The vast flows of investor money out of Eurozone fixed income is happening and will continue to happen and in doing so will drive down the EURUSD conversion argues Deutsche Bank.

Analysts at Deutsche Bank have confirmed their warnings that the euro to dollar exchange rate will decline significantly over the longer-term as investors seek higher returns .

Notably, analysts at the German bank have confirmed they will stand by their Euroglut thesis despite high-level criticism from peers.

In October 2014 Deutsche Bank introduced their “Euroglut” hypothesis in which it was predicted a wave of European capital outflows to the rest of the world would keep Eurozone yields unusually low and cause dramatic euro weakness despite the region’s large current account

The theory has drawn criticism since it was launched with a key argument made by the New York Federal Reserve who assert the 'Euroglut' theory ignores balance of payments accounting.

According to Thomas Klitgaard and David Lucca at the New York Fed, balance of payment accounting, "requires any financial outflow from the euro area to be matched by a similar-sized inflow, absent a quick and substantial current account improvement."

As such the impact on the exchange rate is essentially neutralised.

Furthermore the Fed authors suggest the focus on cross-border financial flows also is misguided since, according to asset pricing principles, the euro and global asset prices can move without any change in financial outflows.

Deutsche say Euroglut is Real

In the wake of the criticism, the theory's author, Deutsche Bank's George Saravelos, has taken time to review the evidence at hand.

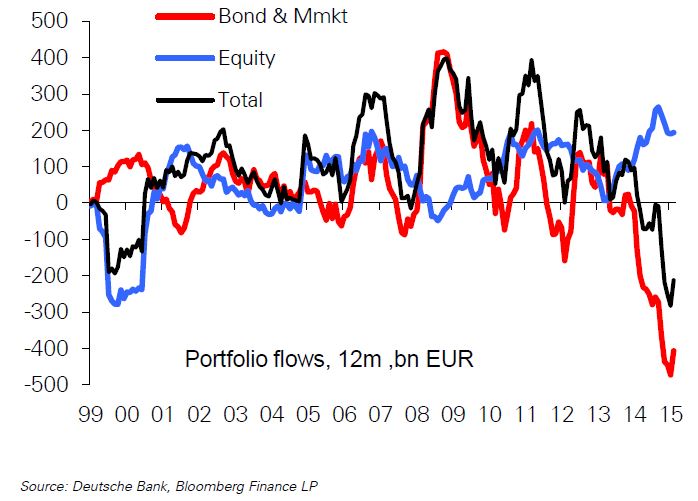

"We show that 'Euroglut' is no longer a hypothesis but a reality: the Eurozone has experienced an historically unprecedented shift in portfolio flows, with net fixed income outflows running at a staggering 500bn EUR over the last twelve months, the largest on record," says Saravelos in defence of his forecast model.

Deutsche Bank's analysis suggests flows are mostly directed towards US bond markets and have exceeded the Eurozone’s current account surplus.

Above: Record European portfolio outflows, all fixed income.

The ECB has engineered the massive outflow of money by slashing interest rates and expanding its balance sheet, in the process making investing in Eurozone fixed income unnattractive.

"They have pushed the basic balance into deficit over the past year contributing to EUR/USD weakness," says Saravelos, torpedoing Klitgaard and Luca's assertion that, "any financial outflow from the euro area be matched by a similar-sized inflow."

The natural destination for this displaced money has been the United States, a flow that has boosted demand for dollars and bid down the euro.

Looking ahead, Deutsche Bank believe Euro-area portfolio outflows will likely remain in the driving seat for years to come as core Europe’s (mostly Germany’s) vast savings are deployed overseas, while American and Asian investors retreat from European assets.

Furthermore, Quantitative Tightening, the reserve draw-down by the major central banks in emerging markets, has only helped to accelerate this process.

Euro Forecast to Fall Well Below Parity

With the ECB expected to announce an extension of this programme at their December meeting one would assume this dynamic will continue.

But, bearish pressure on the euro from this structural adjustment is therefore likely to continue irrespective of how much easing the ECB delivers in December.

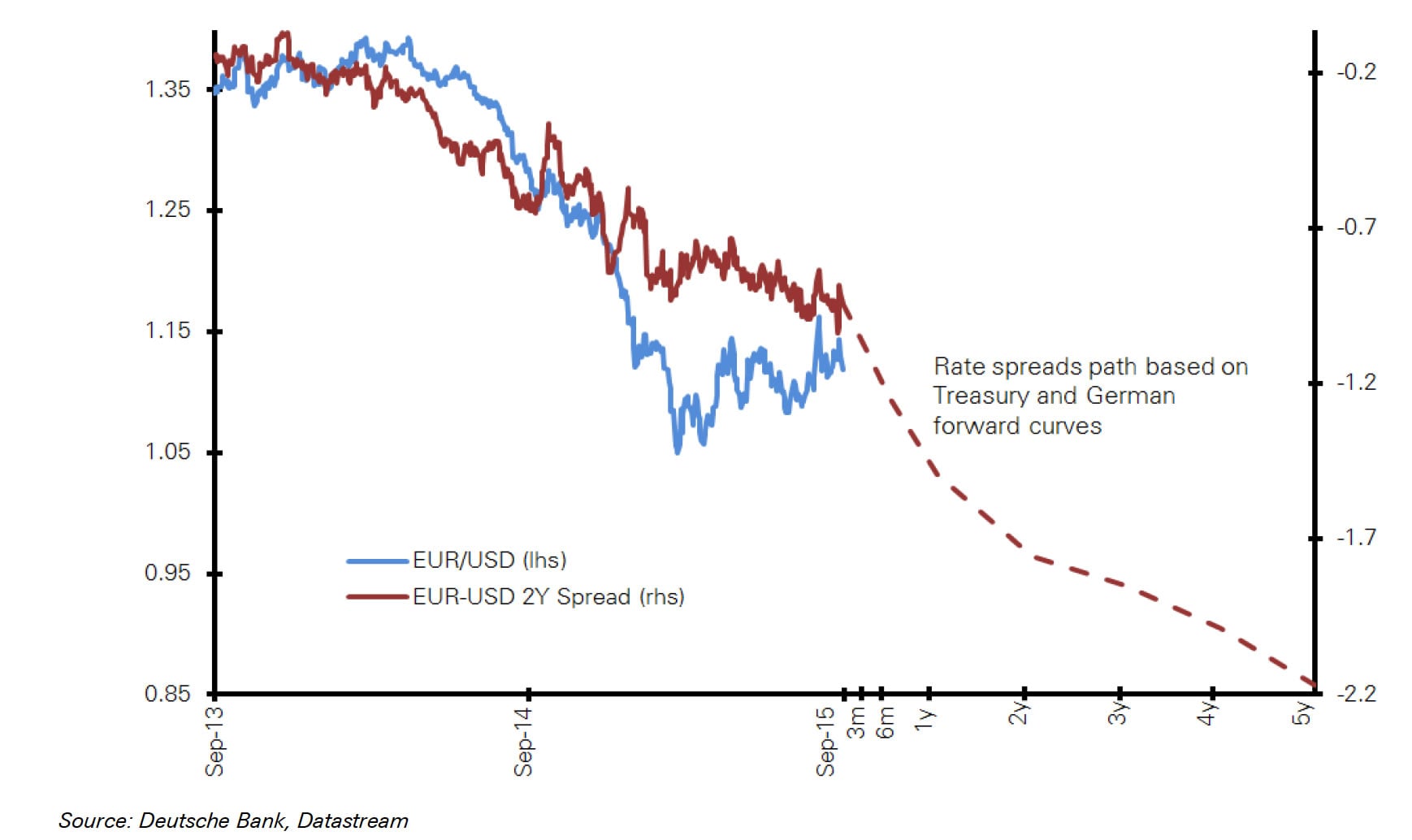

"We re-iterate our forecast for continued EUR/USD weakness over the course of this decade, with a move below parity in 2016 and a terminal forecast of 85cents by 2017," says Saravelos.

This view is in stark contrast to what analysts at HSBC are forecsting. HSBC say 2016 will likely see the US dollar peak in strength as US Federal Reserve rates will be raised at a gradual rate. So gradual in fact that they prove ultimately bearish for the USD's outlook.