Image © Lakov Kalinin, Adobe Stock

- Pound Sterling remains vulnerable to further weakness

- GBP/EUR could sell-off down to the 1.10s if Brexit risks materialise

- Main calendar release for Sterling is Q2 GDP - for the Euro the ECB's Economic Bulletin

Pound Sterling is under pressure at the start of the new week, in sympathy with growing fears for a 'no deal' Brexit and the technical downward trend that has been alive since April.

Headlines pushing Sterling lower pertain to the chances of a 'no Brexit' deal with UK Trade Secretary Liam Fox telling the media at the weekend that the prospects of a 'no deal' outcome are now at 60%.

"GBP continues to suffer on Fox's 60 pct no deal Brexit estimate," says Robert Howard, who sits on the currencies desk at Thomson Reuters. "Sterling's fear factor is rising fast."

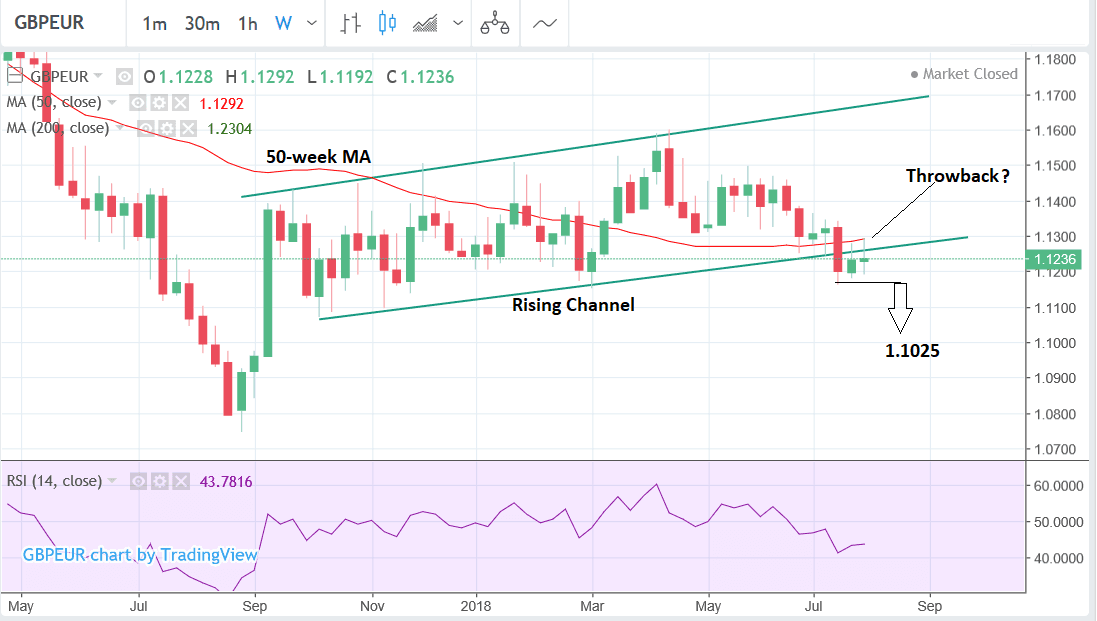

Our latest technical studies suggest the outlook is little changed for GBP/EUR from last week; Sterling remains precariously perched just below its major long-term range/rising channel.

There is no question GBP/EUR has made a clear downside break out of the channel - the question now is will it follow through lower?

The pair has recovered back to the floor of the range over the last two weeks following the initial break, but this does not mean a full-blown reversal is nigh. This pull-back could merely be what analysts call a 'throwback' move, which is when prices retrace for a moment following an initial break, like a pause after all the hard work of knocking through the level. Once prices have retouched the original level the market usually resumes its downtrend with renewed force and vigour.

Thus if the recovery on GBP/EUR is in fact such a throwback - as it probably is - it could keep bearish hopes very much alive. The fact the 50-week Moving Average (MA) is also acting as a resistance level is a further headwind for struggling bulls. Major MA's like the 50 often act as incredibly tough obstacles where prices get stuck or reverse.

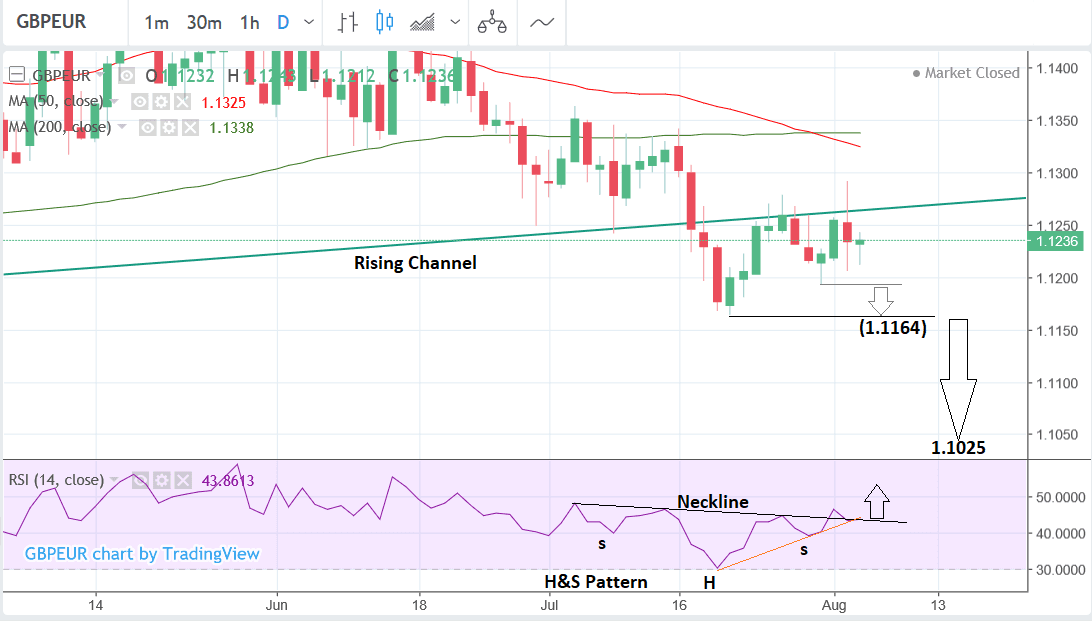

The one piece of evidence which is contradicting the throwback hypothesis is the bullish look and feel of the RSI momentum indicator on the daily chart (below).

This appears to have formed an inverse head and shoulders (H&S) pattern which is a bullish indicator for momentum and, therefore, also probably for the underlying exchange rate.

The inverse H&S has temporarily broken above its 'neckline' - a confirmation level at the pattern highs, which should confirm more upside. Yet after the break, momentum has so far failed to follow-through. It is now at a make-or-break level back at the neckline again after tracing its own 'throwback'.

From here it could go higher, but at the same time if it were to fail and move lower it would be at risk of negating the pattern if it fell below the orange line joining the head with the right shoulder.

Such a breakdown would flip momentum and suggest more downside inside.

Overall, a break below the 1.1192 lows of July 31 would be a bearish signal on the daily chart which would probably confirm a move down to the 1.1164 lows of the July 20 lows.

It would require a break below those July 20 lows, however, to signal a continuation down to the next downside target at 1.1025 calculated by taking the golden ratio (0.618) of the height of the channel and extrapolating it lower from the breakpoint.

Advertisement

Get up to 5% more foreign exchange for international payments by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

The Calendar for the Pound

Last week's price action confirms the Pound is not really paying much attention to Bank of England interest rates, and thus economic activity.

Instead, persistent concerns of the shape of Brexit negotiations remain the key driver.

Sterling took a dip ahead of the weekend after Bank of England Governor Mark Carney said on BBC Radio 4 that the risks of a 'no-deal' scenario are now "uncomfortably high".

In the week ahead, therefore, the main focus is going to be on the odds of a 'no-deal' materialising.

Prime Minister Theresa May cut short her holiday to meet French president Emmanuel Macron at his Riviera retreat over the weekend in an effort to gain more support for her proposals.

In the week ahead there is likely to be much focus on the outcome of this meeting. Early signs are Mr Macron has made it clear he does not want to 'go over the head' of his chief negotiator Michel Barnier, so its questionable whether the meeting achieved any traction for May's plans.

Barnier has been critical of May's plan saying the idea of the UK collecting tariffs on behalf of the EU 'unworkable', but without this element of the deal the UK will not be able to forge unilateral trade deals with third parties, killing the dream of new alliances, and making it completely unpalatable to already-sceptical Brexiteers.

May has already had problems uniting her party behind her plan and there remain many dissenters who think her proposals are too concessionary.

She therefore lacks any further negotiating slack to compromise with the EU, and this is why governor Carney has raised his risk assessment of a 'no-deal' outcome.

May's has given as many concessions as she can, yet it's not far enough for the EU. An intractable deadlock appears to be the new threat on the horizon and currency markets are expressing this by keeping Sterling under pressure.

From a hard data perspective the week ahead is fairly quiet, which is likely to further magnify Brexit as a driver.

The main release is Q2 GDP on Friday August 10 at 9.30 B.S.T, which is forecast to show a 0.4% rise after Q1's disappointing 0.2%.

Q2 GDP will be important mainly as a benchmark for comparing Q1 - if it really does come out at 0.4% then everyone will be relieved at the rebound and those who said the slowdown in Q1 was just a 'blip' due to 'the weather', will be vindicated. If, however, Q2 also shows a slowdown then economists will start to wonder whether this part of a deeper more troubling decline. Sterling may react.

Other important data in the week ahead includes the Trade Balance in June, released at the same time as GDP, which is forecast to show a -11.95bn deficit versus -12.36bn previously.

Industrial production is also out at the same time and forecast to show a 0.4% rebound in June. Manufacturing production, likewise, out at the same time and expected to show a 0.3% rise in June.

The Royal Institute of Chartered Surveyors (RICS) house price monitor is out at 00.01 on Tuesday. it showed a 1.1% positive score in June. The RICS monitor is composed of survey answers from surveyors about whether they think house prices have gone up, down or no-change.

Business Investment on Friday at 9.30, Halifax house prices and the BRC Retail sales monitor are out on Tuesday, and New Car Sales on Monday morning at 8.00, are further releases on the UK economic calendar.

What to Watch for the Euro

The main release in the week ahead for the Euro is the European Central Bank's Economic Bulletin out on Thursday, August 09 at 9.00 B.S.T.

This will present the latest assessment of the Eurozone economy by the European Central Bank (ECB) and will therefore be closely watched by analysts and traders.

Economic indicators in the region have given conflicting signals, with PMI's showing robustness but GDP growth disappointment - the bulletin may shed light on these discrepancies and provide insight into the ECB's views of the economy's trajectory in H2.

If its positive it could boost the single currency.

The other main release for the Euro-area is the Retail PMI for July, out at 8.10 on Monday morning. The stat showed a 51.8 result in June.

Advertisement

Get up to 5% more foreign exchange for international payments by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here