Image © Adobe Images

The Euro will be looking to record a third successive daily advance agains the Dollar on Tuesday as a near-term rebound shapes up.

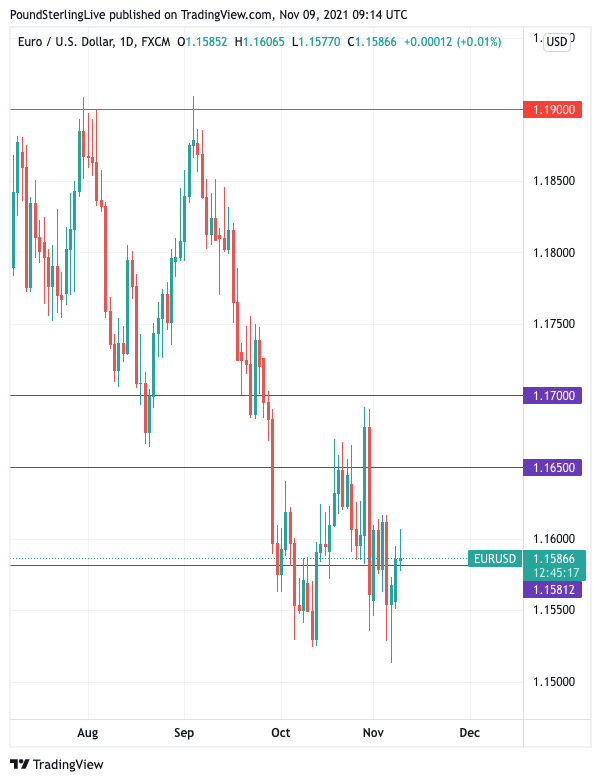

However, analysts suggest there is a great deal more work to be done by Euro bulls before the outlook improves to an extent that a run back towards 1.20 can be considered.

"The EUR/USD supermajor confirmed the tactical bullish reversal from Friday, but the rally yesterday was modest in scale and the price action needs to vault the 1.1650-1.1700 area to suggest that the US dollar is under broader pressure and to open up the range toward 1.1900," says Steen Jakobsen, Chief Investment Officer at Saxo Bank.

Above: The key hurdles the Euro must cross identified by Saxo Bank in order for the outlook to turn more bullish.

- EUR/USD reference rates at publication:

Spot: 1.1590 - High street bank rates (indicative band): 1.1185-1.1266

- Payment specialist rates (indicative band): 1.1480-1.1533

- Find out about specialist rates, here

- Or, set up an exchange rate alert, here

The Euro had in fact fallen to a new 2021 low at 1.1513 on Friday in the wake of stronger-than-expected U.S. labour market data, underscoring the downward slope of the near-term trend.

However, selling pressure soon flipped and a rebound ensured the Euro-Dollar ended the day with a gain.

The turnabout gives a sense that there is some solid support to be found at around the 1.15 area and this could allow the prospect for some tepid advances by the Euro.

But Saxo Bank's Jakobsen says he is unsure as to what the catalyst for a more meaningful rally by the Euro could be, "given how much support USD bears have already seen recently from the backdrop of strong risk sentiment and weak US long yields".

"A close back below 1.1550, meanwhile, sets up pressure on the cycle lows ahead of 1.1500. The US CPI data tomorrow is perhaps the next catalyst for a USD move," says Jakobsen.

All eyes turn to the midweek release of U.S. inflation where a stronger-than-expected reading could bolster support for the U.S. Dollar.

Such a reading would signal to markets that the U.S. Federal Reserve could bring forward the expected timing of an interest rate rise in 2022 in order to combat heating prices.

This would provide support to the yield paid on U.S. bonds, a key attraction for foreign investors hungry for superior returns.

"We are maintaining a short EUR/USD trade idea. The trade idea has got off to a good start as EUR/USD has fallen back to a new year to date low of 1.1514,” says Lee Hardman, a currency analyst at MUFG, who’s been a seller of the Euro-Dollar rate from 1.1650.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

MUFG continues to expect EUR/USD to trade heavy heading into year-end on the back of monetary policy divergence between the European Central Bank and Federal Reserve.

"The main risk would be a policy surprise from the ECB on 16th December when they are due to unveil their QE tapering plans for next year,” said Hardman.

The ECB is anticipated to end its Covid crisis-era quantitative easing programme (PEPP) in March 2022 but will likely continue with its longer-running quantitative easing programme known as APP.

The market has of late bet that the ECB could also be forced to react to rising inflation levels by raising interest rates as early as 2022.

This would require both the PEPP and APP programmes to end within months of each other, something the ECB governing council have been reluctant to countenance.

Indeed, all recent communications from ECB governing council members have been unanimous in their view that interest rates won't rise as early as 2022, suggesting Euro buyers who had been betting on such a surprise could be disappointed.

On November 03 ECB President Christine Lagarde said "conditions for a rate hike are unlikely to be met next year".

Head of the Banque de France, François Villeroy de Galhau, said last week he sees "no reason to raise rates next year".

Robert Holzmann said later in the week that a "2022 rate hike is inconsistent with the central bank's forward guidance".

This is particularly significant in that Holzmann is considered one of the more 'hawkish' members of the ECB.

ECB Chief Economist Philip Lane said on Monday that "we have to be sufficiently patient so as not to overreact to a temporary increase in inflation."

"We still believe the ECB will maintain accommodative policy next year, but risks are now tilted towards a quicker removal of stimulus than markets were banking on just a few months ago," says Claus Vistesen, an economist at Pantheon Macroeconomics.

Pantheon Macroeconomics anticipate the pace of APP will slow to €20B in the fourth quarter of 2022, from €40B immediately after the PEPP ends in March next year.

Even by bringing forward the slowdown in APP the ECB will be a laggard to the U.S. Fed and Bank of England with regards to normalising policy, suggesting the Euro will remain under pressure with regards to central bank policy divergence for some time yet.