Pound Sterling hit an impressive multi-week high against the Euro in the wake of Donald Trump's victory and we believe further advances are possible.

- British Pound to Euro exchange rate today: 1.1371, 24-hour best rate: 1.1454, 24-hour low: 1.1079

- Euro to Pound Sterling exchange rate: 0.8793, 24-hour best: 0.9025, 24-hour low: 0.8762

Donald Trump is the new President-elect of the United States who will govern alongside a Republican majority in congress.

The news came as something of a shock to foreign exchange markets which had been pricing an Hillary Clinton victory.

The uncertainty triggered a massive sell-off in global stock markets, commodities, the Dollar and commodity Dollars in what looked to be a repeat of the reaction to June's Brexit vote.

The Euro enjoyed strong gains as is usually the case when stocks fall as it is a major funding currency of US stock markets.

However, an impressive reversal then took place with markets having a change of heart it would seem.

The S&P 500 embarked on it's largest reversal since 2008 and the Euro was punished as a result.

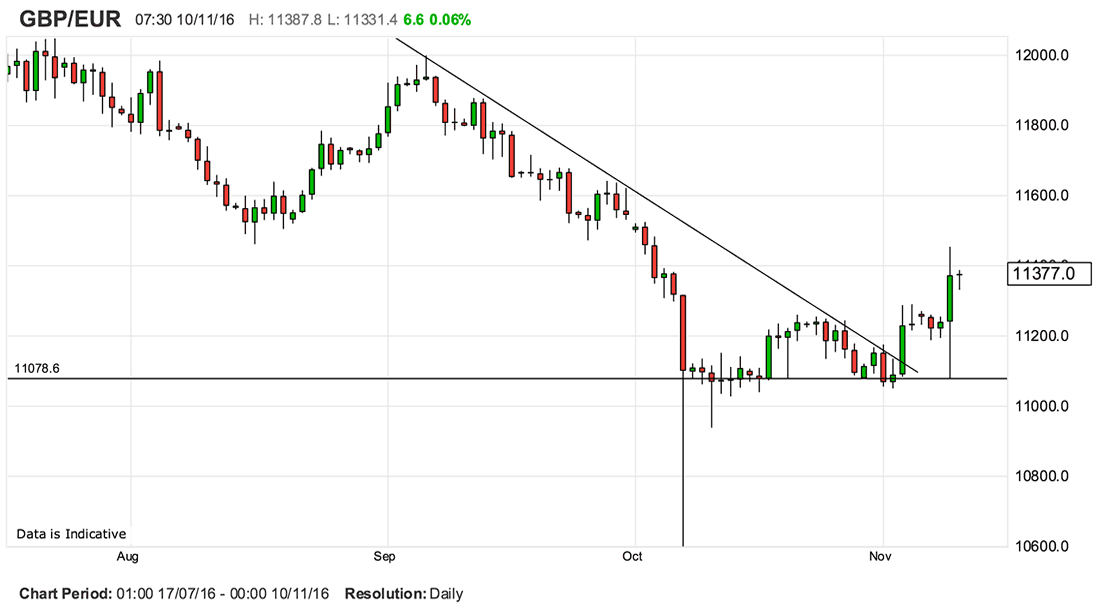

GBP/EUR found support at the old faithful 1.1080 area and rallied strongly on the Euro's demise:

Looking ahead we expect 1.1080 to remain the key support level for GBP/EUR and any weakness should be limited by this point.

The break above the downward-sloping trend line is also suggestive further advanes are possible as momentum turns positive.

The recovery should extend we believe.

Latest Pound/Euro Exchange Rates

| Live: 1.1705▲ + 0.27%12 Month Best:1.1828 |

*Your Bank's Retail Rate

| 1.1307 - 1.1354 |

**Independent Specialist | 1.1541 - 1.1588 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Why Did Markets Change Their Mind About Trump?

One reason for the sudden reversal in financial markets is actually the similarities between the election outcome and Brexit.

"We believe investors feel like they have seen this movie before and have been eager to take advantage of any exaggerated sell-off as an entry point for longs. As a result, we ex-pect the fall in prices to be rather mild with very few trades both on the way out as well as on the way in," says Christian Schwarz at Mizuho in London.

Aurelija Augulyte at Nordea Markets also believes the pullback we have seen from the initial move proves markets have learned from Brexit and enacted a faster reversal.

The market has also adopted the opinion that a Trump presidency could actually benefit US economic growth going forward thanks to an assured speech given by the President-elect following his victory.

Watch: Trump's first speech promises massive spending on infrastructure upgrades:

Of note is that Trump may embark on a Regan-like fiscal stimulus with the promise to spend $550BN on infrastructure spending.

Whether Congress allows such a splurge remains to be seen, but we can expect some type of stimulus that will add some handy figures to US GDP.

Note too that Trump ran on a ticket that promised massive tax breaks, particularly corporate tax breaks.

This could further provide a stimulatory effect that will support stock markets going forward and potentially undermine the Euro.

US Interest Rate Rise in December Still Likely

The big deal for the US Dollar, and thus the Euro and Pound Sterling, over coming weeks is the debate over whether the US Federal Reserve will raise interest rates in December.

The Trump victory saw markets suddenly decide the Fed would shy away from the cut.

However, the prospect of a rise is back on following the impressive turnaround in stock markets.

Analysts believe that the Fed would only skip a December hike were financial markets become disorderly following the Trump victory, which appear to not be the case.

The Dollar rose as the rate rise was factored back in.

Pound to Dollar Upside Limited as Fed Tipped to Raise Rates in December

"We expect the Fed to deliver a hike in December, as the economic data have been indicating. Furthermore, we believe the Fed has no interest at all to become politically tainted by refraining to hike as a result of the US election. Of course, this is contingent on the sell-off being rather mild and short-lived," says Christian Schwarz at Mizuho in London.

Drew T. Matus at UBS agrees:

"We continue to expect the Fed to move rates higher in December. The odds are lower as uncertainty is higher, but the near-term impacts on growth and inflation are small absent a sustained financial market shock. Any risk to the Fed outlook is to the path of policy in 2017 and 2018.

This will likely ensure the Euro remains under pressure over the short-term which will naturally feed into moves in the GBP/EUR cross rate.

The October-November recovery in Sterling could therefore extend.

Trump Good for the Dollar Long-Term

The initial knee-jerk reaction to sell the USD was expected but now comes the hard part - deciphering impending currency moves.

Greg Anderson, Global Head of FX Strategy at BMO Capital believes the Dollar should benefit from a Trump presidency owing to his stances on tax, and his ability to appoint the next US Fed Governor:

"Trump’s proposed re-write of the US tax code could bring a big shift in USD fundamentals. Reducing US corporate taxes and closing loopholes has the potential to dramatically alter the competitiveness of American business and therefore the long-run equilibrium of the dollar.

"Without knowing all the details on the loophole closures, it’s hard to be definitive, but we (BMO FX Strategy) tend to view corporate tax reform as long-run positive for the USD."

"The President nominates appointees to the Fed’s Board of Governors as openings occur. The next President will nominate the successor to Janet Yellen as Fed Chairman when her term expires in January 2018. Trump would appoint mostly Republicans, who tend to be more hawkish than Democrats, although there isn’t a perfect mapping of that issue.

"The Fed’s rate path in 2017 probably wouldn’t be different under Trump, but over the span of several years, a FOMC that is gradually staffed with more hawkish members would likely to result in higher Fed base rates. This would be a USD-positive factor during the period the rates market priced it into forward curves."