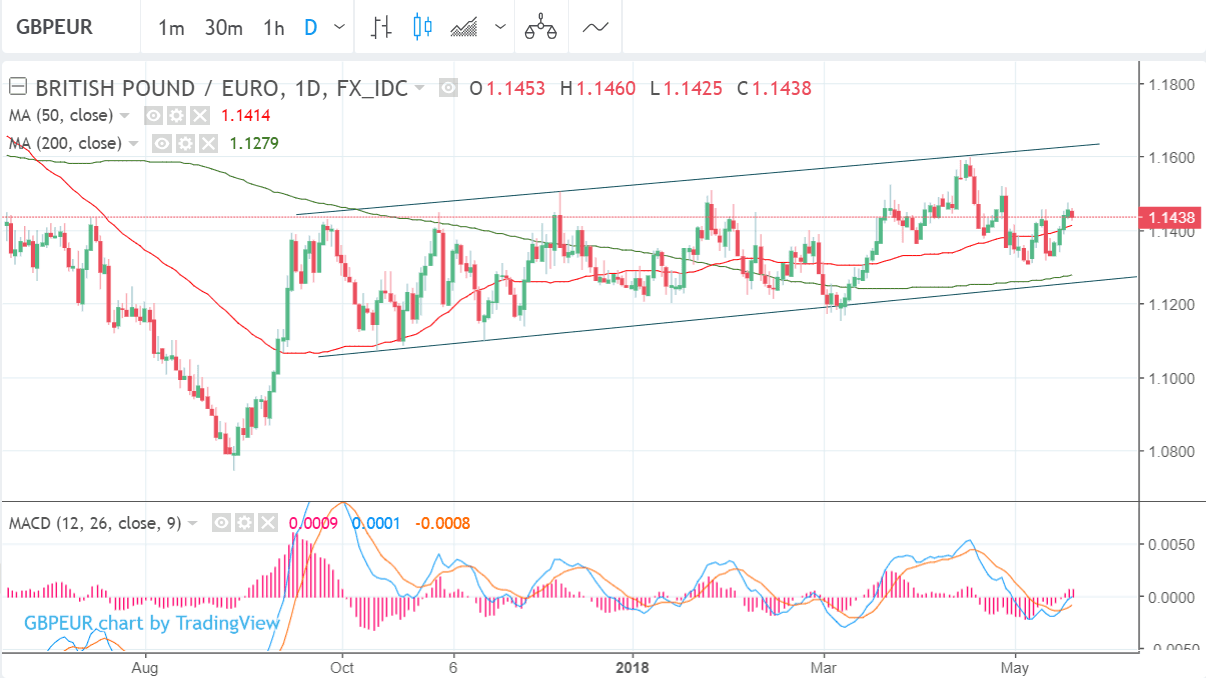

- GBP/EUR continues to trade in a range it has been in since 2017

- The Pound faces inflation and retail sales data in the week ahead

- For the Euro, the main data release is PMI survey data for May

© John Gomez, Adobe Stock

A Pound buys 1.1417 Euros at the time of writing, 0.32% less than it did at the start of the new week amidst signs of broadbased Sterling weakness.

While the Pound starts the week on the back-foot we would caution that any weakness is unlikely to prove persistent in the absence of notably bad news concerning Brexit or the economy; risks we don't see in the immediate future. Indeed, the Euro has its own political considerations to fret over now that a populist coalition is about to take the reins of power in Italy.

Technical considerations are certainly likely to play a part in the currency pair's direction as GBP/EUR is back in the middle of a well-trodden range, in fact, looking at the exchange rate reminds us that markets can go sideways for an awful long time.

In the case of GBP/EUR the pair has meandered within a tight range between 1.1100 and 1.1600 since September 2017.

Try to stay awake though; it's a truth in financial markets as well as life that 'dead' periods normally precede periods of high volatility.

When the breakout finally comes we previously expected it to be higher; now we are less sure - a double-dip back down to the 1.07s does not seem as strange as it once seemed.

There is little the charts can add or illuminate for investors in this situation - the pair is going sideways and that's about the sum of it.

If pressed, we are marginally more bullish in the medium and long-term, expecting an eventual breakout higher, but not as set on that outcome as we were previously.

In the meantime the pair appears to be basing within the range and starting to move higher, but its difficult to forecast a continuation up to the range highs in the 1.15s - the pair could just as well capitulate back down to the 1.13s again.

None of the indicators are very helpful in these situations either.

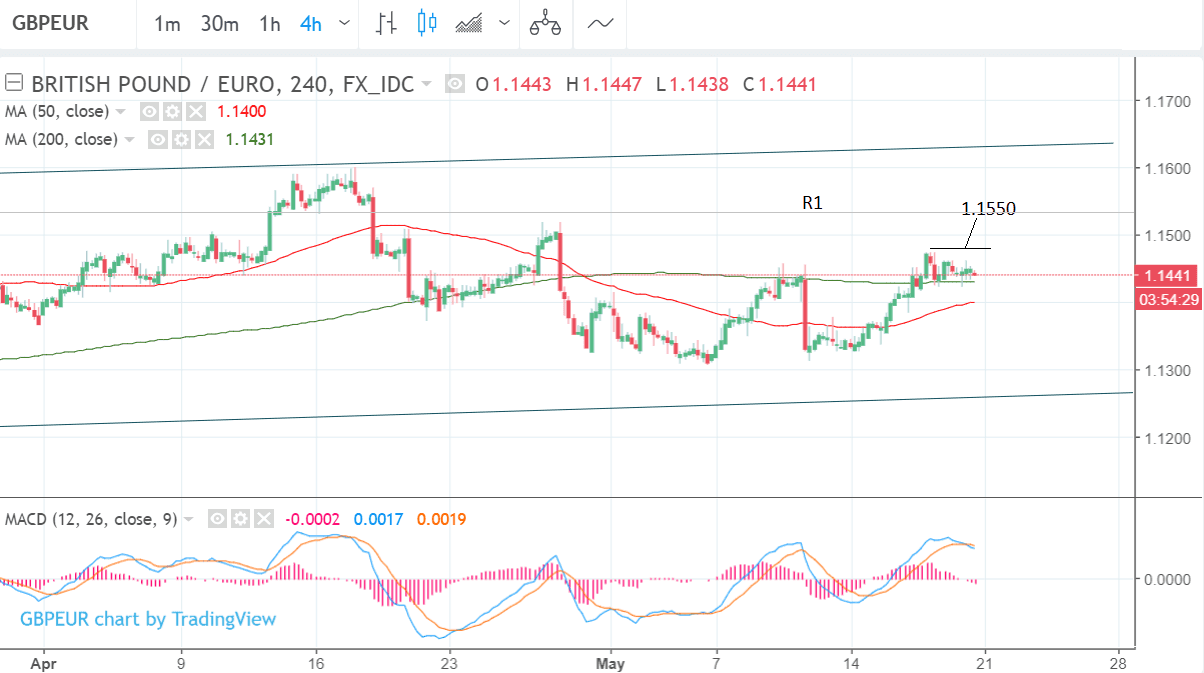

The 4-hour chart shows the pair trading with a marginal upside bias after forming steadily higher lows and higher highs; yet it is not particularly convincing.

Nevertheless, for those struggling rudderless in unsympathetic 'seas' the upside is to be marginally prefered.

As such, a break above the 1.1474 highs would probably confirm a continuation up to a target at 1.1550 where the obstacle of the R1 monthly pivot kicks in.

Monthly pivots are levels on charts used by traders to gauge the trend. They also offer support and resistance to prices in and of themsleves acting as 'real' barriers to the trend on price charts, thus the pivot at 1.1553 may well stall any uptrend assuming one evolves.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

GBP: What to Watch

It's a busy week ahead for Sterling traders, with a welter of economic releases due for the Pound.

Inflation data, out at 9.30 on Wednesday, forms the main data event with traders looking to see whether prices are moving in a direction consistent with further interest rate rises at the Bank of England. Over recent months we have seen the Pound become increasingly attuned to Bank of England interest rate expectations; moving higher when expectations for a rate rise increase, and moving lower when those expectations are rowed back.

We recently reported that economists at Capital Economics are expecting two interest rate rises in 2018 which would present an highly bullish outcome for Sterling, but the data will have to start moving in the right direction very soon for this assumption to prove correct.

And of course, the Bank of England is watching the data and will only move on rates once they have evidence the economy is picking up pace once more.

"UK inflation figures from April will be closely watched by markets and influence the pricing of Bank of England," says Andreas Steno Larsen, a strategist at Nordea Bank.

Inflation is expected to fall to 2.1% from 2.3% as base effects from the weak Pound start to fall away.

"As for April there is a clear risk of a rather low result due to base effects," adds Larsen.

Analysts at Investec are more bullish about inflation in April:

"We expect to see inflation tick up to 2.6% from 2.5%, albeit with the April rise likely to be a blip on a path in which we see inflation moderating," says Investec economist Victoria Clarke.

Global oil prices have been on the rise, and we would expect this to perhaps deliver an upside surprise. However, the core CPI release will therefore be crucial as it strips out the likes of external one-offs like oil, and the Bank of England uses the number as a proxy for underlying wage growth. In short, a beat on the core CPI would likely help Sterling higher, core is forecast to read at 0.5%.

In other UK releases, retail sales figures due Thursday morning will also be closely watched amidst concerns about UK growth (and consumer spending) momentum.

The BRC’s April figures were particularly weak, with the timing of Easter a depressing factor; we suspect the ONS’s Easter timing adjusted numbers will not look quite so gloomy.

The second estimate for UK GDP growth is due at the end of the week where Clarke suspects we will see an unrevised reading of +0.1% print. A beat would however likely boost Sterling.

Right at the beginning of the week we get some second-tier numbers with public sector finances released at 9.30, they are expected to show government borrowing fall by 7.0bn in April. Recent public sector data has been positive on the whole so a further fall in borrowing would be seen as a positive for the economy, although a surprise reading either way would pobably be necessary to move the Pound.

The Consortium of British Industry will also be releasing two reports for the month of May: the CBI Industrial Trends survey at 11.00 GMT on Monday and the Distributive Trades survey at the same time on Wednesday. Both will provide the most up-to-date information on economic activity in the UK and could, because of their timeliness, impact on Sterling.

EUR: What to Watch

Political risks have risen of late for the Euro - after the relief that followed Macron's historic victory over Le Pen markets are now having to entertain the prospect of an Euro-sceptic coalition taking power in Italy which has renewed the political risk-premium for the Euro.

We will be watching developments here closely over coming days.

The key release for the Euro in the week ahead will be the preliminary estimates of Eurozone PMIs for Services and Manaufcaturing in the region, in the month of May, which will be released at 9.00 GMT on Wednesday, May 23.

PMI's are activity metrics generated by survey responses from pivotal procurement managers. They provide a timely and accurate gauge of levels of activity within the economy.

Because they will provide the first insight into the health of the economy in May they will be vierwed as providing confirmation of whether the slowdown in Q1 has extended into Q2. If there are signs of a continued slowdown into Q2 the result may lead to weakness in the Euro.

A loss of growth in Q2 after the poor Q1 will begin to weigh on current expectations that the European Central Bank (ECB) will remove emergency stimulus by the end of the year, and it is only after they remove stimulus that they can begin raising interest rates.

Higher interest rates drive up the value of currencies as they attract greater inflows of foreign capital drawn by the promise of higher returns.

"Debate has continued over whether softer Q1 economic data, in a number of geographies, signals a cyclical downshift in momentum or a temporary blip," says Philip Shaw, analyst at Investec, adding, "From the Euro area, the ‘flash’ PMIs for May are due, providing the ECB with a key source of information on the direction of change in EU19 economic momentum ahead of its June ECB meeting and forecast round," he adds.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.