The British Pound found relief and defended its recently-established floors against the Euro and Dollar following surprising comments concerning the need for a future rise in UK interest rates from a key Bank of England member on Wednesday, June 21.

The Bank of England's Chief Economist Andy Haldane said in a speech that he expects to vote for an interest rate rise soon; comments that saw the Pound recover from multi-day lows against both the Euro and Dollar.

The comments are significant in that Haldane is seen as one of the more conservative members of the BoE when it comes to interest rate rises.

"I think that the balance of risks associated with tightening 'too early', on the one hand, and 'too late', on the other, has swung materially towards the latter in the past six to nine months," says Haldane.

The speech comes just a day after the Pound fell in response to the Bank of England Governor saying he felt no interest rate rise was needed in the near future.

Haldane noted just how resillient the UK economy was proving in the face of Brexit uncertainty and that economic growth was shifting away from consumer spending towards exports and business investment as businesses put their substantial balance sheets to work.

"Even if the two sets of speeches do not necessarily contradict each other, it does on the surface suggest an increasingly split board on how to look at the latest uptick in inflation. With a divided board, each board member potentially becomes more pivotal and hence our call for a BoE on hold throughout the Brexit negotiations is increasingly becoming at risk," says Danske Bank Chief Analyst, Jakob Ekholdt Christensen..

Haldane argued a 0.25% interest rate rise must be placed in context - the cost of borrowing on financial markets would still be cheaper following such a move than it was during the same period last year before the Bank cut rates following the Brexit vote.

Thus Haldane is not necessarily arguing for an interest rate raising cycle, rather a reversal of 2016's cut. This could explain why there has been little upside follow-through in Sterling.

What we have here is open discussion about higher interest rates at the Bank and a breaking down in consensus that interest rates should stay lower for an extended period of time.

Higher interest rates make for a stronger currency as they tend to attract capital from global investors seeking out higher returns on their capital.

It would appear that for now the Pound will follow developments at the Bank of England closesly.

"Bank of England developments have generated significant volatility for the GBP in the past week, even if ultimately EUR/GBP is more or less where it was a week ago," says Shahab Jalinoos at Credit Suisse.

The BoE rate decision in mid-June delviered a shock 5-3 vote outcome, with two other external members of the MPC joining long-time hawk Kristen Forbes in voting for a rate hike.

This led to a gap higher in GBP, reflecting the market being taken by surprise by the idea that a significant number of MPC members saw enough inflationary pressure to vote for a hike despite the patchy growth data, weak wage numbers and threat to investment posed by the onset of Brexit negotiations.

The big question now surrounds Silvana Tenreyro, who replaces the departing Kristen Forbes ahead of the next Monetary Policy Committee meeting in August.

“If she picks up where the hawkish Forbes left off, and Haldane votes in line with the contents of his speech, the central bank could be looking at a 4-4 summer split. If not then Carney may continue to get his way until the end of the year and beyond,” says Campbell.

Relief for the Pound Against the Euro was to be Expected

Ahead of the Haldane comments we briefed readers with the view that there could be some relief in store for those who need a stronger Pound to buy Euros and Dollars, but beware the moment could be fleeting.

The Pound to Euro exchange rate (GBP/EUR) has reached the bottom of a range between 1.13 and 1.20 within which it has been trading all year suggest our latest technical studies.

Whilst it is expected to find it difficult to break below the floor there are few signs of price action reversing yet.

Technical studies rely on previous price action to ascertain the structure of the market as this gives great clues as to potential future behaviour.

The mini-downtrend from the 1.20 April highs is still intact and therefore capable of breaking lower, and entering the fresh pastures below 1.13.

And whilst it may seem unlikely, a break below 1.1275 would probably confirm a breakout from the range and a move lower to an initial target at 1.1200.

The MACD is not signalling further downside, however, and the little pattern it has formed at the cycle lows (circled) is a bullish reversal pattern on an indicator, suggesting a reversal of that indicator, and therefore the actual exchange rate too.

We would want to see a break above the trendline of the mini-down-move for greater confirmation of a reversal of the trend, however.

Given the trendline remains intact it is too early to speculate about such a reversal.

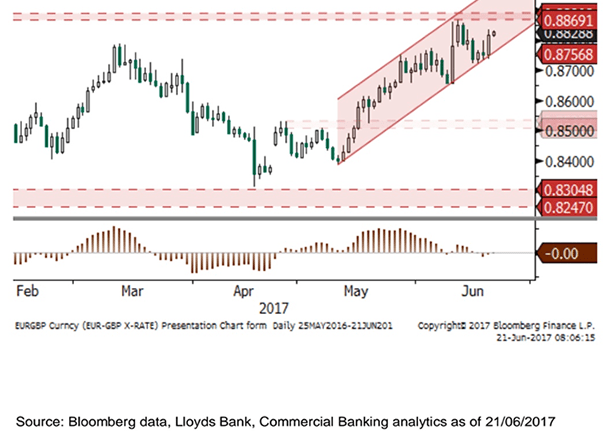

The Euro Uptrend is Intact Longer-Term say Lloyds

Frustratingly for some readers, there is hardly ever consensus on where a given currency pair is going.

But observing timeframes is important in clearing up any potential confusion.

Technical analyst Robin Wilkin at Lloyds Bank had been expecting a deeper correction lower in EUR/GBP after seeing the 0.8850-0.8900 range highs hold. (Note we have flipped the anlysis from GBP/EUR to EUR/GBP).

“However, the 0.8730/20 region of support has held and we are bouncing back towards that resistance region,” notes the analyst in a briefing to his commercial banking clients on June 21.

Wilkin says his studies still suggest the upside should be limited to the range highs, but a clear break of 0.8850-0.8900 would likely see a shift to 0.9000, with more important resistance above there at 0.9175-0.9200.

“A drop back through 0.8750/20 would again signal that range highs have held for a deeper decline, with further support for that view coming from a break of 0.8680,” says the analyst.

Long term, it is still unclear to Lloyds whether the decline from the “flash-crash” highs at 0.9710 are just corrective, for an eventual re-test of the 2008 highs at 0.9802, or a major lower high for a move back towards 0.7500-0.7000 range lows.

They have been highlighting 0.8250 as key support in determining this outcome.

Pound Could Rise in the Short-term on Positive Politics

Keep an eye on headlines - we get the sense that the Pound has absorbed a huge portion of negativity concerning politics, and some relief should surely be found.

Analysts at Credit Agricole also see the Pound rising in the short-term on this basis.

According to London-based analyst at the French bank, the ambiguous election result means there is now more chance of the Tories reaching out across the ‘divide’ and agreeing a ‘soft’ Brexit.

“The election outcome may reduce the risk of a very hard Brexit. Indeed, given their weakened position in parliament, investors expect the Tories to reach out across the divide when devising their Brexit strategy. This seems consistent with recent comments by some key members of the Brexit negotiation team,” says Credit Agricole analyst Valentin Marinov.

Another theme expressed in the ambivalent election result is the rejection of austerity by voters, which could also be supportive of GBP.

“Some clients seem to believe that the election may lead to a period of a relatively lax fiscal stance that could help support the recovery at a time of heightened uncertainty about Brexit,” says Marinov.

The greater fiscal looseness would be supportive of Sterling via increased consumer spending and economic growth.

We believe any relief in GBP will not last long, however, as deteriorating UK economic data is likely to undermine the currency.

Indeed, we saw the Pound fall notably on Tuesday, June 20 after Bank of England Governor Mark Carney told an audience that now is not the time to raise UK interest rates.

The Pound fell half a percent against the Euro on the viewpoint being made clear.

Euro Risks: Inflation

Another potential factor to consider going forward is Eurozone inflation.

Research from ABN Amro Bank suggests Eurozone inflation is likely to fall faster than members of the European Central Bank are currently anticipating, which is problematic for those hoping for a stronger single-currency.

“We continue to expect core inflation to undershoot the what is expected in the ECB’s Staff Macroeconomic projections,” says Nick Kounis at ABN AMRO Bank in Amsterdam in a recent research note. “Indeed, we are actually somewhat downgrading our view of core inflation from the already weak profile we had earlier.”

This suggests to Kounis that there is more slack in the labour market, which will keep wage growth depressed for longer.

ABN AMRO expect Eurozone core inflation to average 0.9% in 2017 and 1.1% in 2018. This compared to the staff forecasts of 1.1% and 1.4% for those years, respectively.

It is a two-edged outcome for the Euro: on the one hand inflation is falling faster than the ECB is expecting and therefore hints at policy staying unchanged, which could potentially see some of the currency's gains undone.

On the other, the ECB appears to be running out of bonds to buy under its quantitative easing (QE) programme and could therefore have to tighten policy regardless of inflation.

This will certainly be a topic to watch over the remainder of 2017 as it could weigh significantly on the single currency.