U.S. Dollar exchange rates have not benefited from recent financial market volatility but Goldman Sachs research suggests this is not unusual and that any 'safe haven' bid going forward would be likely to vary according to the degree of stress there is in the banking sector and broader global markets.

Dollars were sold widely against most other major currencies last week, leading USD/G10 pairs to fall for much of the period even as heavy losses for banking stocks pulled share indices lower around the world while cultivating the kinds of market conditions that have often benefited the U.S. currency.

Speculation about the future of Credit Suisse and the connected bonfire of European banking stocks offered the Dollar some brief respite last Wednesday when weighing heavily on European currencies but the greenback still ended the week nursing widespread losses.

To many, this will have appeared contrary to the 'safe haven' characteristics of the Dollar but Goldman Sachs research shows how those characteristics lead to different types of response and a variable performance against other currencies during periods of market upset.

"In short, we find that it is not unusual to see the Dollar underperform in periods of increasing financial stress, but it generally occurs when the magnitude of stress appears less severe," says Karen Reichgott Fishman, a senior FX strategist at Goldman Sachs.

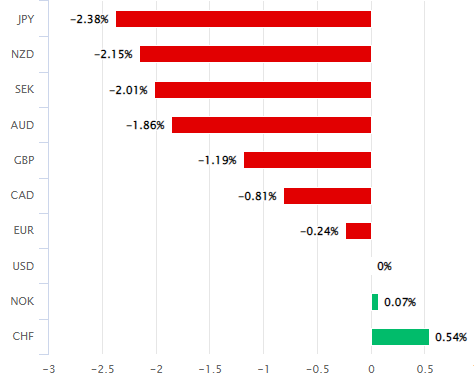

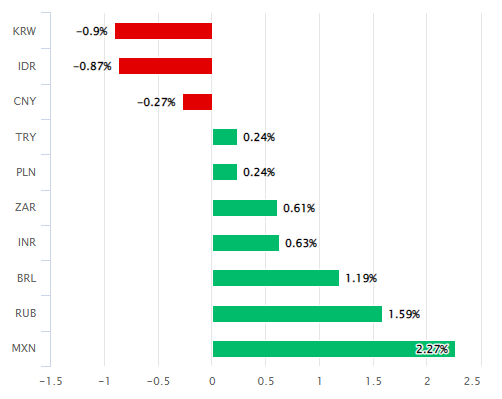

Above: U.S. Dollar performance relative to G10 and G20 currencies in week ending March 17. Source: Pound Sterling Live.

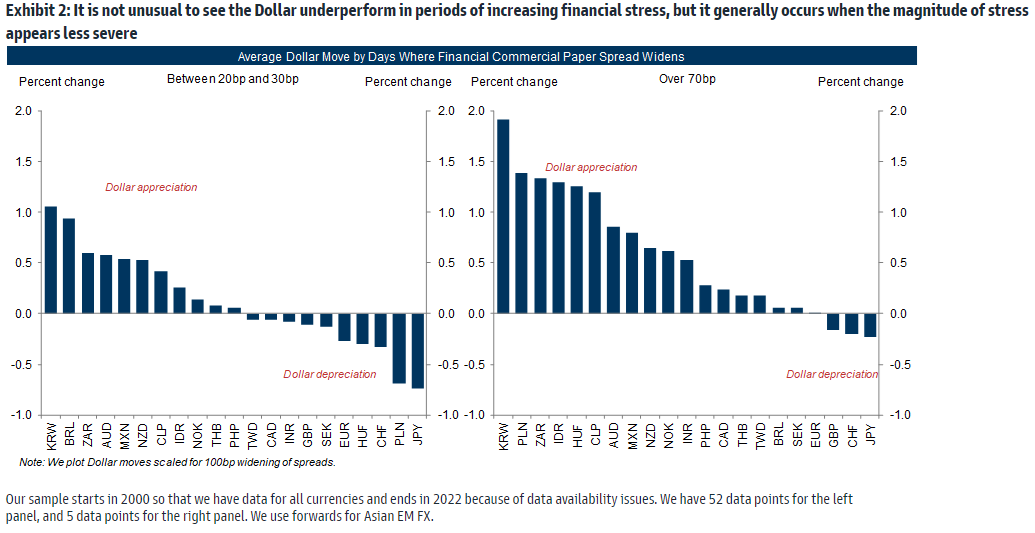

Fishman and colleagues' research suggests that 'safe-haven' demand for the Dollar tends to vary with the difference between yields on the three-month corporate debt of the banking sector and its 'risk-free' counterpart in the U.S. Treasury market.

Data covering yields during bouts of financial sector distress going back to the year 2000 shows that when the banking sector's corporate bond spread remains below 30 basis points or 0.3%, gains and losses for U.S. Dollar rates were almost evenly split across the USD/G20 grouping.

Dollar strength builds and broadens significantly once the corporate bond spreads rise above 70 basis points or 0.7%, although there have only been five such instances since the turn of the millennium while there were 52 instances of distress involving a bond spread of up to 0.3%.

"On days when the financial spread widened by over 70bp, the Dollar typically strengthened against most currencies except for other safe havens and GBP. This suggests that the Dollar should still rally if the current situation worsens and becomes more systemic," Fishman and colleagues say.

"In that scenario, we would also expect to see equities selling off and global rates rallying alongside US rates," they add.

Source: Goldman Sachs Global Investment Research. Click image for closer inspection.

The Goldman Sachs team also says one important factor that at least partially explains the differing Dollar outcomes is the performance of stock markets because the largest and broadest rallies from the greenback have tended to coincide with the steepest losses for share indices.

Similarly, when moderating expectations for the Federal Reserve (Fed) interest rate prompt U.S. Treasury yields to fall more than their overseas counterparts, as they did in response to March turbulence in the U.S. banking sector, the Dollar has often tended to underperform other currencies.

But Fishman and colleagues have argued that this is also now one reason why the Dollar might be unlikely to fall much further in the weeks and months ahead, and could even make a comeback in some circumstances.

"The high level of uncertainty and volatility, however, suggests that we may continue to shift quickly between regimes. For instance, if equity prices are falling on rising systemic risk, the Dollar should see more support, or if pressures broaden to other jurisdictions that have also seen rapid rate increases and duration losses," they write in a research briefing last Wednesday.

"But even if the current banking system stress remains relatively isolated with limited spillover to the real economy or larger banks, the latest shift in Fed expectations means that we would most likely face a similar backdrop to just a few weeks ago: an overheated economy that requires another repricing as cuts are unwound and rate hikes are added back in after March," they add.

Source: Goldman Sachs Global Investment Research. Click image for closer inspection.