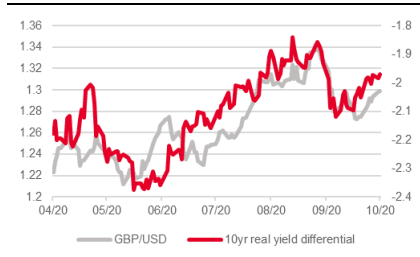

- UK-US yields hint at further GBP/USD support

- Real yield movements back September's USD outperformance

- Eurozone real yields not tracking nominal yields

- Reflects markets low faith in ECB to stir inflation

Image © Adobe Images

- GBP/USD spot rate at time of publication: 1.2931

- Bank transfer rate (indicative guide): 1.2583-1.2674

- FX specialist providers (indicative guide): 1.2742-1.2820

- More information on FX specialist rates here

Economists at Société Générale have told clients that the yield paid on government bonds in the U.S., Eurozone and UK maintain a strong grip on foreign exchange market dynamics and continue to explain moves in the Dollar, Euro and Pound.

The movement of real yields matters, as investor capital tends to flow from where yields are low to where they are relatively higher, therefore a move higher in U.S. real yields relative to Europe would support the Dollar against the Euro.

Indeed, findings by Soc Gen are that real yields are currently showing two things: 1) the Dollar should remain supported against the Euro 2) the Pound-Dollar rate should remain supported by dynamics in the UK-US yield differential, which continue to suggest support for the Pound.

Image courtesy of Societe Generale. If you would like to lock in today's exchange rates for use in the future, thereby protecting your international payments budget, please learn about the options available to you here.

"Sterling is OK for now, as the market is pulled one way then the other by Brexit uncertainty. However, if a 'hard Brexit' pushes the MPC into negative rates, the risk is that falling UK real yields take the pound down with them," says Soc Gen foreign exchange strategist Kit Juckes.

The Bank of England has been floating the idea of negative interest rates about for months now and have indicated research into the matter will be intensified before year-end. However, Bank of England Governor Andrew Bailey has so far opted to downplay the introduction of negative rates, which has offered support to UK yields and Sterling.

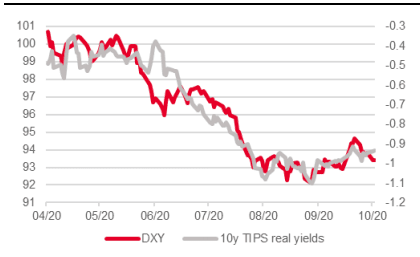

Soc Gen have meanwhile recently noted a recent widening in U.S./European yield differentials, which foreign exchange analysts at the investment bank say is proving to be supportive of the U.S. Dollar against the Euro.

Juckes notes that this would not necessarily be the case were Eurozone real yields higher.

Real yields (which account for future inflation) in the Eurozone would be higher if they were tracking nominal yields (which don't account for future moves in inflation).

Juckes says this phenomenon appears to be a result of the market's lack of faith in the ability of the European Central Bank (ECB) to stir inflation, thereby offering support for real yields in the Eurozone.

"The widening nominal yield gap is not being reflected in real yields, which are a better indicator of currency moves. When most central banks were targeting a 2% (inflation target in one form or other, and the market believed they would succeed in hitting it, nominal and real yield differentials tracked each other, the exception was Japan, mired in disinflation. Now though, the market has (some) faith that the Fed can overshoot its 2% inflation target and almost no faith in the ECB’s ability to get close to it," says Juckes.

Image courtesy of Societe Generale. If you would like to lock in today's exchange rates for use in the future, thereby protecting your international payments budget, please learn about the options available to you here.

The above chart shows the way the Dollar index - a broad measure of USD performance - has tracked the most uplift in U.S. real yields since the pandemic, a move that helps explain some of the strength in the Dollar during September.

"In the last few weeks it does support the idea of a modestly stronger Dollar," says Juckes of rising real U.S. yields.

"If U.S. rates continue spiking here the risk sentiment apple cart could be upset and keep the USD bears at bay," says Saxo Bank's John Hardy.

U.S. yields rose sharply this week, a move Hardy says is likely due to the Democrat candidate Joe Biden pulling ahead in the polls.

"Biden is pulling away in the polls is the chief driver and the argument here is that the Democrats are set to take back the presidency and the Senate, therefore paving the way for a massive multi-trillion stimulus passed in the first one hundred days of a Biden administration, taking US inflation much higher while leaving the Fed policy rate pegged near zero. The US dollar has clearly been driven by the market’s pricing of future inflation," says Hardy.

The findings hint that expectations for another leap higher by the Euro are potentially overly optimistic until such a time as markets are convinced inflation is returning to the Eurozone.

Eurozone headline inflation fell from -0.2 in August to -0.3% in September.

"Temporary factors are causing disinflation in the eurozone, but the longer it lasts the more worrying it becomes. That seems to give plenty of ammunition to the ECB doves to argue for more stimulus in December," says Bert Colijn, an economist at ING Bank N.V.

Colijn says a worrying aspect of the Eurozone's most recent inflation report is the drop in inflation within the services sector, which usually shows very little volatility and is a large component of the core inflation index.

Services inflation was 1.6% in February and has dropped to just 0.5% in September.

ING find that this is predominantly due to large drops in prices for services related to social distancing, which suggests to economists that the coronavirus has had a significant deflationary impact.

"For the European Central Bank, most of these factors ordinarily should not cause a change of direction. Still, core inflation this low is hard to ignore, especially since President Lagarde has recently put a lot of emphasis on the importance of the core measure. Also, the second round effects of low inflation for quite some time could become a factor for the medium-term expectations, which is enough for the doves to argue for more stimulus in December," says Colijn.