- EUR/USD buoyed by U.S. stimulus hopes after Trump-inspired recovery.

- Westpac says EUR rally at risk after new record low for inflation in Sept.

- Eurozone disinflation reduces DE-U.S. yield spread, threatens EUR/USD.

- But stimulus, U.S. election & virus dominate EUR agenda in short-term.

Image © European Central Bank, reproduced under CC licensing

- EUR/USD spot rate at time of writing: 1.1766

- Bank transfer rate (indicative guide): 1.1356-1.1438

- FX specialist providers (indicative guide): 1.1592-1.1662

- More information on FX specialist rates here

A dearth of Eurozone inflation is being tipped as the greatest headwind to sustained an long-term appreciation by the Euro, according to new resrearch from Westpac.

“The key risk to the USD bear trend remains the gravely low Eurozone inflation picture and the risk that it might trigger expanded ECB asset purchases,” says Richard Franulovich, head of FX strategy at Westpac.

Eurozone inflation fell -0.3% in September, a new record low that built on the -0.2% decline of August and in a month when economists and markets expected that price pressures would rise, which risks vindicating European Central Bank (ECB) policymakers for their protests about strength in the single currency.

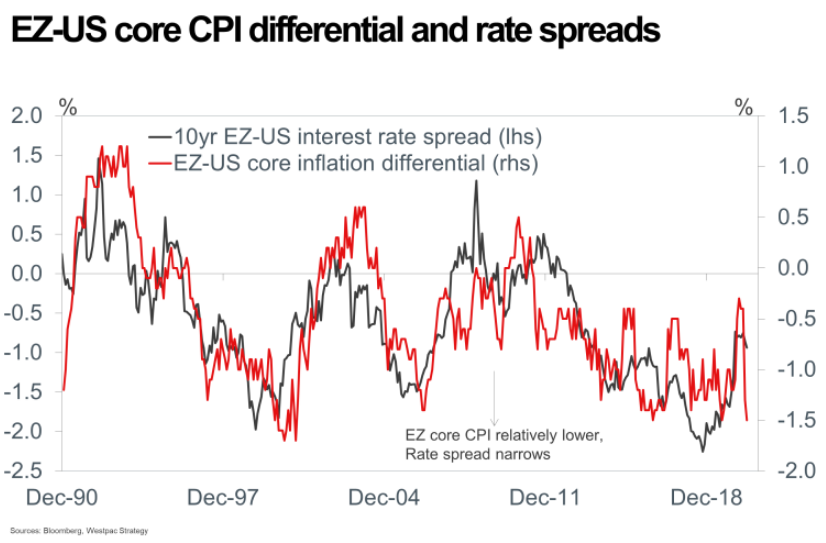

"While some of the weakness in inflation reflects temporary one-offs (i.e. delayed summer sales and sales tax cuts), the ECB is likely to maintain a close watch. As shown below, the Eurozone-US core inflation differential has historically been a reasonable gauge for the Bund-Treasury spread and further undesirably low EZ inflation would be associated with a drift in the spread in an EUR-negative direction," says Franulovich.

Above: Westpac graph showing correlation between gap in Eurozone and U.S. core inflation, and German-U.S. bond yields.

If Eurozone prices continue to fall, or even just fail to keep pace with those in the U.S., then German-U.S. bond yield spread - the difference between yields on the two countries’ bonds - would likely also be found falling and this might have implications for the Euro.

The movement of real yields matters, as investor capital tends to flow from where yields are low to where they are relatively higher, therefore a move higher in U.S. real yields relative to Europe would support the Dollar against the Euro. We reported on Monday that research from Société Générale showed that real yield are currently moving in favour of the Dollar.

Analysts at the French based investment bank said that this was because the market had faith that the U.S. Federal Reserve would generate inflation while the same could not be said for the ECB.

EUR/USD has closely followed the gap between German and U.S. yields since the single currency's formation two decades ago, although 2019 saw one of the longest-lived breakdowns in this relationship during which time the Euro followed the differential in market expectations for economic growth.

"Growth and rate differentials are of secondary consideration for FX markets, which continue to grapple with a once-in-one-hundred year global shock," Franulovich says. "FX markets will react to any major policy responses by repricing the global outlook first, via risk sentiment channels, and that is USD negative. The USD anyway has a long established positive relationship with the US fiscal position, tending to appreciate as deficits narrow and depreciate when deficits expand...There’s every chance another surge in Treasury issuance might be accompanied by an expansion of Fed asset purchases too, under the guise of maintaining smooth market functioning."

Above: Euro-to-Dollar rate shown at monthly intervals with German-U.S. 10-year bond yield spread (orange line, left axis).

Many economists still expect the Eurozone to outperform the U.S. over the coming year or so, while the Dollar is being hampered by rapid increases in U.S. government spending and the creation of new Dollars by the Federal Reserve (Fed) in order to facilitate Treasury programmes.

These factors could keep the Euro-to-Dollar rate on an upward trajectory for a while yet, although this would depend on the Euro remaining oblivious to a less favourable spread between German and U.S. government yields.

Westpac forecasts the Euro will rise to 1.21 by year-end and 1.25 before the curtain closes on 2021, as the Dollar downtrend continues, although economic growth, employment, inflation, politics and actions of the ECB as well as Fed will all be important in determining whether these are ultimately borne out.

Strengthening currencies can counteract inflation by making imported goods cheaper to buy and Europe, more so than others, has long struggled to generate the “close to, but below 2%” price growth the ECB is charged with delivering.

Like others, the ECB has for years used interest rate cuts and quantitative easing in the hope of lifting inflation back to its long-elusive target. But this was to little avail even before the pandemic, which has since undermined the limited growth and inflation that the common currency bloc previously had.