© Adobe Stock

- Formation of new Italian Gov addresses one downside risk to EUR.

- But is not enough to keep EUR afloat says MUFG and Credit Suisse.

- ECB rate policy and trade war both remain in driving seat of EUR.

- UBS eyes even "more aggressive" ECB policy action in September.

- As ING warns that 1.10 level is vulnerable into next ECB meeting.

The Euro ceded ground to the Dollar Thursday even after Italian political parties struck an agreement that averts a market-unfriendly general election, although analysts say this "noise" is not enough to offset more significant concerns about the U.S.-China trade war and European Central Bank (ECB) interest rate policy.

Italy's anti-establishment M5S party, the largest political force at the time of the March 2018 election, has agreed to throw its lot in with the Democratic Party (PD) in order to govern without having to return to the ballot box following the breakup of a coalition with Matteo Salvini's The League.

It's not yet clear whether such a formation can govern effectively for very long and in doing so, avoid new elections, but President Sergio Mattarella invited them to try on Thursday

#Quirinale, #Consultazioni: la dichiarazione alla stampa del Segretario Generale della Presidenza della Repubblica pic.twitter.com/NQdTQNHYfy

— Quirinale (@Quirinale) August 29, 2019

Salvini requested a confidence vote in his own government earlier this month in an effort to capitalise on surging support in opinion polls that now suggest The League has the backing of up to 40% of voters, although the gambit has reportedly resulted in the loss of some backers. One poll put the party on 33% this week, down around four percentage points from earlier August levels.

A general election was set to follow in the Autumn if M5S failed to form a coalition with establishment parties who its past criticism of, and opposition to, helped it built a political brand and sizeable support base among Italians. M5S received 29% of the vote in 2018 but its support in opinion polls has since fallen as low as 17% and was estimated at 19% this week. M5S members will have to approve, in an online ballot, the entry into coalition with the PD.

Above: Euro-to-Dollar rate at hourly intervals.

"A less expansionary budget and cancellation of the planned VAT hike now appears more likely further encouraging the adjustment lower in Italian government bond yields. With yields at record lows, the long-term sustainability of Italian public debt is less of a concern. It provides some much needed good news for the euro by removing a downside risk, although not sufficient on its own to reverse the euro’s gradual downward trend," says Lee Hardman, a currency analyst at MUFG.

The composition of Italy's new government is seen in the market as likely to mean the Meditteranean nation avoids another clash with European Union budget hawks in Brussels this Autumn. Italy feuded with Brussels under Salvini last year over spending pledges made in both League and M5S manifestos which put the country in breach of EU rules, drawing demands for the policies to be abandoned as well as threats of financial penalties if they weren't.

Thursday's developments are positive because they mean there's one less thing for the Euro to worry about in the months ahead, but analysts say they're unlikely to lift the single currency because Europe has a litany of problems that are much larger than running supranational battles over the Italian budget. Forecasts are increasingly suggesting the Euro will fall even further in the months ahead as the ECB seeks to support an ailing continental economy amid an escalating U.S.-China trade war.

"We are inclined to think that the risks to EURUSD from Italian political risk are more likely to generate noise, than to dictate a clear new directional outlook for the cross," says Alvise Marino, a strategist at Credit Suisse. "The market currently expects the ECB to cut interest rates by 12bps at its next meeting 12 September."

Above: Euro-to-Dollar rate shown at daily intervals.

"With the economic backdrop having deteriorated further since the last policy meeting, the ECB is likely to move more aggressively," says Frederick Mellors, a strategist at UBS Global Wealth Management. "The experience of Japan, where policymakers arguably did not react decisively enough, resulting in extended periods of deflation, likely rests heavily on their minds."

The ECB hinted in July that it will cut its interest rate again in September and potentially restart the quantitative easing programme that saw it buy almost a third of the European bond market between January 2015 and December 2018. But markets have long seen the ECB as being unable to cut its benchmark rates much below their current levels and so are positioned for oly a meagre reduction in the already-negative -0.4% deposit rate on September 12.

Benign expectations for ECB cuts are a threat to the Euro because Europe's problems are large and growing larger, while at least one influential voice at the bank has already advocated strongly for a 'shock and awe' style stimulus package that goes far beyond current market expectations. Such a thing would inevitably see 'yield' returns earned by investors in Eurozone financial assets further depressed at already-low levels, likely hurting the Euro.

"A package of easing measures from the ECB on 12 Sep (20bp deposit rate cut and €30bn per month QE) suggests EUR/$ support at 1.10 is vulnerable. Only a more aggressive Fed can help EUR/USD," says Chris Turner, head of FX strategy at ING.

Above: Euro-to-Dollar rate at weekly intervals.

Europe's economy has been hurt in the last year or so by a range of factors but most notably the U.S. trade war with China, which has slowed the world's second largest economy and particularly on the consumer side. That's hurting Europe because many of the bloc's car firms had bet the house on the Chinese luxury car market in recent years, but that market's now cratering.

Germany's economy is widely believed to be on the verge of recession as a result of the slowdown in global trade, which is happening right as a 'no deal' Brexit appears to be growing more likely by the day and as President Donald Trump pushes Brussels for a reduction in tariffs on American cars and farm goods under threat of U.S. levies on European goods.

"Without any near-term structural reforms coming from the fiscal side, the path of least resistance appears to be to do more of the same, loosening monetary policy even more and extending the period of low interest rates," says UBS' Mellors. "The easing may come in the form of a package of rate cuts and a new asset purchase program."

Economic woes are undermining the bloc's already-insufficient inflation pulse and necessitating stimulus that currency and bond markets are currently unprepared for. The ECB needs inflation to be at the target of "close to, but below 2%", although the core consumer price index has not been above 1.3% at all since the bank began its quantitative easing program in 2015.

The main inflation rate has been stuck below the target ever since November when oil prices began reversing earlier gains and if not for volatility in oil prices, the headline rate might not have seen the target level for years. Meanwhile, Eurozone GDP growth fell from 0.4% to 0.2% in the second quarter and the German economy contracted for a second time in the last year.

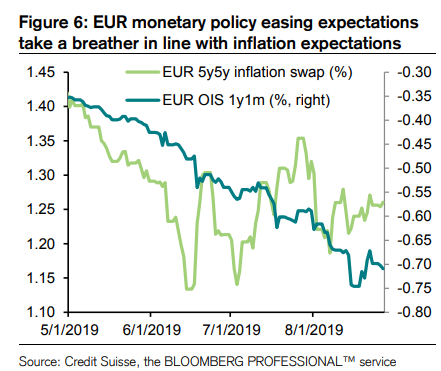

Above: Credit Suisse graph shows 5-year inflation expectation rising while 1-year-ahead ECB deposit

rate sits just 30 basis points below prevailing -0.4% rate.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement