- 1.20 a possible target in next three months say Commerzbank's Jones

- Lloyds eye near-term restistance targets in 1.17-1.1730 region

- ING say risks are Sterling-Euro hits year-end target sooner rather than later

© Lakov Kalinin, Adobe Stock

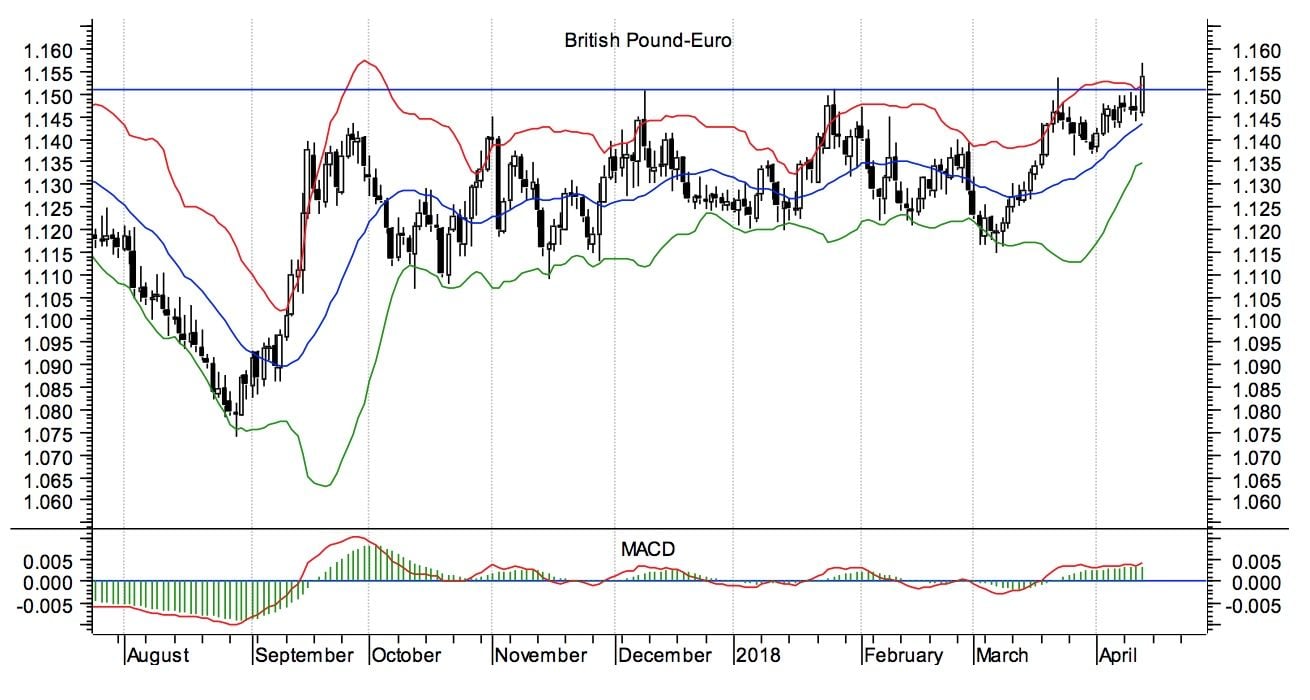

The Pound-to-Euro exchange rate has moved sharply higher over the course of the past 24 hours and has finally delivered a break of the key 1.15 resistance area and recording a fresh ten-month high of 1.1589.

The move is significant in that the multi-month range that lies between 1.11 at the bottom and 1.15 at the top has been broken thanks to a strong impulse of Sterling buying that has been in place since early March.

At the time of writing 1 Pound buys 1.1579 Euros on the inter-bank markets as Sterling strength accelerates and looking at the retail market, those with Euro-based international payments could be getting rates as high as 1.1468 with Horizon Currency ltd.

The question is can we expect even better exchange rates for those holding Sterling; where next for the exchange rate now that it is on the move? We have checked-in with those technical strategists we follow for clues on the outlook, and find that overall the outlook remains constructive for Sterling.

Karen Jones at Commerzbank notes the GBP/EUR exchange rate "has at last" broken up from the ceiling of its range and she continues to target 1.1730.

The technical analyst identifies this target at the 78.6% retracement of the move from 2017.

Near-term, the Euro is expected to remain offered while the GBP/EUR exchange rate is above 1.1363/1.1350.

Initial support to any subsequent Sterling weakness is identified at the 1.1465 near-term uptrend line. Jones notes the intraday Elliott wave counts remain positive while confirming a buy signal exists on the DMI.

Concerning the short-Term trend (1-3 weeks), Jones has an initial target at 1.1728.

Long-term trend (1-3 months), Jones initially targets 1.2027 which is the April 2017 high.

Robin Wilkin, an analyst with Lloyds Bank Commercial Banking meanwhile warns that for the Euro, "momentum and seasonals remain bearish, so a break here would risk a further extension lower".

The next main support for EUR/GBP is not seen till the 0.8550-0.8525 region, which translates into the next resistance targets for GBP/EUR being located in the 1.17-1.1730 region.

Bill McNamara, who heads up The Technical Trader service, tells his clients that Sterling is "on the move" and flags recent Sterling-Euro chart action as his "chart of the day," now that recent price action has "taken the UK currency to its highest reading relative to the Euro in ten months".

McNamara's studies suggest the GBP/EUR exchange rate might finally be breaking out of the range that has been keeping it in check over the last few months, where resistance has been evident at around 1.15.

McNamara also notes Sterling has also returned to the top of its range relative to the Dollar – Thursday’s closing level was £1.4225, which is just fractionally below the 19-month high that was recorded back in early February (when it topped out at $1.4264).

Meanwhile, a note out from Viraj Patel at ING says the risks are that their EUR/GBP year-end target of 0.85 is met much earlier. EUR/GBP gives a GBP/EUR exchange rate target at 1.1765.

"While one may be inclined to chalk down GBP’s bullish bias of late to seasonal factors, we’ve also been noting how 2018 is very much a different Brexit trading environment for the pound," explains Patel, adding:

"Gone are the days of noisy Brexit headlines stirring sharp – and almost sentimental rather than fundamental – knee-jerk moves in the currency, with the buffer of last month’s Brexit transition deal buying GBP investors some extra time to assess the Brexit facts."

The positive outcome of the March EU summit helped calm markets with regards to Sterling and allowed the political debate to settle for now, but analysts warn the Brexit climate will probably heat-up again soon as trade negotiations between the UK and the EU are set to intensify during the summer.

We note that there is no shortage of analysts out there warning that Sterling might suffer Brexit-related jitters again in the medium-term.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

Euro Weakness is Key Near-Term Driver

We note the combination of a benign Brexit environment and broad-based Euro selling are playing a part in helping Sterling move higher against its European counterpart.

The Euro was sold on the back of some disappointing data out of the Eurozone on Thursday, April 12 where industrial production grew 2.9% on an annualised basis according to Eurostat; markets were optimistic in looking for a reading of 3.8%.

The monthly data actually signalled contraction with the February reading coming in at -0.8%, worse than the 0.1% forecast by markets.

The data tells us that the period of consensus-busting Eurozone economic growth might now be over; indeed it was this consensus-busting pace of growth seen during 2017 that really saw the Euro catch a bid over the course of the year.

This slowing in data is consistent with data releases elsewhere and suggestive that the Eurozone is entering a period of slower growth.

The European Central Bank added to the soft Euro tone with the scheduled release of the Account of the Monetary Policy Meeting held in Frankfurt on 7-8 March, which suggested to markets that there is no guarantee the ECB will turn off the printing presses in 2018.

It is the assumption that the ECB will exit its Asset Purchase Programme (aka quantitative easing, money printing) in 2018 that saw the Euro appreciate markedly during 2017.

The ECB's governing council were in broad agreement that there was not enough evidence that inflation is sustained in the Euro area while expressing "widespread concern" over risk of trade conflicts and noting global economic risks are tilted to the downside. This suggests the Bank is in no rush to bring forward the cessation of its quantitative easing programme, tipped to end around September 2018.

Any delay to the end date would certainly hamper the single currency and open the door to further gains by Sterling.

The ECB's Governing Council members also flagged the common currency's 2018 rally as a source of concern for the ECB in a much more pronounced fashion than before, citing it as a material risk to their inflation and economic growth forecasts which could ultimately end up threatening the central bank's ambition to wind down its quantitative easing (bond buying) program later this year.

"It was remarked that recent movements in the euro exchange rate seemed to relate more to relative monetary policy shocks, including communication, and less to improvements in the macroeconomic outlook for the euro area. This suggested that the exchange rate appreciation could be expected to have a more negative impact on inflation," the ECB says.

This suggests to us that concerns over the value of the Euro could be a reason unto itself for the ECB to engage policy decisions that in turn curb the Euro's value.

"We are pushing out the end of net APP from September 2018 until December 2018," says Philippe Gudin at Barclays. "The ECB would then pause for roughly six months and in June 2019 would deliver a DFR hike of +15bp. Then, in Q4 19, we forecast a DFR and a MRO hike of +25bp each, effectively removing negative rates by end of 2019."

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.