Image © Adobe Images

"Dollar melts up, tracking Treasury yields" - Societe Generale.

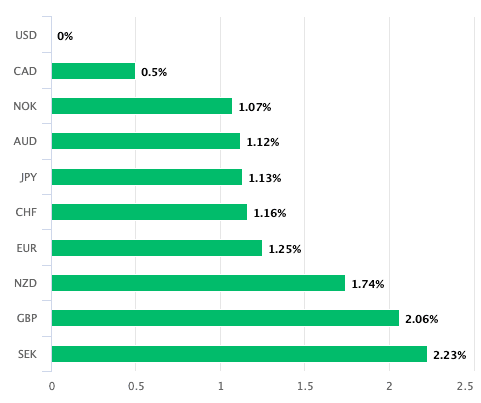

The dollar is purring along nicely: it's outperforming all peers and sits atop the G10 and free-floating EM leaderboards for the week.

The reason for the outperformance is not difficult to fathom: the market has conceded it has to consider the fact the Federal Reserve will raise interest rates later this year as rising inflation pressures and a solid economy simply can no longer be ignored.

That shift in expectations is reflected in rising U.S. bond yields, which are proving supportive of dollar exchange rates.

"The most interesting regime shift for markets and macro traders will be if the market starts to price in Fed rate hikes. This will light a fire under the USD and FX and bond market volatility," says Brent Donnelly, analyst at Spectra Markets.

That USD-positive regime shift in markets is underway and follows this week's consensus-beating inflation data which demands that the Fed consider raising interest rates.

Headline CPI shot up to 3.8% y/y in April, core rose to 2.8%. PPI inflation - which can tend to lead CPI inflation - surged to 6.0%, core PPI to 5.2%.

Chicago Federal Reserve Governor, Austan Goolsbee, said this week that "we have an inflation problem in this country," adding that the Fed has got to be thinking about how to break the chain of escalating inflation.

The shift in FX market is notable: GBP/USD drops from 1.36 to 1.3343 in the space of four days, a welcome dose of volatility in what has been a relatively staid market.

EUR/USD drops from 1.17 to 1.1623 by the time of writing Friday. "EUR/USD slipped to the lowest level since early April, driven by wider UST/Bund spreads and higher energy prices," says analyst Kenneth Broux at Société Générale.

"We are revising our Fed call and no longer expect rate cuts in 2026," says TD Securities in a market briefing out Friday.

"With the Iran conflict in a stalemate, oil prices still high, and supply chains stressed, we no longer see inflation progress as feasible this year," it adds.

Nevertheless, TD Securities is holding back from calling the next move on U.S. interest rates to the upside. "The next move for the FOMC is still more likely to be a cut than a hike. Risks of labour market acceleration are low, and inflation expectations remain well-anchored."

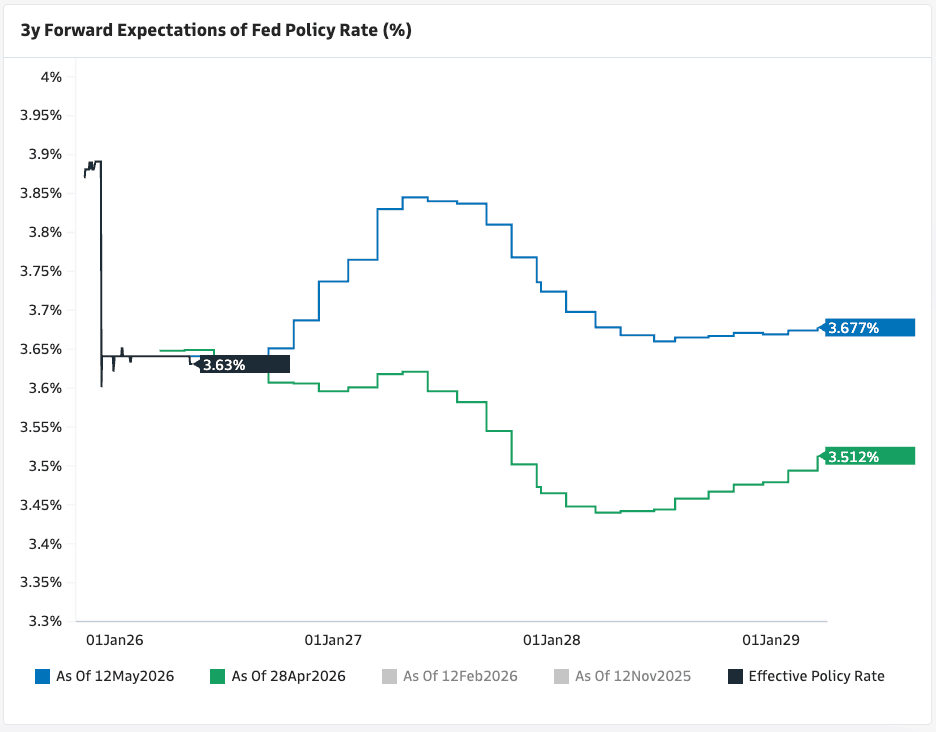

Above: Expectations for the future of U.S. interest rates have shifted higher notably. That's underpinned the dollar.

In addition, market nervousness regarding the seemingly intractable Middle East standoff is growing.

The assumption in many corners of the market was that the Strait of Hormuz would be opened by now, and that would send oil prices lower and release pressure from the global economy.

With the U.S. more insulated to these dynamics courtesy of its status as the world's largest exporter of oil, it's little wonder the dollar can benefit as tensions rise.

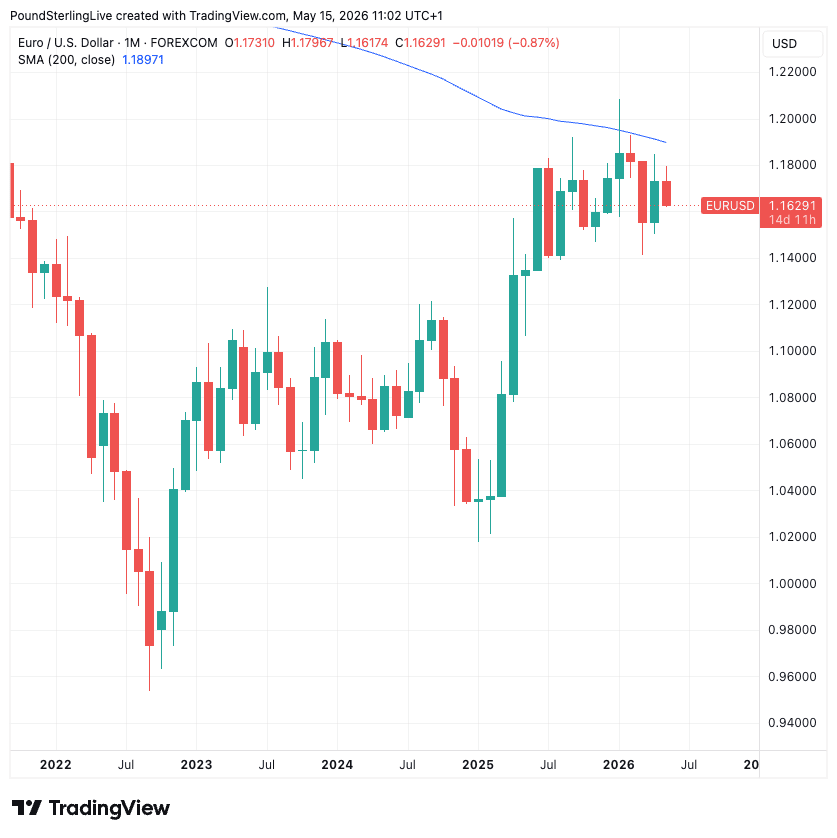

This week's strengthening in the dollar is by no means meaningful enough to suggest a major turning point in the currency's long-term selloff has been reached.

The monthly chart (above) confirms that the trend of USD weakness, in place since 2022, is intact, and for now, we're observing a seasonal snapback.

Indeed, May is traditionally a good month for the dollar.

Bigger picture, the longer-term dynamics that favour USD weakness are intact. "The Fed staying on hold makes us less bearish on the USD than before. However, we still maintain a downward USD forecast path in 2026 on asymmetric USD risks," says TD Securities.