Research shows that the outlook for the euro exchange rate complex (EUR) remains challenging as US corporates continue to pile into Eurozone debt markets seeking cheap finance.

Also tipped to keep the euro under pressure is the continued flood of global money going into Europe as investors pick up stocks that are expected to outperform thanks to European Central Bank (ECB) quantitative easing. Usually this would boost the euro, but billions of euros are being simultaneously hedged on currency markets and this is why the exchange rate is falling.

At the time of writing the euro to dollar exchange rate (EURUSD) is seen at 1.0935, marginally down on the previous days close and well down from 2015’s high at 1.200.

The euro to pound exchange rate (EURGBP) is at 0.7154, higher than at last night’s close but down from a 2015 high at 0.7875.

Why has the euro fallen against the dollar?

1) The Reverse Yankee Effect – Corporate Debt

Underlying the euros heavy fall for the past year has been the theme of central bank policy divergence. With the US and UK looking to raise interest rates, and thus the cost of borrowing, the ECB has set itself apart by looking to cut rates and pursue a policy of quantitative easing.

Quantitative easing and negative interest rates in Europe have created a borrowers’ paradise. Data shows that US companies are eager to take advantage of this cheap money at the very time when they face increased borrowing costs.

US dollar borrowers are able to raise long-term euro funding at costs lower than are available in the United States. Look at this for an example – Coca-Cola recently issued $9.5 Billion in Euro-Denominated bonds making it the latest American firm to tap the market.

WSJ say this is the largest euro-denominated bond issued by an American firm on record and the second-largest by any company in the currency.

“One of the reason for the sharper than expected decline in the EUR during March was as a result of a marked increase in US corporate issuance into the Euro Area to take advantage of cheaper all-in funding,” says Kamal Sharma an FX Strategist with Bank of America Merrill Lynch Global Research.

How does this drive currency markets, specifically with regards to the outlook for the euro? The answer lies in the fact that a good chunk of the money raised will be converted into dollars.

“This trend in the so called ‘reverse Yankee’ trade is set continue for the rest of the year according to our credit strategists and will provide a source of pressure on EUR/USD as US corporates repatriate some the proceeds from issuance back to the US to pay down USD denominated debt. According to media reports, new US corporate issuance in Europe has come to the market again in recent days,” says Sharma.

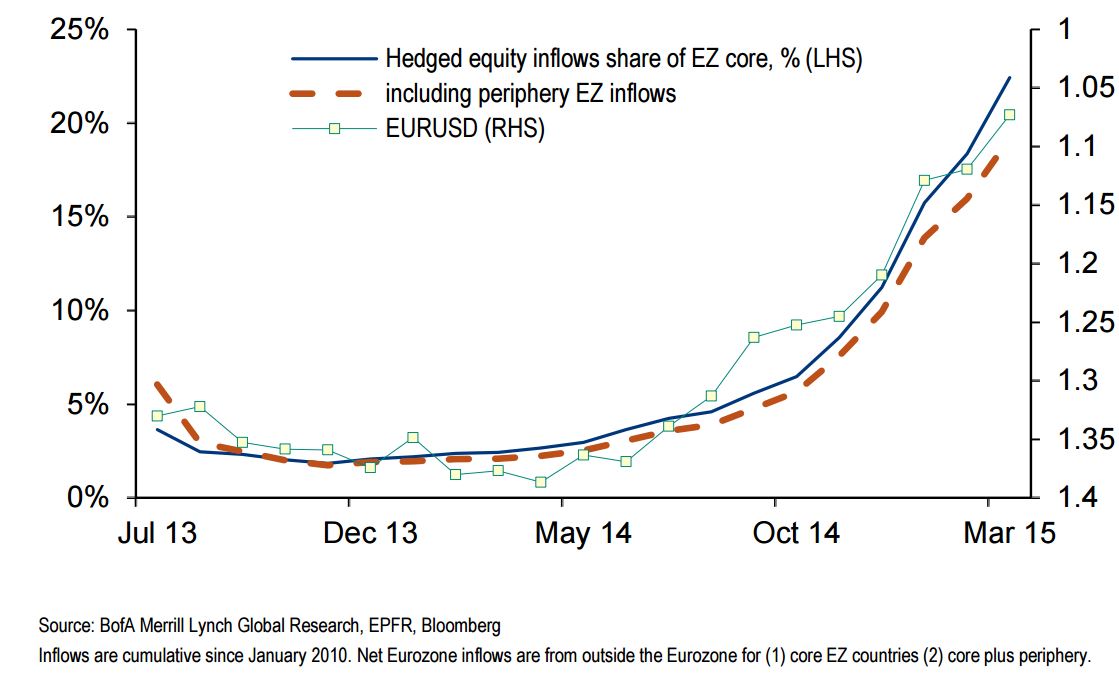

2) Equity Markets: Hedged Exposure is Negative for the Euro

The EURO STOXX market has outperformed the SPX by 15% to 3% year-to-date indicating the extent of interest in European stocks at the present time.

Logic would usually dictate that the transfer of US dollar funds into euros, for the purchase of stocks, should boost the euro.

However, “investors have been increasingly hedging their European equity inflows,” says Sharma, “the support for EUR has weakened more than previously believed because investors have been hedging more. This development is bearish EUR all else being equal.”

The below graphic confirms the relationship between hedging and the exchange rate:

When central banks ease, investors tend to buy into the equity bull-trend that the extra money being printed fuels. However, foreign investors’ returns are undermined when converted back to USD because of simultaneous currency depreciation.

Studies show how both the Nikkei and the DAX have rallied from their respective lows as market expectations grew that QE was imminent. But the Euro fell despite the consistent rise in the German DAX index.

“The view is that such flows had become increasingly more FX hedged than was previously thought. We had expected that the Euro would have found some support from equity inflows but had clearly underestimated the extent to which they had been increasingly FX hedged,” says Sharma.

As investors have become more comfortable holding hedged equity positions during currency trends, the equity inflows would provide less support for the currency. This is bearish EUR all else being equal say Bank of America.

More Weakness to Come for Euro Dollar Exchange Rate

Bank of America’s European economists continue to believe that the ECB QE program will run to its entirety to September 2016 and could be extended beyond that date. At the same time, they maintain their view that the US will begin its tightening cycle in September.

“Given the recent ‘tantrum’ in bond markets which has filtered into FX markets, the long USD/US curve flattening position has been significantly pared back by the speculative community. Should the US data pick up more consistently then the continuation of the trend of EUR/USD weakness remains our baseline scenario,” says Sharma.

As long as Eurozone debt remains cheap and investors buy into the stock rally Euros will continue to be sold.