Analysts at Lloyds Bank have lowered their estimates for Pound Sterling's future levels but maintain expectations for a recovery.

- Pound to Euro exchange rate today (15-10-16): 1.1111

- Euro to Pound Sterling exchange rate today: 0.9003

The outlook for Sterling remains challenging with one of the UK’s largest high-street lenders announcing a cut to their forecasts for the currency.

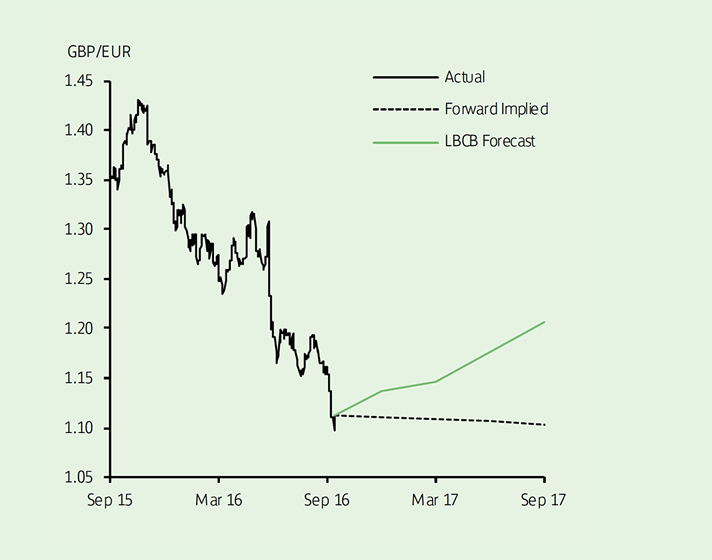

Lloyds Bank have rowed back on previous estimates for the British Pound which had the GBP to EUR exchange rate ending 2016 at 1.18.

The October slump in the UK currency has all but made such a recovery unachievable it would appear.

The pound underperformed all other major currencies over the past month and, at one point, plunged below $1.15 for the first time since 1985.

It also fell briefly under €1.10.

The general decline seems to have been spearheaded by confirmation that the UK will go ahead with EU withdrawal and market perceptions of an increased risk of what has been widely reported, if not precisely defined, as a ‘hard Brexit’.

“We have revised down our forecasts for the Pound, following confirmation that Article 50 will be triggered early next year and fears of a so-called hard-Brexit,” say Lloyds in the latest edition of their International Financial Outlook publication.

British Pound Recovery Through 2017, ECB to Undermine the Euro

While the forecast targets have been slashed Lloyds still maintain the currency will recover through 2017.

The tone of key cabinet members - including PM Theresa May, who relayed her intention to trigger Article 50 by the end of Q1 2017 - alerted markets to the possibility of a hard-Brexit.

However, “persistent GBP weakness is out-of-line with recent data, which suggest that the UK economy is outperforming market expectations,” say Lloyds.

The move lower in GBP/EUR has been further compounded by a scaling back in expectations of additional easing by the European Central Bank (ECB), following recent suggestions of a potential tapering of QE.

However, it would be wrong to believe the ECB is done:

“Given that Euro area inflation is expected to remain below the 2% target for the foreseeable future, this seems unlikely.

“In fact, we suspect ECB President Draghi will announce a six-month extension to the programme at December’s policy meeting.”

Latest Pound/Euro Exchange Rates

| Live: 1.1717▲ + 0.12%12 Month Best:1.1828 |

*Your Bank's Retail Rate

| 1.1319 - 1.1365 |

**Independent Specialist | 1.1553 - 1.16 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

This suggests to Lloyds that the ECB’s balance sheet will continue to expand at a more rapid pace than that of the Bank of England.

On a relative basis, this argues for a higher GBP/EUR as expanding balance sheets tend to weigh on a currency.

That said, analysts also do expect the Bank of England to cut interest rates again to 0.1% at the 3 November meeting.

"But we acknowledge that it is a close call and that the risk of no change has risen," say Lloyds.

An inactive BoE would certainly aid Sterling but another cut would certainly undermined the expectation for a rebound, particularly if markets were seen to be discounting such a move.

“While in the near term, GBP/EUR remains susceptible to further bouts of volatility, we see scope for the pair to drift towards 1.18 by mid-2017,” say Lloyds.

Lloyds say they now predict the GBP/USD exchange rate at 1.25 (1.30 previously) at end 2016 and 1.30 (1.36 previously) at the end of 2017.

For the equivalent periods, GBP/EUR has also been revised down to 1.14 (from 1.18) and 1.21 (from 1.27).

End of Another Dismal Week for Sterling

GBP was the second-worst-performing currency in the G10 space for the week ending 14th October.

"The Swedish Krona is the weakest of the G10 currencies this week - knocking the pound off its dismal perch for once," notes Kit Juckes at Societe Generale in a brief to clients, "GBP's fall may be eclipsed by the SEK move, but the pound has fallen by twice as much as any other major currency over the last month."

The near-term outlook for the currency is unlikely to improve as markets keep a nervous eye on news headlines as the UK currency has become almost exclusively sentiment driven.

The Bank of England's Governor Carney didn't help matters on Friday the 14th with his comments that the Bank is willing to allow inflation to overshoot the 2% level targetted by the Bank.

Typically, rising inflation would prompt the Bank to raise interest rates as this tends to stem price pressure.

An side effect of higher rates is a stronger Sterling.

However, the suggestion that rates will stay lower-for-longer despite rising inflation offers very little support to those hoping for a recovery in the Pound.

The Pound has become increasingly sentiment-driven since Prime Minister May fired the starting gun on triggering Article 50 in March 2017.

Latest developments that will keep markets wary of bidding Sterling higher includes news that the President of the European Council Donald Tusk told an audience that Britain has a binary choice between no Brexit or a hard-Brexit.

What this suggests is that the trade deal reached with Europe following Brexit will be worse than the current relationship.

It also confirms upcoming negotiations are going to be incredibly tough and it's hard to see Sterling staging any major recovery.

Also weighing on sentiment is the legal challenge to the Government’s right to trigger article 50 by bypassing Parliament at the High Court.

If the court sides with the claimants and overturns May’s decision we would expect some movement in Sterling.

Whether it is lower on increased uncertainty, or higher on the assumption that perhaps Article 50 is not triggered at all, is hard to call at this stage.