- EUR/USD in strong start

- Raises likelihood of a breakout

- As U.S. debt dynamics are a key concern

- Reinvigorating the 'sell America' trade

Image © Adobe Images

The 'Sell America' trade is back on.

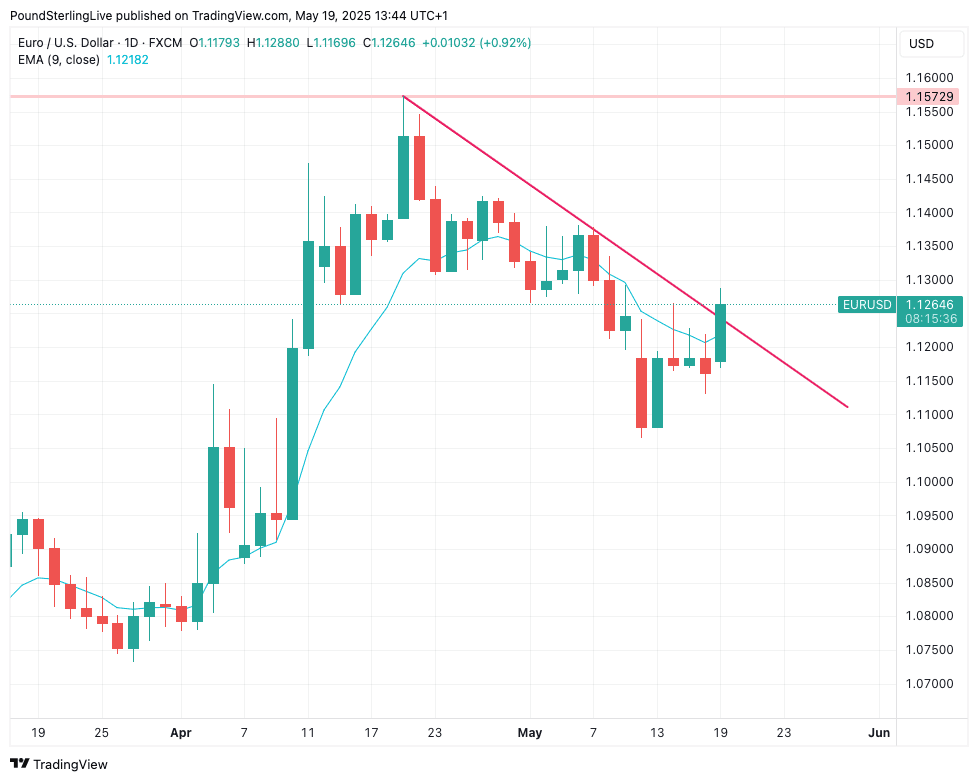

The Euro to Dollar exchange rate (EUR/USD) kicks the new week off with a strong start that raises the likelihood a technical breakout is underway, which ultimately brings the 2025 highs back into scope in the coming weeks.

A near-1.0% bounce on Monday comes as investors resume the 'Sell America' trade amidst fears that the U.S. is piling on the debt, an issue that was brought into sharp relief late on Friday when Moody's cut its rating for U.S. Treasuries.

The rally means the exchange rate is now attempting a break through the downward sloping trend line that has been in place since April 23, when it peaked and turned tail:

Above: EUR/USD at daily intervals.

Consensus projections for the next four quarters, compiled from leading investment banks.

Access the full forecast →

The recovery to 1.1264, where we find ourselves on Monday, could be decisive enough to breach the downtrend line and take the market above the nine-day exponential moving average (turquoise line in the above).

This turns the market near-term bullish, and a near-term move to 1.13 becomes visible.

Moody's lowered its U.S. debt rating after markets closed last week, cutting it one notch to Aa1 from Aaa, while its outlook was changed to stable from negative. Fitch and S&P, the other main agencies, had previously removed the US’s pristine rating.

The decision comes as the Republican Party this week looks to pass a bill that will embed 2017's tax cuts, while offering little by way of meaningful spending cuts.

This means the U.S. debt burden is set to grow, and there are whispers that a market that is more sceptical about the U.S. in the Trump era might be less willing to fund this spending by buying U.S. debt (bonds).

"With less global trust comes less desire to finance the external position of other countries. I don’t want to overstate this relationship, but it could be a useful framework going forward if Liberation Day was the peak for the USD and global investors become more risk averse as it pertains to investing in countries that require a steady stream of external capital," says Brent Donnelly, trader and analyst at Spectra Markets.

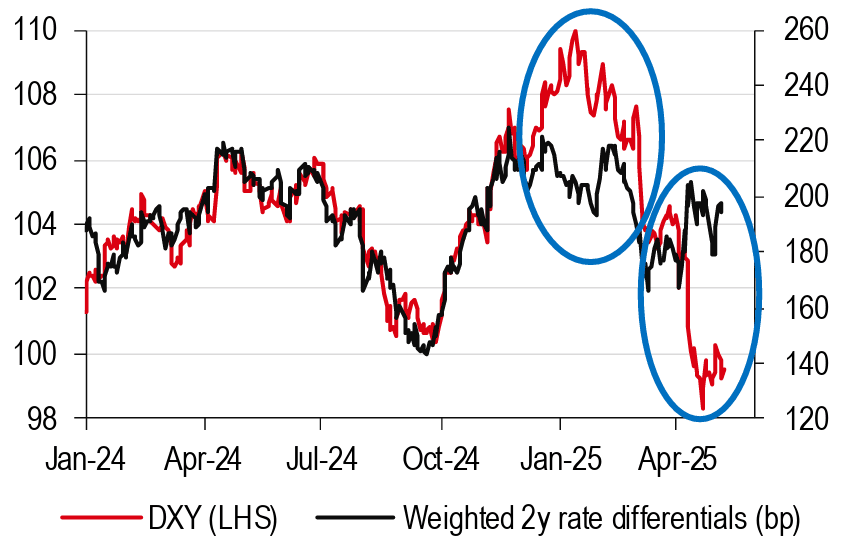

Above: The Dollar index has decoupled from yield differentials. This means it is now carrying a risk premium, that is associated with a breakdown in trust in U.S. assets. Image courtesy of HSBC.

"The structural bear case against the dollar has begun to play out: investors are rethinking underhedged asset exposures to the US that could lead to a prolonged valuation adjustment lower," says FX strategist Alex Cohen at Bank of America.

Concerns about the U.S. debt situation are evident in U.S. Treasury yield dynamics, where the long-dated 30-year yield has risen to the psychologically significant 5.0% level.

We are not yet seeing a crisis, but if it does become a problem, it will become a problem in a big way, and quickly.