Image © European Central Bank

- EUR/USD to trade with a bearish tilt until mid-November possibly later

- After that stars will align for the Euro and pair should recover

- Dollar liquidity shortage a factor driving EUR/USD down now but this will end in November

The EUR/USD exchange rate is likely to "have a downside tilt" for the next month or so, according to analysts at Nordea Bank; but from the middle of November, it is tipped to recover.

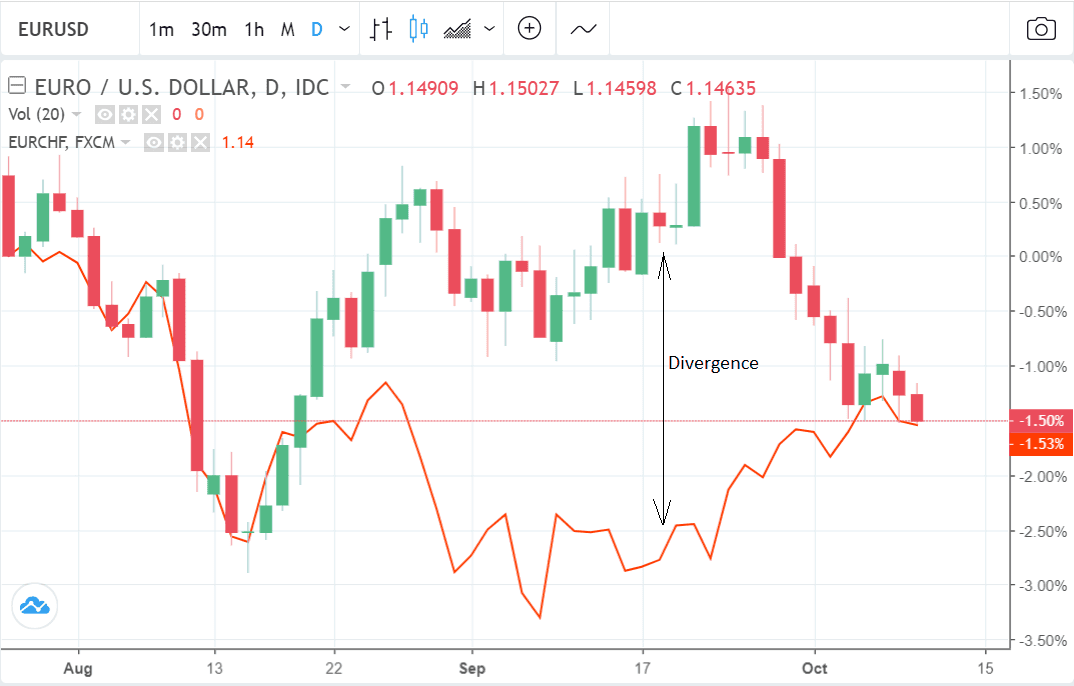

Although most market commentators have put the recent bout of EUR/USD weakness down to investor concerns about the Italian budget, Nordea argues the more pressing reason for the pair's decline is US Dollar strength, not Euro weakness.

Evidence for this comes from the fact that the EUR/CHF has risen recently - which would not have happened if the problem rested solely with the Euro.

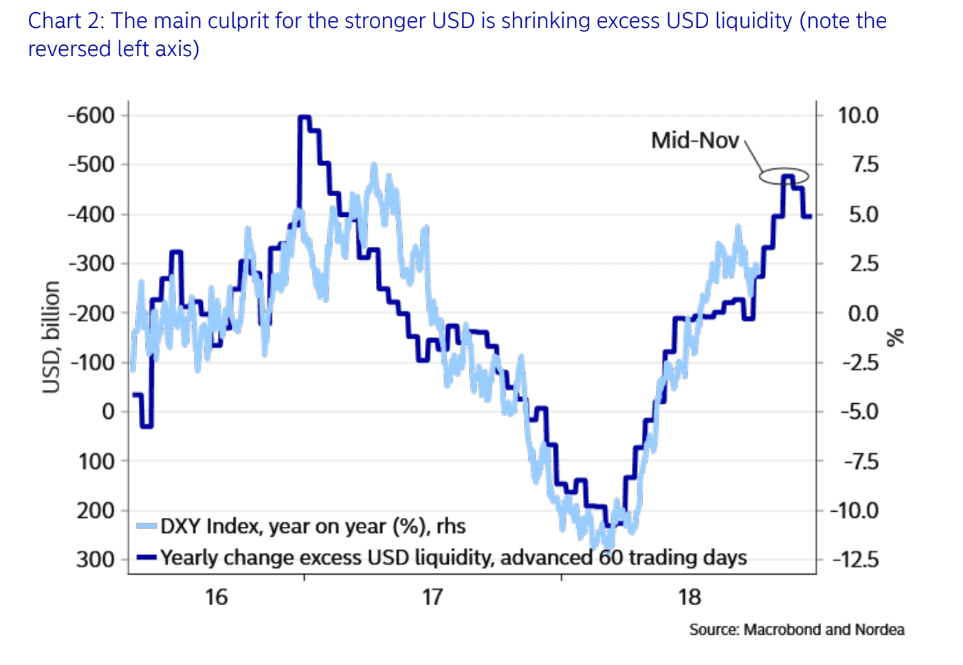

Shrinking US Dollar liquidity is the main reason for the Dollar's strength, says Nordea, caused by a combination of the US Federal Reserve ending its policy of reinvesting principal from its bond redemptions; falling US tax revenue due to Trump's tax cuts; and the fact the US Treasury has a policy of keeping circa $300bn in reserve (for emergencies) at all times - an amount which periodically needs topping up.

These three main factors have 'hoovered' up US Dollars from the economy and created the US Dollar-scarcity problem which is driving up the currency's value.

Nordea's estimates of US Dollar liquidity, at a 60-day lag, closely correlate with the US Dollar Index.

The bank forecasts that in about mid-November the US Dollar could peak when the US hits its debt ceiling.

Unable to borrow to cover the shortfall between revenue and spending the US Treasury will have to raid its reserves, injecting circa $300bn into the economy, increasing liquidity and weakening the US Dollar.

"On our lead/lag studies, the USD will peak in Mid-November seen from an excess liquidity momentum perspective," say Andreas Steno Larsen and Martin Enlund, chief analysts at Nordea Bank in a recent report.

"A trend reversal that could be further fuelled, if we get another debt ceiling stand off in early 2019 (a likely scenario, especially if the Republicans lose the majority in the house). In such case the US Treasury will empty its cash balance at the Fed, flushing the commercial banking system with up to $3-400BN (a USD negative scenario)," add the analysts.

If there is no debt-ceiling stand-off the US Dollar peak may be delayed until the start of 2019.

Other factors which have aided the Dollar's uptrend are Chairman Powell's recent comments about US interest rates being likely to surpass the 'neutral rate' - the Goldilocks 'just right' level where they are when the economy is neither growing nor shrinking.

Another factor has been the steeper US Treasury yield curve, which suggests a strong growth outlook longer-term, and is, therefore, a greater draw for foreign investor inflows.

Italian Headwinds to Fade

Of course, the Euro has also participated in its own decline.

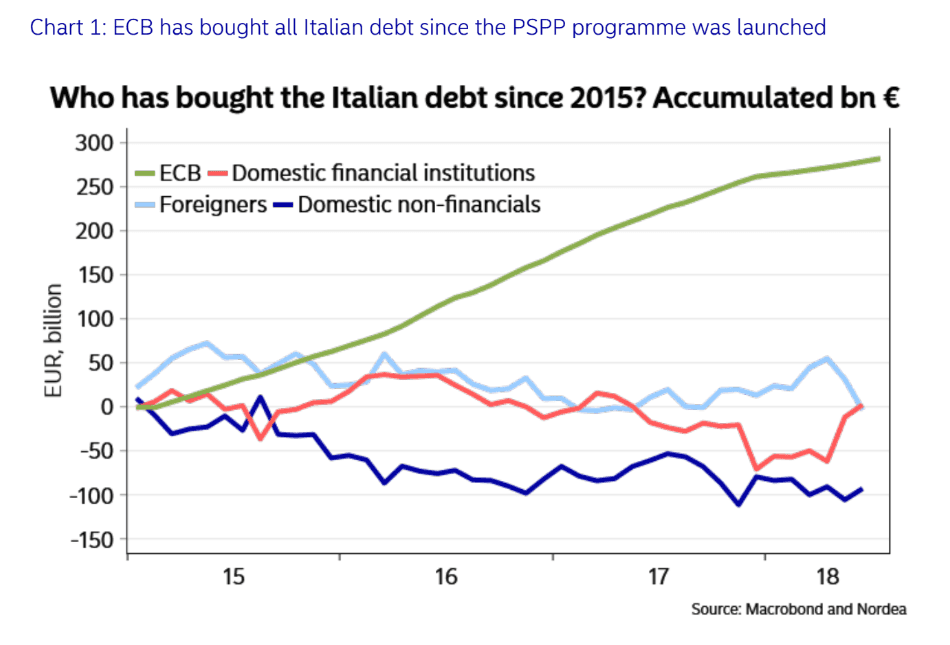

Concerns over Italy have been a contributing factor but Nordea thinks that these will resolve in time. The Italian government has already made concessions by lowering the budget deficit to 2.0% in 2020 and 2021 from 2.4% in their initial proposal.

Nordea thinks more retreats will follow as financial reality wins over ideology.

"Sooner not later Luigi Di Maio and Matteo Salvini will have to dance after the markets tune. That is simply needed to avoid catastrophe," say Larsen and Enlund.

One of main reasons they are so sure of this is because almost all the money the Italian government borrows comes from the European Central Bank's quantitative easing stimulus programme, which is set to close at the end of the year.

Once this source of discounted funding is removed Italy will have to go cap-in-hand to outside capital markets which will almost certainly be less forgiving. This is almost certain to push up the cost of borrowing. Once Italian politicians grasp this fact they may relent. Further concessions should resolve the crisis and take some pressure off the Euro.

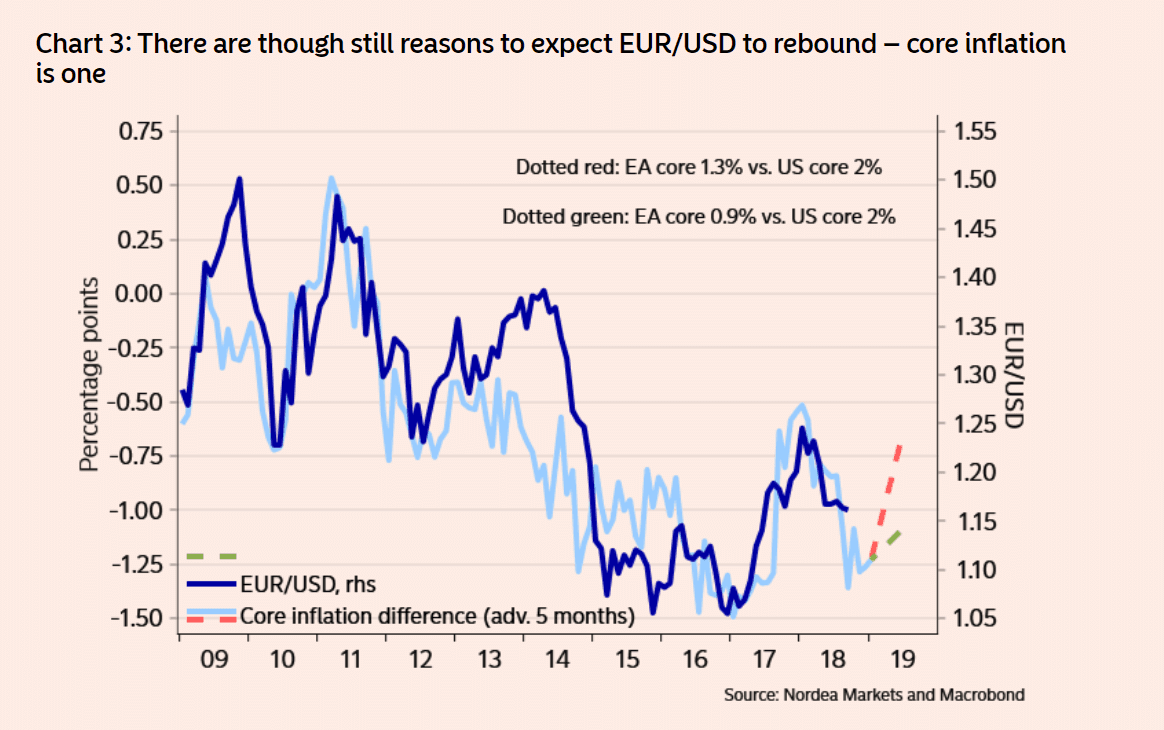

Another source of renewal for the single currency may come from a closing inflation spread between US and Eurozone, says Nordea.

Up until now the spread has been quite wide and this has put downward pressure on EUR/USD, however, this is set to reverse.

The most recent fall in core Eurozone inflation back down to 0.9% did not bode well for the Euro as it suggested the ECB might have to delay putting up interest rates, however, this is probably the 'bottom of the barrel' for Eurozone inflation which is likely to rise from here and close the gap with the US.

A final driver for Euro gains versus the Dollar could come from the fall-out from worsening China-US trade war, according to Deutsche Bank.

Increasing trade tensions between the U.S. and China could lead to a diversion of trade away from the U.S. and more towards Europe. This will increase European imports to China.

Recent Chinese trade data from July already showed this happening with European imports surging 51% in only a month.

If the trend continues it will strengthen the Euro at the Dollar's expense.

Advertisement

Get up to 5% more foreign exchange for international payments by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here