A spike in implied volatility on the EUR/USD pair confirms markets are growing nervous of Donald Trumps ascent in the polls. But, we also hear markets will eventually learn to love a Trump presidency.

Donaly Trump's manifesto and agenda mark a radical departure from the issues US Presidential candidates would traditionally run on.

Even if a President Trump would be unlikely or unable to push through all the radical ideas he has mooted on trade (e.g., leaving NAFTA, leaving the WTO), the market would nonetheless need to price in some risk of a push in that direction.

Surveys suggest businesses may not want a populist president given the extra policy uncertainty that could be generated, posing downside risks to business investment – and by extension Fed hiking probabilities – into the election period.

What we have here is a mix of uncertainty - and currencies don't like uncertainty.

Just ask a post-Brexit vote Britain.

Therefore, global foreign exchange markets could enter a period of volatility should Trump win.

According to the latest analysis on the matter, such an outcome might hurt the likes of CAD and MXN vs USD.

However, it could also weigh on USD itself vs more defensive currencies like EUR, CHF and JPY, or even distant but "super AAA" AUD.

"As far back as March, we raised the idea of "Trumpxit" – the risk that the US economy disengages from the global economy – as a material issue that the market would have to contend with as the election approaches," says Shahab Jalinoos, a research analyst with Credit Suisse.

Credit Suisse feel that the current market expectations for a US Federal Reserve interest rate rise for 2016 seem reasonable based on the prospect of heightened uncertainty leading into November.

The July 27th FOMC statement noted that, "on balance, payrolls and other labor market indicators point to some increase in labor utilization in recent months" while "household spending has been growing strongly."

However, market enthusiasm for an impending rate rise was offset by the more sombre observation that, "market-based measures of inflation compensation remain low; most survey-based measures of longer-term inflation expectations are little changed, on balance, in recent months."

There is therefore a growing risk to Dollar bulls that the delay to higher rates is kicked further into the distance as political uncertainty grows over coming months.

Credit Suisse argue that "Trumpxit" risk might hurt the likes of CAD and MXN vs USD, but it could also weigh on USD itself vs more defensive currencies like EUR, CHF and JPY, or even distant but "super AAA" AUD.

After a long period of ignoring this issue (MXN aside), there are signs that the market is taking the risk of FX volatility induced by the presidential election more seriously.

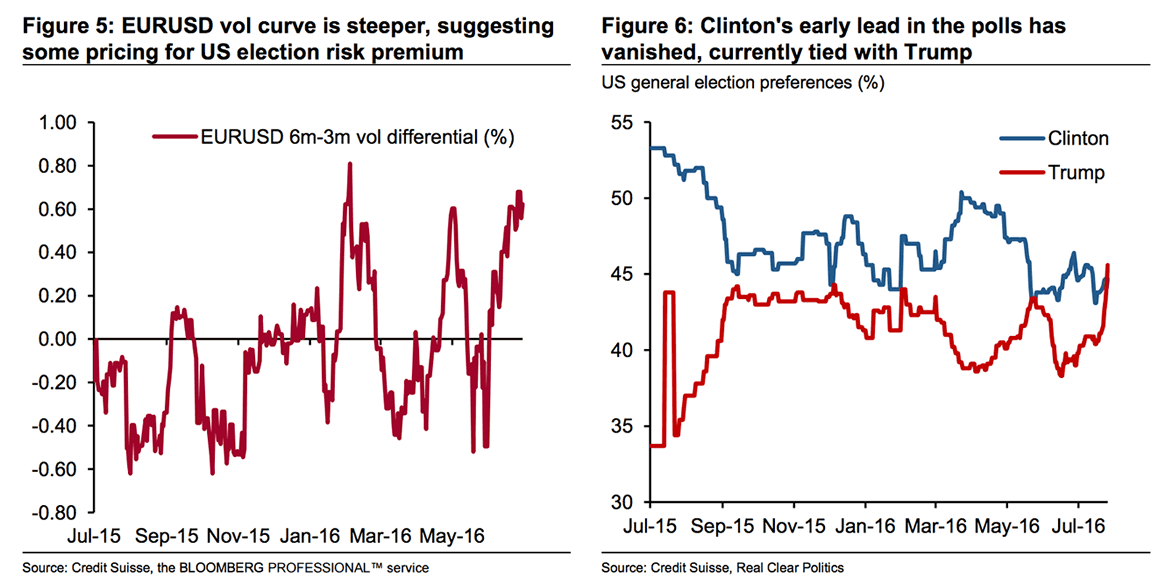

For example, Credit Suisse observe that the EURUSD 3m v 6m vol spread is now pricing in a decent premium for 3m implied volatility in 3m time – albeit off a very low base for 3m implied volatility:

This tells us that the cost of insuring against volatile movements in the EUR/USD at around the time of the election have risen sharply.

This implies that markets see a Trump victory as being more likely. Indeed, polling data shows Trump catching up with Clinton.

"It is still very early days for this phenomenon – we suspect it won't really pick up properly until a) we are still closer to November and b) the polls shows a strong chance of a Trump victory at that time," says Jalinoos.

How to Position for a Trump Victory

Credit Suisse strategists believe markets are pricing in a US election risk premium in USDMXN, but not in USDCAD.

"We think this represents a mispricing, as CAD is also vulnerable to potential risks to its external trade outlook," says Credit Suisse's Alvise Marino.

Strategists are long a 2 August 2016 1.32 USDCAD call in their recommendation portfolio, and would look to hold on to the spot position if the option were to be exercised at expiry.

Strategists also recommend buying a 4m dual digital structure that pays off if USDCAD exceeds 1.3615 (103% of a spot ref of 1.3218) and if AUDUSD exceeds 0.7514 (100% of spot ref 0.7514).

The risks to the trade are limited to the upfront premium.

"We also recommend buying a 15 November 2016 expiry USDMXN call spread struck at 19.50 and 20.50 for 1.21% premium (spot ref 18.78). The trade offers a 4.2:1 max payout and the risks to the trade are limited to the upfront premium," says Marino.

Markets Will Eventually End up Liking Trump

We saw an initial 'shock reaction' by markets to the Brexit vote, but a stabilisation in Sterling, stocks and confidence has materialised one month on.

Could markets adopt a similar tone to a Trump victory in 2016?

John Redwood, Chief Global Strategist at brokers Charles Stanley, says this pattern could well be repeated.

"After an initial bout of unhappiness should he win, markets will turn to liking the aggressive tax cuts and the deals oriented approach to trade and investment. He states his tax changes would be neutral, but in the early days it could well be a substantial fiscal stimulus before the extra revenues from lower rates materialise as he hopes," says Redwood.

Trump remains the underdog, but Redwood believes he could win from here.

"He seems to have most traditional republicans on board, and he is making an audacious pitch to disgruntled Democrats, many of whom voted for Mr Sanders in their primaries. I also think that He is seeking to offset early revenue loss with a major drive to repatriate profit and cash to the USA by multinational US corporations," says Redwood.