© European Central Bank, reproduced under CC licensing

- EUR bests retreating USD, aided by ECB's Coeure Thursday.

- Coeure unperturbed by market fears over EUR inflation outlook.

- Says ECB should look at more favourable consumer expectations.

- But markets are looking for increasingly significant stimulus from ECB.

- Pantheon eyes German contraction, Eurozone slump and ECB rate cuts.

The Euro advanced against a retreating Dollar Thursday after European Central Bank (ECB) board member Benoit Coeure downplayed a recent increase in market fears over the outlook for the Eurozone economy, private sector forecasters are increasingly warning of trouble ahead.

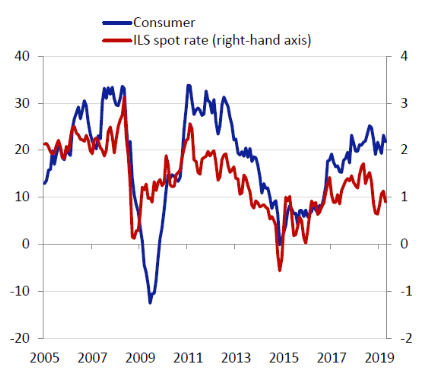

Benoit Coeure, one of the ECB's influential economists, told the SAFE Policy Center in Frankfurt Thursday that households and commercial firms are better at predicting inflation than financial market participants or forecasters, and argued for the ECB to be guided by these as well as by market concerns and forecasts.

"Households seem to look with much less scepticism into the future. Their inflation expectations have remained more stable since the start of the year, and today remain close to a six-year high. There is also tentative evidence suggesting that household inflation expectations are better predictors of future inflation outcomes," Coeure says. "All this confirms the need for central banks to consider and analyse developments in a broad set of inflation expectations."

Consumer inflation expectations have held around the ECB's 2% target throughout 2019 despite market expectations falling sharply. Market-based measures such as the five-year 'inflation swap' have pointed to steep falls in consumer prices up ahead and still imply investors see inflation remaining below the ECB's 2% target in five years.

Above: Consumer inflation expectations Vs market expectations (red line). Source: ECB.

If the ECB places more emphasis on consumer expectations than those of the market, the bank could then argue it doesn't need to take much action at all. But it if it goes with the market then the bank could be forced to implement bold measures in an effort to lift consumer price pressures. Measures which might weaken the Euro, particularly in the short-term.

"Such a drop in short and medium-term inflation expectations is particularly remarkable in an environment where highly volatile inflation components, such as energy prices, have remained relatively stable, and have even been rising since the start of the year. Recent market developments therefore suggest expectations that the current weakness in euro area and global demand will persist," Coeure told his audience.

Couere's suggestion the ECB should focus as much on the consumer expectations as it should the market's could explain why the Euro was trading so buoyantly on Thursday, as it might mean the ECB is less inclined to do as markets now expect and cut its interest rate later this summer.

Minutes of the ECB's latest policy meeting suggested on Thursday that markets could be right in thinking the bank is close to taking fresh action to support the Euro area economy and help lift inflation.

Waning expectations matter for the ECB because it's obliged to use interest rate policy to keep inflation "close to but below 2%", and Eurozone inflation has spent much of the time since the debt crisis well below that level. Core inflation, which economists see as the truer measure of price pressures, has not been above 1.4% in all that time.

"The ECB minutes continued to prepare a ground for further easing. However, Coeuré played down the role of market-based inflation expectations which supports the view that they will not hurry. We continue to expect a new easing package in September," says Tuuli Koivu, an economist at Nordea Markets.

Above: Euro-to-Dollar rate shown at hourly intervals.

Inflation is impacted by many things but most notably economic demand, which has been weak in the Eurozone ever since the debt crisis and has ebbed in the last year due to the U.S. trade war with China and a range of other factors. Eurozone growth fell from 2.3% in 2017 to 1.8% last year, although even the European Commission doubts that it'll come in much more than 1.2% this year.

The Eurozone economy, like many others, has slowed in line with a fall in business confidence resulting from the U.S. trade war with China. Furthermore, both the European Union and UK economies are yet to arrive at the end point for the Brexit process, which could also have an impact on the economic outlook. These factors that have slowed the economy and dented the growth outlook have also helped drive inflation expectations lower.

"Judging by the monthly data, everything went wrong in the German economy in Q2," says Claus Vistesen, chief Eurozone economist at Pantheon Macroeconomics. "Our model currently suggests that GDP crashed by nearly 0.6% quarter-on-quarter in Q2, fully reversing the 0.4% increase in Q1."

German industrial output rose 0.3% in May but much of this was simply "mean reversion" from a low base after previous falls. Meanwhile, the details of the report revealed the construction sector output began to decline that month after previously having supported the economy. The trade balance also mean reverted thanks to a 1.1% increase in exports and a 0.5% decline in imports. However, this was only after exports fell 3.4% in April, which still leaves "net trade" as a drag on second quarter GDP growth.

"It is difficult to escape the idea that GDP fell outright in the second quarter. Our base case is a 0.2% decline, driving the year-over-year rate down by 0.6pp, to zero,2 Vistesen says. "More pertinently, a hit to the German economy would feed negatively into the EZ headline—we look for Q2 growth of 0.1% q/q—which, in turn, supports our forecast for the ECB to ease further."

Above: Euro-to-Dollar rate shown at daily intervals.

If Pantheon is right in its forecasts for the German and Eurozone economies in the second quarter then 2019 GDP growth could be substantially below even the latest estimates of the European Commission, which would be unwelcome news that bodes ill for the inflation outlook of the European Central Bank.

Falling growth and inflation have now got investors widely anticipating at least one interest rate cut from the European Central Bank this summer while some analysts and economists are also suggesting the central bank could restart its quantitative easing program in an effort to stimulate the economy.

"We are not betting on more QE at the ECB," Vistesen says. "Our base case remains a 10bp cut in the deposit rate, to -0.5%, in September. That said, if the implied change of 20bp, based on Euribor futures, remains stable through this month’s meeting, we are liable to nudge our forecast down."

Vistesen says the market consensus for ECB action is shifting in favour of a fresh quantitative easing program that would see the bank buy European bonds in an effort to stimulate economic growth and inflation by forcing down government and corporate bond yields.

That's in addition to cutting its interest rate further below zero. It wasn't until December 2018 that the ECB managed to wean the market off its earlier bond buying program, which was announced in January 2015.

The ECB left its refinancing rate, marginal lending rate and deposit rate unchanged at 0%, 0.25% and -0.4% respectively in June but Draghi told an audience in the Portuguese city of Sintra that if inflation doesn't pick up toward the target of "close to but below 2%" then additional stimulus could be required. He specifically mentioned the prospect of further deposit rate cuts and another quantitative easing program.

Pantheon's forecast for a 0.1% interest rate cut in September will be changed to 0.2% if at the end of July markets are still betting on a greater reduction, Vistesen says. But regardless of whether the ECB cuts rates, restarts its quantitative easing program or does both, the Euro could suffer as a result.

This is because changes in interest rates and bond yields have significant influence over capital flows and the decisions of short-term speculators. Capital flows tend to move in the direction of the most advantageous or improving returns, with a threat of lower rates normally seeing investors driven out of and deterred away from a currency. Rising rates have the opposite effect.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement