- Week Ahead Forecast anticipates steady gains

- Mean-reversion pullback possible soon, however

- Trump provides overarching EUR-supportive narratives

- Why the ECB decision could weigh on EUR

Photo by: Sanziana Perju / ECB.

The Euro is on the front foot as Donald Trump reinvigorates global trade uncertainties.

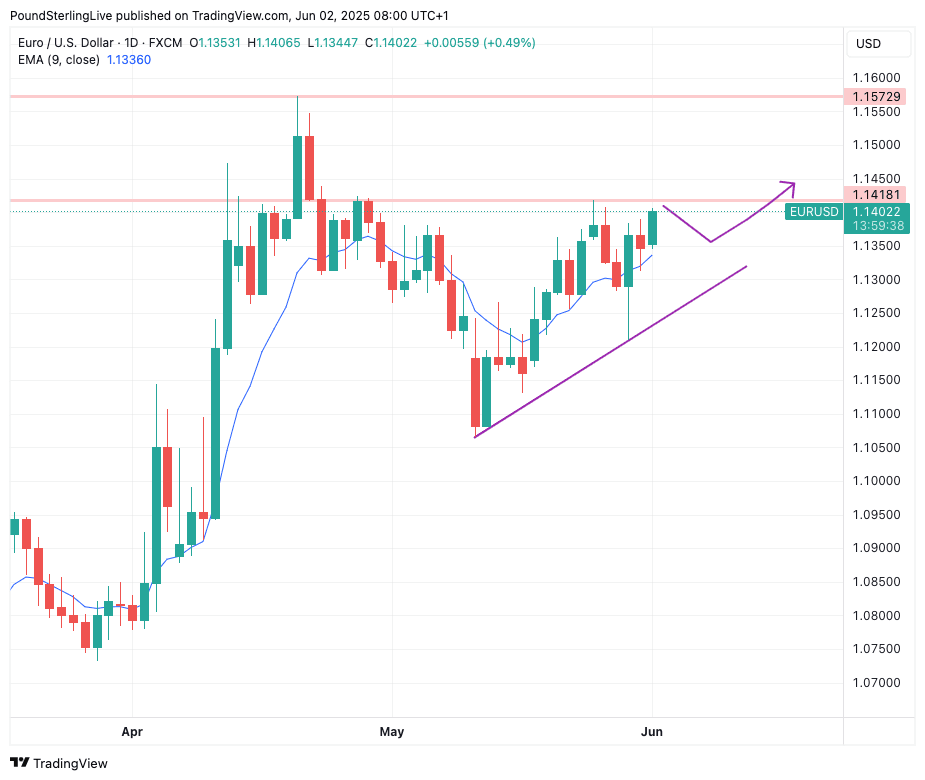

The Euro to Dollar exchange rate (EUR/USD) starts the new week well bid with a three-quarters of a per cent gain to a high of 1.1430, the highest level in more than five weeks.

The advance takes the pair through a graphical resistance line located at 1.1418 and opens the door to a push to 1.1450, which we see as a decent Week Ahead Forecast target.

Above: EUR/USD at daily intervals.

Consensus projections for the next four quarters, compiled from leading investment banks.

Access the full forecast →

However, the day's close must be above the resistance line at 1.1418 to confirm it has been broken and an intra-day pullback is possible.

The exchange rate likes to keep in touch with the nine-day moving average (the blue line in the above), which means some mean reversion is possible ahead of a resumption in the rally.

Bigger picture, this exchange rate is back on the front foot and the path of least resistance is to the upside in the coming days, fuelled by a compelling fundamental narrative of rising global trade tensions.

U.S. President Donald Trump must have gotten board with the calm that followed the China-U.S. trade agreement of early May, because he is now accusing China of breaching that agreement. In addition, after markets closed on Friday, he jacked up tariffs on Aluminium and steel.

"Tariff uncertainty is on the rise again following Trump's Friday evening announcement of a doubling of the steel and aluminium tariffs, to 50% starting June 4th. EUR/USD is back above 1.1350 and US yields are ticking higher, all whilst equity futures are well in red," says Jesper Fjärstedt, Senior Analyst, FX Strategy at Danske Bank.

A higher Euro now forms part of a classic market reaction to rising tariff tensions. The reminder that Trump fundamentally likes tariffs, and is unhappy with U.S. trade balances, should underpin the 2025 uptrend for the foreseeable future and we wouldn't be surprised if Euro-Dollar printed new highs as a result.

Trump said that China had "totally violated" the U.S.-China trade deal, bringing to an end the steady improvement in trade relations between the two countries.

Official White House Photo by Carlos Fyfe.

U.S. Trade Representative Jamieson Greer, who helped establish the agreement made between the U.S. and China in Geneva, said China has been "slow" in rolling out its compliance with the recent trade agreement, "which is completely unacceptable and has to be addressed."

The Chinese Ministry of Commerce responded in strong terms Monday, rejecting the accusations and accusing the U.S. of violating the agreement by introducing new chip controls and cancelling Chinese student visas.

"It should now be clear to most market participants that, even if we see periods of short-term détente from time to time, the fundamental conflict between the two world powers cannot easily be resolved," says Michael Pfister, FX Analyst at Commerzbank.

"In the long term, it will become increasingly clear that the US administration has no intention of abandoning tariffs," he adds.

Tariffs are proving a problem for the Dollar on the basis that they will undermine U.S. economic growth.

The problem is that the U.S. economy continues to hum along quite nicely, which undermines this thesis. Sooner or later, the data must start to show the kind of weakness that sellers of the USD have been anticipating over recent months.

June's release docket is important because it presents data that covers a period that should certainly start to encapsulate trade uncertainty. With the USD heavily bid, the big moves would be in response to above-consensus data that defies gloomy expectations, inviting a lopsided USD reaction function to the upside (i.e. EUR/USD downside).

U.S. ISM PMI figures for May are due for release on Monday and Wednesday, with JOLT job openings on Tuesday.

All bear watching. However, it is Friday's non-farm payroll figures that will be the clincher.

"The market is expecting a sharp slowdown in job creation for last month, as the labour market starts to crack under the weight of weak consumer and business confidence as tariff uncertainty weighs on the US’s economic prospects," says Kathleen Brooks, an analyst at XM.com.

The consensus looks for a 125k gain in payrolls for May, with a drop in private sector payrolls, and signs that jobs are being lost in the manufacturing sector. The unemployment rate is expected to remain steady at 4.2%.

"If the unemployment rate ticks up more than expected, we think the market reaction could be swift. The dollar is likely to fall, and the bond yields too, as the market rushes to price in rate cuts from a data-dependent Fed," says Brooks.

ECB President Christine Lagarde. Image: Andreas Reeg/ECB.

Don't forget the European Central Bank (ECB) on Thursday. Although the USD side of the equation is undoubtedly the more important, we would expect some short-term churn around the decision, where a 25 basis point rate cut is expected to take the base rate down to 2.0%.

The cut isn't the story. Instead, it will be the guidance that moves the exchange rate. With inflationary pressures cooling in the Eurozone, there is little incentive for President Christine Lagarde to discount further interest rate cuts, particularly if the ECB thinks U.S. tariffs will negatively impact growth going forward.

"The ECB are widely expected to cut interest rates by 25bps. However, markets are less certain about a hike at the following meeting in July. As result the ECB’s post meeting communication will be important for interest rate expectations and EUR/USD," says Kristina Clifton, Senior Currency Strategist at Commonwealth Bank.

A steady flow of cuts should benefit the Eurozone's economy, but would pose a headwind to the Euro's advance.

It is highly likely that Lagarde will stick with a well-worn message that interest rates are not on a preset path and the ECB remains data-dependent.

This means more cuts are coming, but there is no need to expect a faster pace, nor is there a need to bet on more cuts further down the line beyond what is already anticipated.

This will offer a limited opportunity to send Euro exchange rates in any meaningful direction, and post-ECB moves are likely to be faded as a result.

"We expect the ECB to be dovish because the US‑led trade war poses downside risks to the already soft Eurozone economy. If we are correct, markets will price in a higher chance of a cut in July which will weigh on EUR/USD modestly," says Clifton.