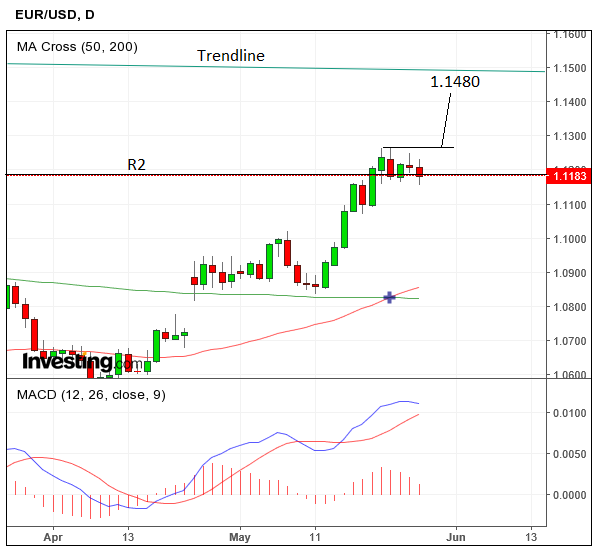

The pair has been in a shallow sideways consolidation, probably partly due to support from the R2 monthly pivot at 1.1186, which has helped prevent deeper penetrations.

Monthly pivots are levels on charts which trader’s use for positioning and trade management.

A break below the 1.1158 lows, however, would be a significant bearish sign and confirm that R2 had been breached, definitively and that we were going lower.

In the absence of such a break, however, we remain bullish since there is insubstantial evidence yet to suggest the short-term uptrend has finished, and a break above the 1.1268 highs would probably lead to a move higher to 1.1400 and then possibly 1.1480, where the trendline is later.

The gap in the market which occurred after Emmanuelle Macron won the first round of the French Presidential Election remains open which is unusual as markets have a tendency to close these gaps.

“Five weeks have passed since EUR/USD gapped up from 1.0730 to 1.0880. There is a saying that gaps are meant to be filled and after such a long period of time, traders are still itching to drive the pair lower,” said BK Asset Management’s Kathy Lien.

The reason it is still open is that it represents the level at which the Euro was pressured down by political risk in the Eurozone.

Following Macron’s decisive victory, however, that political risk has been dispensed with.

Data for the Euro

The main event for the Euro will be inflation data out on Wednesday, May 31 at 10.00 BST.

Inflation impacts on the policy decisions of the European Central Bank (ECB) which means that if it goes up substantially the central bank is more likely to raise interest rates (or normalise policy).

Higher interest rates strengthen a currency as they attract more flows of international capital.

The expectation for the data out on Wednesday is that inflation will fall to 1.5% from 1.9% year-on-year in May, but that this is more to do with an “Easter effect” than a real decline in underlying inflation.

“We look to Eurozone inflation to slip back to 1.5% y/y in May as the Easter effect falls out of the equation. This is below the ~1.75% rate that the ECB had forecast in March. And with core CPI falling back down to 1.0% y/y, we don’t think that the Eurozone is anywhere near a place yet where the ECB can declare a convincing upward trend in underlying inflation,” said Toronto-based TD Securities.

The other major release for the Euro in the week ahead is the Unemployment Rate out at 10.00 on Wednesday and is forecast to fall to 9.4% in April from 9.5% previously.

The release will be important given all the talk about the Eurozone economic recovery, and another fall in the Unemployment Rate will probably bolster this view.

“The near-term political risks have faded and the latest economic reports were positive for the euro – German investor confidence rose strongly in May, the Eurozone’s trade surplus hit a 3-month high and there was no revision to the Eurozone’s Q1 GDP and French CPI reports. Even ECB President Draghi acknowledged the euro-area recovery as resilient and increasingly broad based,” said BK Asset Management’s Kathy Lien.

Data for the Dollar

The most important release for the Dollar in the week ahead will be Non-Farm Payrolls (NFP) at 13.30 BST on Friday, June 2.

The consensus amongst analysts is that NFP’s will show another month of steady job gains, solidifying expectations of a June rate rise and thereby leading to a rise in the Dollar – fall in GBP/USD.

“In the U.S the publication of non-farm payrolls for May will attract the most attention. Jobless claims in the month fell to their lowest level since the 1970s, suggesting a decline in layoffs. As for hiring, Markit’s composite PMI reported the fastest rate of job creation in three months in May. Based on these indicators, we expect payrolls to have risen by about 185K, lower than April’s increase but still a very good number considering it is becoming increasingly difficult for American firms to find qualified workers,” said NBF Economics at Strategy.

The other major release from the US will be the Personal Consumption Expenditure Deflator or Index (PCE), which is out at 13.30 on Tuesday, May 30.

The index is expected to show annual growth of 1.7% and 1.5% for Core.

Compared to the previous month Core PCE is expected to have risen 0.1% from -0.1% in March.

The PCE is the Federal Reserves favoured inflation gauge so its results will impact on the Dollar if they are substantially out of whack with expectations.