- EUR/USD jumps

- As 'long' USD positions are cleared

- USD could recover soon says ING

- But a lower terminal Fed rate could be behind the weakness

- In which case, USD weakness has legs

Image © Adobe Images

The Dollar has fallen against the Euro and British Pound, but the move won't be an enduring one says a foreign exchange strategist we follow.

In fact, Francesco Pesole, FX Strategist at ING, says the Euro's run of appreciation against the Dollar will be done by the weekend.

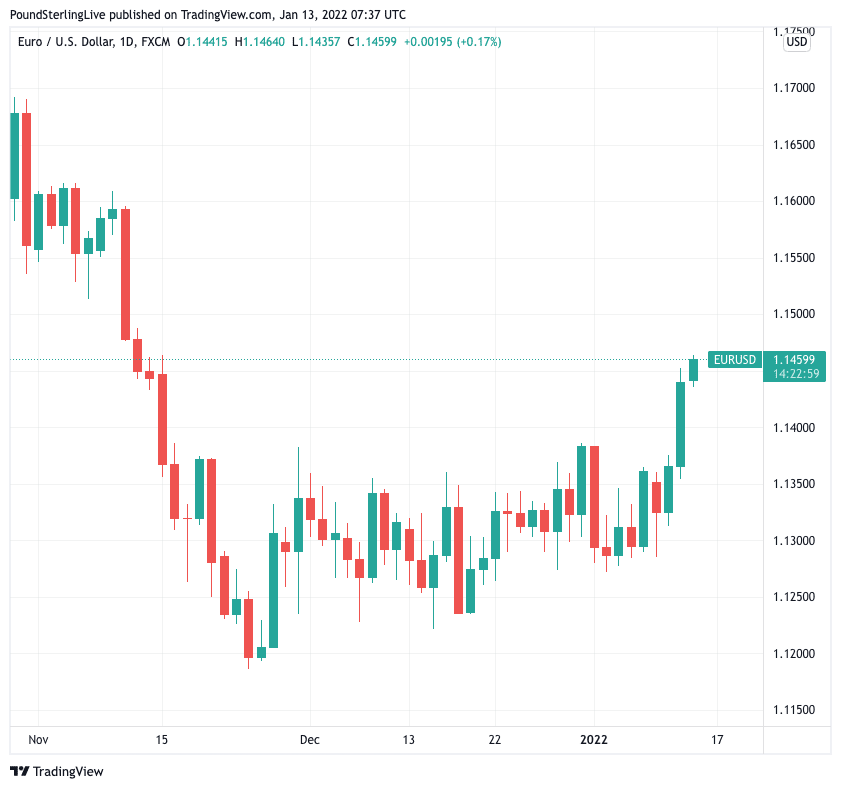

The Euro to Dollar exchange rate (EUR/USD) has rallied to its highest level in two months at 1.1462 at the time of writing on Thursday, January 13.

The pair had been rangebound since early December, but a series of events concerning the U.S. Dollar has ensured it has broken out of its recent range to move to the upside:

Above: EUR/USD shown at daily intervals.

- EUR/USD reference rates at publication:

Spot: 1.1465 - High street bank rates (indicative band): 1.1064-1.1144

- Payment specialist rates (indicative band): 1.1362-1.1410

- Find out more about market-beating rates and service, here

- Set up an exchange rate alert, here

"EURUSD burst through very well-defined resistance at 1.1386 yesterday that had capped the action for the pair since late November as the US dollar weakened sharply in the wake of the December CPI release yesterday, clearly a sign that the bar is high for Fed hawkishness to support the US dollar. The next key resistance area looks like 1.1500-25," says John Hardy, Head of FX Strategy at Saxo Markets.

The Dollar slumped and gave a pass higher to the Pound and Euro on January 12 following the release of inflation data on Wednesday that showed the U.S. witnessed its strongest rise in prices since 1982 in December.

But the 7.0% headline figure was anticipated by markets, who might have been looking for an even hotter read.

"A well-telegraphed jump in US inflation to 7% was taken as a 'sell the fact' opportunity for FX investors, with a substantial unwinding of dollar longs triggering widespread dollar weakness," says Pesole.

ING says the technical break higher in EUR/USD likely put some extra pressure on the Dollar in other crosses, but "whether the 1.1500 resistance holds is key for dollar bulls at the moment".

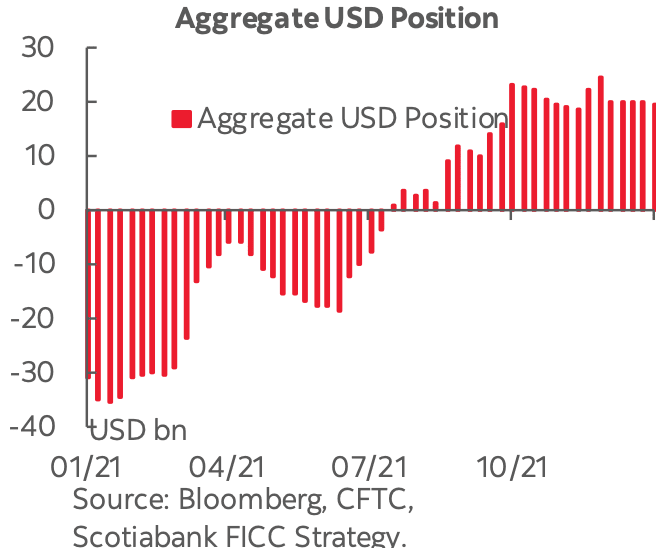

Positioning was firmly pitted against the Dollar heading into 2022 as the market had piled into a consensus 'long dollar' trade through the second half of 2021.

With positioning stacked in anticipation of yet further gains by the Greenback the trade has ultimately become crowded and vulnerable to any setback in the 'long dollar' narrative.

"Positioning suggests that long USD is the consensus trade for the beginning of the year. However, consensus trades have historically performed poorly during the first quarter. Against market consensus and positioning, we continue to expect modest USD depreciation over 2022," says Erick Martinez, FX Strategist at Barclays.

Once extended positioning is cleared away the path higher arguably becomes easier.

"The dollar might have a more balanced positioning now after a large long-squeeze, which could help keep EUR/USD below 1.1500," says Pesole.

There are no shortage of foreign exchange analysts and strategists who continue to back the Dollar in 2022, believing that a squeeze on Dollar longs can actually improve the outlook for the currency.

"We still think the dollar counter trend does not have long legs, and we see scope for a recovery by the end of this week," says Pesole.

The hot inflation data justifies the intention of the U.S. Federal Reserve to begin raising interest rates and then whittling down the balance sheet that ballooned under its quantitative easing programme over coming months.

"The dollar fell after U.S. consumer inflation rose broadly in line with market expectations, keeping intact a highly hawkish outlook for Fed policy," says Joe Manimbo, Senior Market Analyst at Western Union Business Solutions.

"Imminent Fed tightening and room to cement views around a fourth Fed hike in 2022 (the Fed’s Bullard sees this as the base case scenario) still offer the greenback – which should now have a less skewed net-long positioning - some appeal on dips," he adds.

Strategist Bipan Rai at CIBC Capital Markets says it is too soon to count the U.S. Dollar out.

"Over the medium-term, there’s still a compelling rationale to be long USD," says Rai.

CIBC says the market holds a terminal rate (the level at which the rate hiking cycle at the Fed ends) that is too low, in their opinion.

Furthermore, quantitative tightening - the process whereby quantitative easing is reversed - is under-appreciated.

"In the near-term, we’ll concede that hawkish Fed repricing takes a breather and that extant long USD positioning is a significant headwind. Patience is required here," says Rai.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

But analysts at investment bank MUFG are not convinced the Dollar can turn around its fortunes anytime soon.

MUFG says an additional explanation to the Dollar's recent underperformance could lie with the underperformance of long-term bond yields.

These are the yield paid by longer-term bonds, and foreign exchange theory suggests that should longer term bond yields be elevated sufficiently relative to shorter-term yields a 'curve' is created in bond markets that is supportive of the Dollar.

But, longer-dated U.S. yields have in fact been underperforming of late, and the reason is clear.

"The failure of the dollar to advance may also be explained by the relatively poor performance of rate expectations further out the curve," says Derek Halpenny, Head of Research, Global Markets EMEA at MUFG.

The Federal Reserve indicated in the minutes to its December meeting - out last week - that it could soon start reversing its quantitative easing programme.

This could involve the Fed allowing bonds it has purchased under quantitative easing to simply expire, or the Fed could actively sell bonds.

This would have the effect of tightening monetary conditions in the U.S. (as the Fed fights inflation) without the need for raising interest rates.

Therefore, recent talk of quantitive tightening has lead markets to believe the need to push rates higher will ease once quantitive tightening begins.

MUFG notes numerous Fed officials have spoken about the need to engage quantitative tightening, with the latest being Loretta Mester, who said yesterday "we should shrink the balance sheet as fast as we can".

This implies a lower 'terminal' rate for U.S. interest rates and this is not necessarily all-out bullish for the U.S. currency.

The Bank of England, by contrast, set out in August 2021 the conditions that must be met for it to begin quantitive tightening:

Once Bank Rate is hiked to 0.5% it will stop reinvesting the proceeds of maturing bonds that it owns, leading to a steady depletion of its holdings.

But when rates reach 1% the Bank will consider selling some of its gilts back to the market.

The Pound endured a relatively soggy second half to 2021, with analysts saying the Bank of England's terminal interest rate was set lower than elsewhere, an outcome almost certainly linked to the Bank's well telegraphed quantitative tightening scheme.

Now the U.S. Fed is coming on board with this kind of tightening, albeit with a more opaque guidance; but the implications for the Dollar are clear, if the Pound's experience is anything to go by.