Pound Sterling has put in a stellar performance as traders realise the currency has been left undervalued according to its relationship with global bond yield differentials.

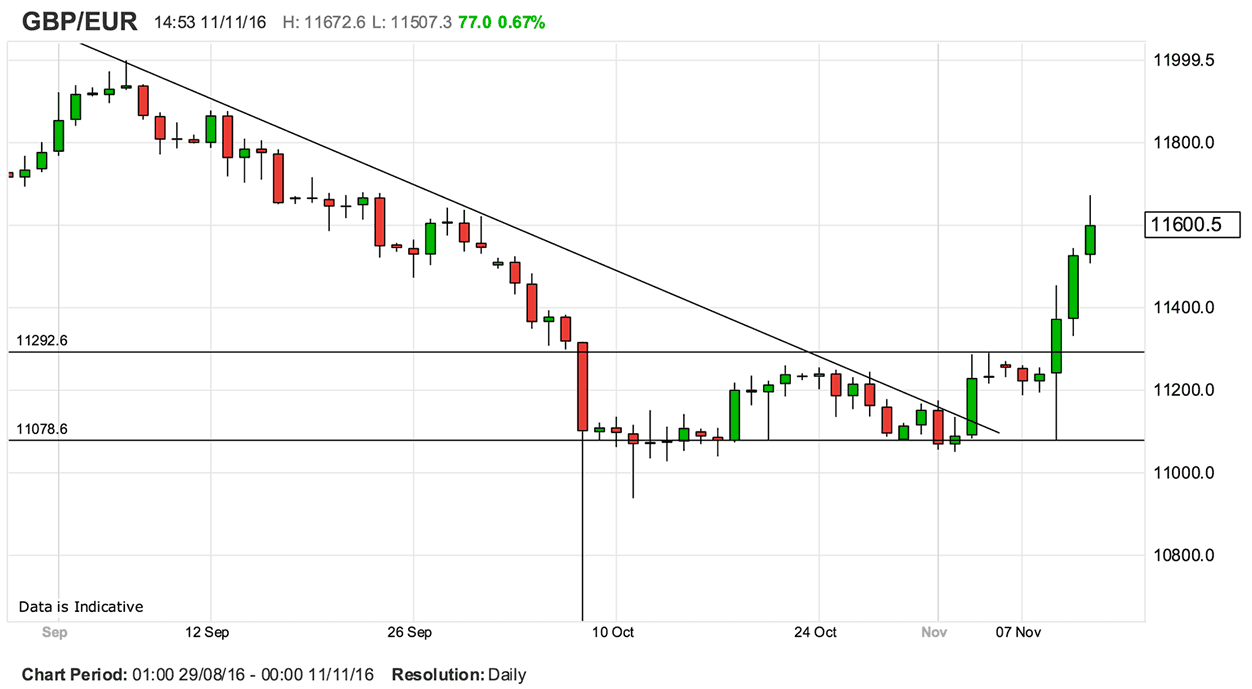

The GBP/EUR has rallied from the week's low at 1.1079 to hit a fresh multi-week best at 1.1672 on Friday October 11th.

This constitutes the pair's strongest two-week run since 2008.

“The only currency in our sample that beat the mighty USD this week was sterling, thanks a combination of continued short covering and some speculation about the UK's improved Brexit negotiating position with a potential US downgrading of its NATO commitments,” says Alvin Tan, analyst with Societe Generale in London.

The Euro struggled in this environment with the currency not only underperforming the Pound but also the US Dollar with EUR/USD sliding 2.5%.

GBP/EUR has broken the resistance area given around 1.1290 (04/11/2016 high) which Strategist Yann Quelenn at Swissqote Bank tells us constitutes the kind of break-out that invites further advances as momentum shifts from down to up for the pair which has been under pressure since November 2015.

Quelenn says he is bullish on Sterling in the near-term and is looking for further advances.

Support is seen at 1.1053, which is the 30/10/2016 low, and therefore suggests the pair is unlikely to embark on a major decline in the current environment.

Robin Wilkin at Lloyds Bank Commercial Banking says he believes support for the Pound to Euro exchange rate should be offered by the 1.1280-1.1299 region.

This was the former resistance that the pair smashed through in reaction to the foreign exchange market’s recalibration of the financial landscape following Trump’s victory.

A fall back through this interim support would reduce the immediate bullish bias and leave us back in a range environment for now.

Wilkin says while above this region we can see the market grinding higher towards next resistances in the 1.1507 - 1.2747 region.

However, longer-term Lloyds are wary that another move to test the 1.02 lows set back in 2008 can’t be ruled out and they are monitoring medium-term price action to confirm whether this will be the case, or whether 1/0309 was a higher low within a broad range.

Quelenn agrees with the notion that the longer-term picture remains unconstructive for the UK currency.

As such, those with a longer-term view, that spans many months, should note that the technical structure actually suggests a growing downside momentum.

The pair is trading far below its 200 day moving average and strong support is to only be found at the 1.0526 psychological level notes Quelenn.

It is only here that the analyst would expect the long-term decline to fade.

Therefore, those with the luxury to wait for a stronger Euro are best served by sitting back and waiting for the currency’s dominance to reassert itself.

A word of caution though as some analysts believe this global dynamic driving the Pound higher against the Euro is not guaranteed to last.

Iin the opinion of Piet Philip Christiansen, Rates Strategist at Nordea Markets the post-Trump market reaction is overdone and rates will revert in the near-future, in particular in the Euroarea.

"That said it’s important to note that the risk-reward of such positions doesn’t look intriguing at current levels, so we prefer to stay side-lined until markets have calmed down before re-entering long positions," says Christiansen.

Latest Pound/Euro Exchange Rates

| Live: 1.1704▲ + 0.03%12 Month Best:1.1828 |

*Your Bank's Retail Rate

| 1.1306 - 1.1353 |

**Independent Specialist | 1.154 - 1.1587 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Pound Chases Rising Bond Yields

Expectations for higher inflation in the developed world since Trump won the US election have gripped financial markets.

The yield delivered on long-dated government bonds has been the stand-out story of the financial market place as investors demand a greater premium for owning bonds that could be at risk of higher inflation in coming years.

The resultant surge in yields paid on government debt has seen a massive flow of funds into the UK from Europe, the United States and the developing world which has in turn seen the Pound bid higher.

And it's about time too.

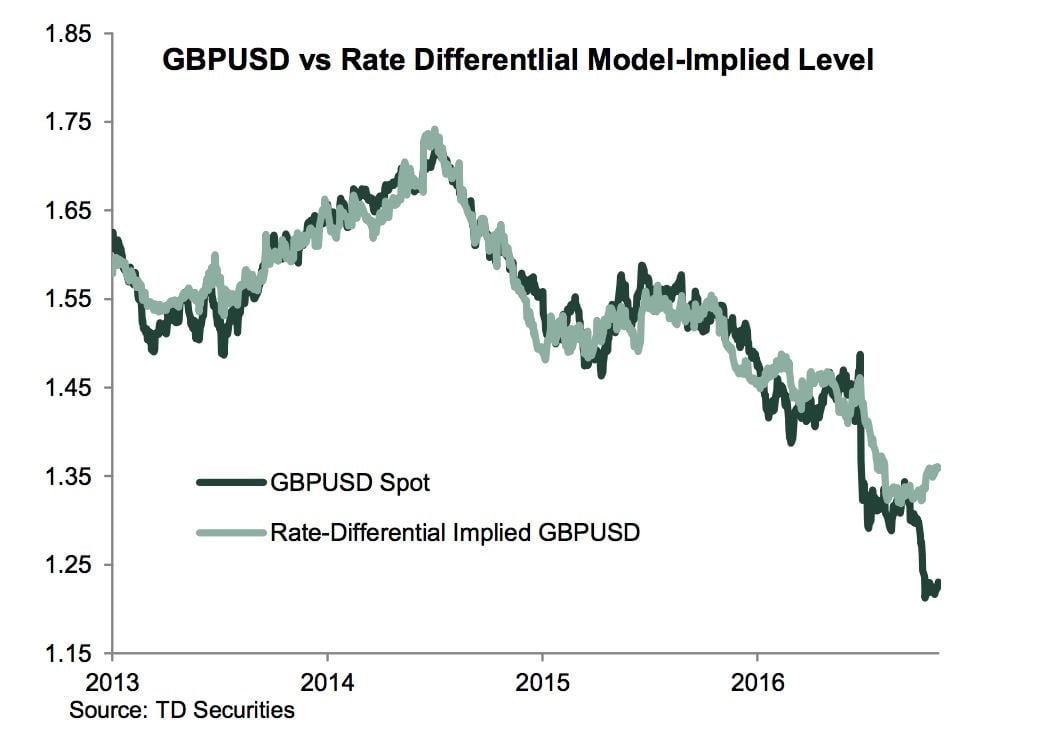

Something strange has happened in the Sterling foreign exchange market place since the Brexit vote - the currency has broken away from tracking the difference between the UK's government bond yields and that of foreign bond yields.

UK government bonds and the yield they deliver to global investors is arguably the single most important driver of currency rates over the medium- to long-term.

More specifically, the currency tracks the difference between its domestic yields and that of foreign yields.

Look at the following graph showing how GBP/USD follows rate differentials between the US and UK:

The startling observation to be made with the above is that recently Sterling has broken away from yield differentials as markets went into a panic over Brexit, making Sterling incredibly undervalued.

The same undervaluation is observable in the GBP/EUR complex.

We have been warning for some time that Sterling must soon play catch-up and snap back higher to fulfil its long-term relationship with Gilt yields.

What has happened since Donald Trump won the US Presidential Election is markets have suddenly refocussed their attention on yield differentials and taken note of Sterling's undervaluation on this metric.

The Great Trump Reflation

Pound Sterling apparently likes the new post-Trump victory financial landscape, particularly when it comes to trading against the Euro.

The global financial market place has suddenly priced in higher inflation now that Trump has ascended to the US Presidency as a result of his promise to massively boost public spending and cut taxes.

The UK 10-year break-even rate, a measure of expectations for retail prices derived from government bond yields, rose to the highest in almost three years.

Importantly the dynamic applies to Europe as much as it does to the US.

The promise of a gargantuan surge in money supply will inevitably push up inflation which in turn requires central banks to raise interest rates.

And rising interest rates = higher currencies.

The rise in US Treasuries is dragging UK Gilts higher in sympathy and the Pound is pushing higher to close the differential gap.

Better Brexit

Markets also like the idea that Trump is the best option for the UK when it comes to negotiating post-Brexit trade deals.

Trump does not like bloc deals and prefers bilateral agreements and some are betting a UK-US agreement would be first on the agenda.

"I think the pound could be particularly positive on a Trump presidency because he has warmly extended the hand of friendship to Theresa May and wants to see her first when he actually takes up the Presidency in Jan," says Kathleen Brooks at City Index.

"This opens the door to an earlier trade deal with the US, compared to what Obama offered, which could make our economic prospects outside of the EU much brighter.

Softer Outlook for the Euro as German Growth Likely to Disappoint

What about the Euro side of the GBP/EUR equation?

Fresh research from Germany's Commerzbank suggests the Eurozone should start to capture investor attention once again with Q3 growth in Germany likely to disappoint.

“While the outlook for Q4 has improved of late, the economic balance for Q3 should turn out rather weak. We expect that the German economy grew by only 0.2% on the preceding quarter, which would mean that the growth rate was the slowest since last year. The Federal Statistical Office will only release the details in the week after next,” said Commerzbank’s Ralph Solvene.

Another major drag on the single currency is likely to come from increasing political risk, as markets start to price in the possibility of further political instability in the Eurozone.

The Brexit vote and Trump win have seen many analysts start to price in potential anti-establishment outcomes in looming European votes.

A referendum in Italy may cause an upset and see the Five Star anti-EU party gain a foothold, however, the main threat at the moment comes from the Netherlands in March where Geert Wilders vehemently anti-EU party is leading polls on a ticket to take the country out of the EU with immediate effect.

The GBP/EUR is forecast to move remain stable by Commerzbank who see the pair trading in a range between 1.1737 and 1.1363.