Pound Sterling is forecast to fall further against the Euro over the course of the next year but the decline will not be as deep as previously envisaged by foreign exchange analysts at JP Morgan.

- Analysts say GBP to continue falling as economic relief to be limited

- Bank of England to cut rates again

- Pound to Euro exchange rate today (14/9/16): 1.1760

- Euro to Pound Sterling exchange rate today (14/9/16): 0.8504

GBP's August-September rally appears to have been decisively decapitated at the 1.20 level against the Euro with investors apparently unwilling to take the UK currency above this level.

It would seem that the big theme for the currency over coming months remains the intentions of the Bank of England - will they cut interest rates again in November? If they do, then we would not expect any sustained strenght in the Pound until then.

What is needed is unequivocally strong data to suggest another rate rise is not warranted. As observed with the reaction to the subdued inflation data of the 13th of September any soft data will be punished.

Yet the positive reaction to the data releases of preceeding weeks suggest the Bank doesn't have a blank cheque to write on extending monetary stimulus.

Therefore, calling the outlook for GBP/EUR remains largely an interpretation of future policy actions at the Bank.

With this in mind, the world’s largest investment bank, JP Morgan, have raised their profile for Pound Sterling having noted UK economic growth has been more resilient than initially anticipated in the aftermath of the Brexit vote.

The resultant data put a squeeze on the record 'short' GBP positions held by traders looking to profit on Sterling's decline.

Since mid-August we have seen a 4% rally in the GBP index.

GBP has now recovered one-quarter of its immediate post-vote losses and one-fifth of its peak-trough decline since last November, peak losses were 20% up to mid-August, reducing to 16% currently.

“We are upgrading our bearish forecasts for GBP but this is essentially a re-profiling to show a less abrupt downtrend without changing the end point very much,” says Paul Meggyesi at JPMorgan in London.

The forecasts for the rest of the year are raised by 3.5% - the year-end target for cable is raised from 1.28 to 1.32 and the target for EUR/GBP is cut from 0.90 to 0.87.

From a GBP into EUR perspective 0.90 = 1.110 and 0.87 = 1.1494.

The rolling 1Y forecasts are little changed for EUR/GBP - 0.90 versus 0.91 previously - and marginally higher for cable (1.33 from 1.30) to reflect the extended uptrend in EUR/USD to 1.20 in 3Q17.

EUR/GBP at 0.91 = 1.0989 in GBP/EUR terms.

Latest Pound/Euro Exchange Rates

| Live: 1.1715▲ + 0.1%12 Month Best:1.1719 |

*Your Bank's Retail Rate

| 1.1317 - 1.1364 |

**Independent Specialist | 1.1551 - 1.1598 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

However, it is worth pointing out that analysts continue to believe GBP is headed notably lower despite the upgrade to their forecast targets.

Hence the largely unchanged medium-term forecasts.

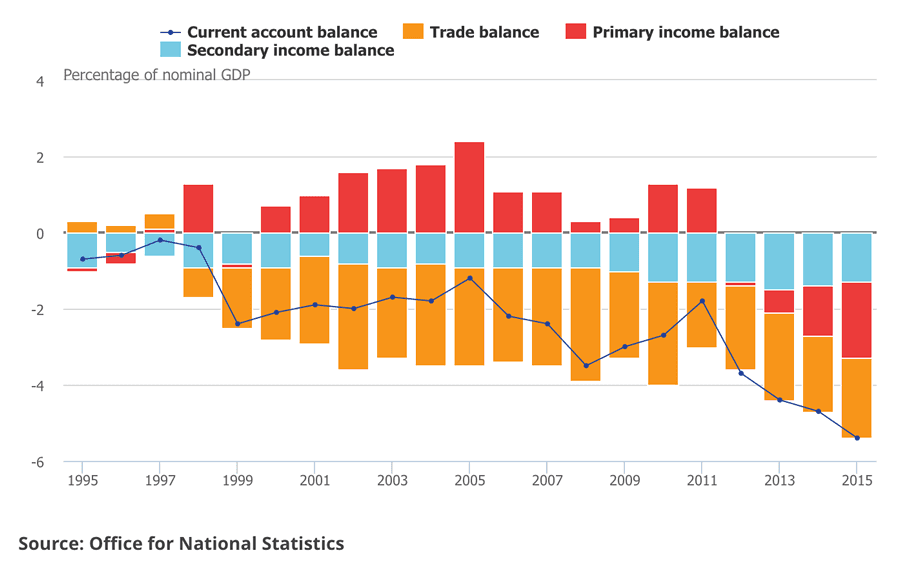

"GBP we believe faces enduring balance of payments strain/stress caused by an excessive current account deficit and an unfavourable investment climate. The current account is nudging 6% of GDP and whereas the entire deficit over the past five years was funded through FDI and equity inflows, the outlook for such inflows is less favourable post-Brexit," says Meggyesi.

Above: The Pound relies heavily on investor inflows to make up for the UK's notable current acount deficit. If these inflows were to weaken, notably on Brexit uncertainty, the currency would have to adjust notably lower.

JPMorgan also believe the Bank of England will be inclined to ease policy again even if the economy does grow as it expects by 0.5% in 2H.

GBP is considered cheap from a long-term perspective (JP Morgan note the Real Effective Exchange Rate is 17% below its 45Y average), albeit less undervalued on short-term interest rate models (the NEER is 1.5% undervalued).

"We expect it to cheapen further as investors demand a risk-premium to continuously fund the deficit during a multi-year period of structural economic uncertainty," says Meggyesi.

Euro Exchange Rates Seen Higher on 'Patient' ECB

Looking at the EUR side of the GBP/EUR pair, the sense is that strength in the shared currency is likely to persist owing to the European Central Bank's apparent satisfaction with their current policy settings.

JP Morgan's John Normand says he believes the Euro is biased higher over coming quarters courtesy of the Eurozone's current account surplus, and the risk of a sharp increase in German Bund yields on any hint of ECB tapering.

"This week’s ECB meeting confirmed our suspicion that the ECB is quite reluctant to provide additional easing, in turn preserving the risk of an eventual spike in yields that pushes the euro towards 1.20," says Normand in reference to their forecast for the EUR/USD pair which should in turn keep EUR/GBP elevated.