Image © Grecaud Paul, Adobe Stock

- The Euro is being pinned down by poor data

- One factor is the price of oil

- Could relief from lower fuel prices support growth in Q4?

One major headwind to the outlook for the Euro exchange rate complex is slowing Eurozone growth; while it is not the only factor keeping the single currency down it is one of what we believe to be the top three main sources of weakness, the other two being Italian politics and the threat of U.S. auto tariffs.

Eurozone growth came in at a paltry 0.2% in Q3, which was well below economists expectations of 0.4%, and the previous quarter’s 0.4% rate. It was even lower than Brexit-embroiled Britain, which managed a comparatively respectable 0.6%.

The slowdown has raised concerns that the European Central Bank (ECB) might do a U-turn on its plan to normalise monetary policy - a move which is believed to already be weighing on the Euro and bodes for further weakness over coming months if the view becomes more entrenched amongst market participants.

The ECB’s current plan is to remove stimulus at the end of 2018 and to start raising interest rates after the summer of 2019. If it diverges from this it would send out a signal that the region was still in need of a ‘life-support machine’ and potentially lead to a further step down in the value of the Euro.

The big question now is whether Eurozone growth will continue a trend of weakness in Q4 and beyond and whether the ECB will continue to stick to its normalisation roadmap.

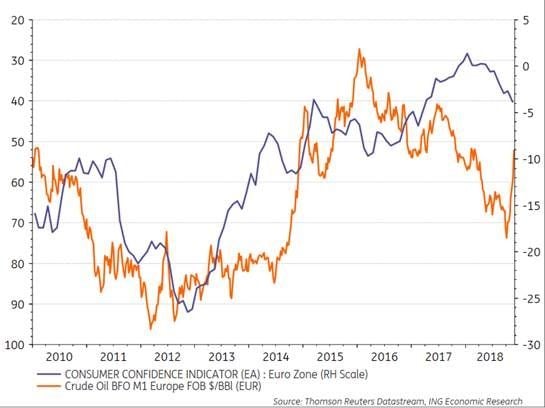

One major consideration in the puzzle of Eurozone growth is the price of oil. Anyone doubting this should watch the footage of the recent fuel tax riots in Paris.

Whilst the protests began because of a proposed increase in fuel taxes the already high base cost of petrol provided the underlying ‘tinder’ for the eventual upwelling of outrage.

In its most recent assessment of the region, the IMF highlighted higher fuel prices as a major factor in the region’s slowdown.

“Higher energy prices helped dampen demand in energy importers,” say the IMF, which also listed political uncertainty as another major factor impacting growth in a recent global economic assessment.

Oil price dynamics will be a major influencer on the ECB’s policy-making too.

“The surge in oil prices since the beginning of the year is probably the single biggest problem for the ECB,” said Carsten Brzeski, an economist at ING.

Put simply, higher fuel costs have been stunting Eurozone growth for the greater part of 2018.

The problem is exacerbated by the fact that the region has to import 98% of its fuel needs and by the historically low EUR/USD exchange rate. Oil is sold in U.S. Dollars so the weaker Euro has magnified the cost of the commodity for Euro-area importers.

Oil prices peaked in Q3 at $76 a barrel in October, which coincided with the sharp drop in GDP growth. This was arguably not a coincidence, according to some economists.

“The oil price increase has hampered growth (see correlation between oil price and consumer sentiment) in Europe (apart from some production delays in the car industry in Germany),” says Peter Vanden Houte, Chief Economist at ING N.V.

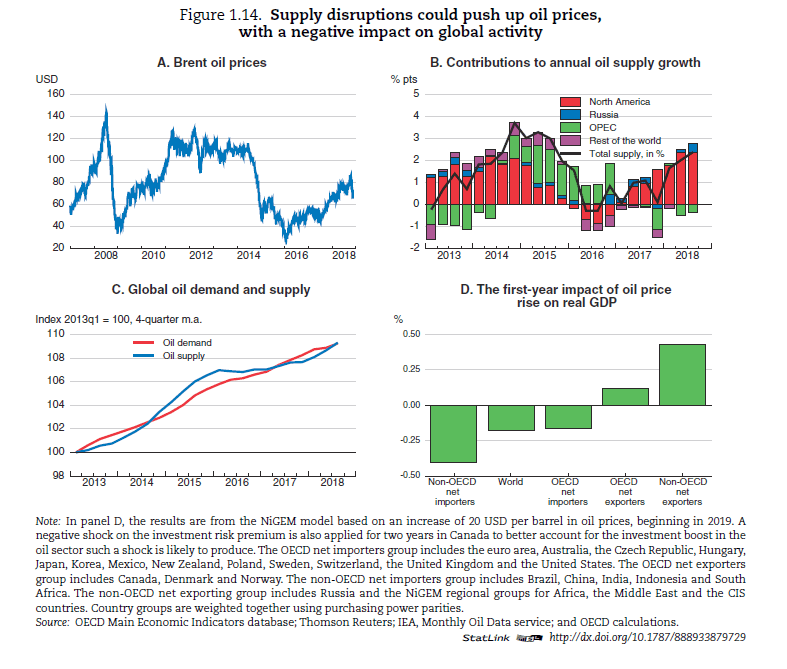

Given high oil prices weigh on growth, their recent sharp decline should also logically benefit Eurozone growth. Does this suggest the possibility of an uptick in Q4 data?

“We might see the opposite effect in Q4 2018 and Q1 2019.” Says Vanden Houte. “According to OECD estimates the fall in oil prices, if sustained might add 0.15 to 0.2% to GDP growth (see slide). Therefore we are certainly not looking at a recession.”

ING’s official quarterly growth forecast is for a middling 0.3% rate, which would be slightly better than Q3 but not as good as Qs 1 and 2. Nevertheless, it would probably keep the ECB on track for tightening in 2019.

The price of oil is not the only factor hampering growth in Europe.

Other key influences cited by economists include the cold winter, the decision to ban diesel cars in Germany, the fading effect of the ECB’s stimulus measures, manufacturing capacity constraints creating bottlenecks, while the extremely high rate of growth in 2017 making anything less than stellar growth in 2018 look comparably slow.

Political uncertainty in Italy and the UK, a weak emerging market, the lack of further reduction in the unemployment rate which has remained stagnant at 8.1% for four months, an ageing population, and low productivity are also at play.

Also, whilst the Euro is considered weak versus the US Dollar it remains relatively strong on a broader trade-weighted basis and this has hampered export competitiveness.

“We mustn’t forget either that in trade-weighted terms the euro is very strong (you wouldn’t think this looking at the euro-dollar exchange rate) and this is having some deflationary impact on the Eurozone economy. We also see that exports are under pressure because of the slowdown in the emerging world. Throw in some political uncertainty (Brexit, Italy) and it still looks likely that growth will be 1.5% at most,” says Vanden Houte.

The complexity of the problem will not be lost on the ECB. They may feel ‘damned if they do damned if they don’t’. Policies which weaken the Euro and restore export competitiveness will have the unwelcome side-effect of also weakening the Euro versus the US Dollar and thus raising the cost of imported fuel.

This also comes at a time when it looks increasingly like OPEC will cut supply to put a safety net under the oil market.

The most probable outcome, this writer humbly surmises, is for the ECB to continue with its current stance, along the lines of the proverb ‘when in doubt do nothing’.

Advertisement

Bank-beating exchange rates: Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here