Image © Adobe Images

Speculation of coordinated currency intervention also weighs.

The Euro to Dollar exchange rate extends higher amidst fresh deterioration in USD demand.

The pair rose to 1.1321 (+0.30%) in the midweek session, with analysts pointing to concerns that U.S. debt market dynamics are making U.S. bonds increasingly unattractive to foreign investors.

Investors are paying close attention to the U.S. thirty-year bond yield, as this long-dated treasury bill is a good indication of how worries about U.S. debt are perceived.

"The steepening at the long end of the U.S. curve has proxied dollar weakness accurately. The current fresh bout of steepening, linked to both US risk premia and also global drivers could lead EUR/USD to our new 1.15 forecasts," says Themistoklis Fiotakis, FX analyst at Barclays.

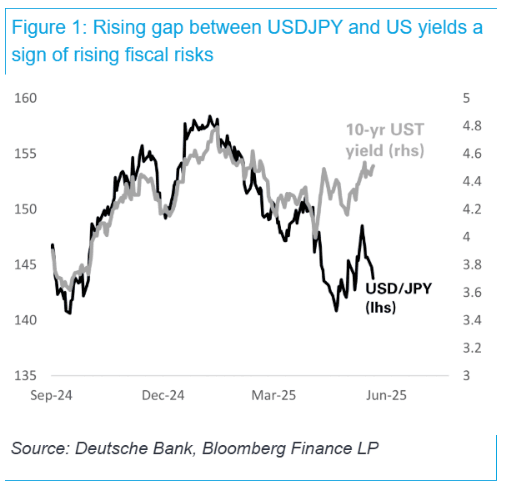

"A widening gap between US Treasury yields and USD/JPY would be the single most important market indicator of accelerating US fiscal risks. The chart below speaks for itself: the JPY is strengthening even as US yields are rising. We consider this as evidence that foreign participation in the US treasury market is declining," says George Saravelos, head of FX research at Deutsche Bank.

USD/JPY weakness mirrors nicely with EUR/USD strength, suggesting both the Yen and the Euro are benefiting from any declining demand for U.S. assets.

The question of U.S. debt sustainability rose late last week when Moody's lowered its U.S. sovereign bond rating, warning that successive U.S. governments have failed to get a grip on the country's finances.

U.S. President Donald Trump's Republican Party is pushing a significant new spending bill through Congress, which will push federal debt, currently at around 100% of GDP, the highest since the Second World War, to 125% of GDP in ten years.

"The U.S. debt trajectory is unsustainable in the long run," says Rogier Quaedvlieg, an economist at ABN AMRO Bank N.V. "The fiscal largesse points to upside risks to US long-term interest rates, which could eventually prove to be a headwind for both the economy and financial markets."

Consensus projections for the next four quarters, compiled from leading investment banks.

Access the full forecast →

The Euro benefits from a reallocation of global and domestic investor funds away from the U.S. to Europe. The shift in flows helps explain why the Euro-Dollar has risen 9.46% already in 2025, and as long as the reallocation extends, the Euro can continue to rise.

Analysts are also watching a G7 meeting of finance ministers to be held in Canada, with some speculation that U.S. Trade Secretary Scott Bessent will bring up the issue of currency with partners.

While Bessent has explicitly avoided saying he wants other countries to weaken their currencies, U.S. President Trump has long had issues with trading partners devaluing their currencies.

In short, we know it is one of the Administration's objectives, albeit one that is being kept on the 'low-down' in order to avoid any major selloffs.

USD weakness would be consistent with other countries - particularly Asian ones - raising their pegs and devaluing the USD in the process.

"If current speculation proves accurate – and the US is pushing for stronger trading partner currencies – it could not only prompt sharp appreciation in those currencies but also weigh on the dollar more broadl," says Pesole.

Given these concerns, it is little wonder the Dollar is selling off.

Add to this concerns over the U.S. debt pile and concerns that tariffs will slow the economy, and the USD downcase becomes clearer.