Pound Sterling was the worst performing currency in the G10 sphere for the week ending 6th of August, and analysts say further declines from here are to be expected.

- The British Pound to Euro exchange rate today: 1 GBP = 1.1792 EUR

- The Euro to Pound Sterling exchange rate today: 1 EUR = 0.8479

That GBP was the worst performing currency in the G10 complex over the week past thanks to the Bank of England monetary policy event of Thursday the 4th of August.

The underperformance came as an interest rate cut and a whopping increase to the Quantitative Easing programme were announced.

Analysts are in agreement that the Bank has taken a bold step in trying to get ahead of the curve and counter any economic weakness emnating from the Brexit vote.

The increase in supply of currency to the economy that the policy changes entail should have weakened Sterling notably.

Yet, the GBP/EUR is still above the 2016 lows and remains within the broader July-August ranges, suggesting that the event was not a knock-out blow for the UK currency:

The Pound to Dollar exchange rate trades at 1.3070, July’s low is at 1.2799, while the best is at 1.3481.

The Pound to Euro exchange rate trades at 1.1792, July’s low is at 1.1558, while the best is at 1.2120.

That we are well within recent ranges is understandable as markets are left with a quandary: Do they sell the GBP on expectations of an increased supply of money into the economy, whereby the unit value of Sterling is devalued, or, do they buy GBP on the basis that the Bank has initiated enough stimulus to save the economy from recession?

Indeed, “the extent of the MPC’s collective pessimism about the economic outlook appears relatively limited, at least after the supportive measures introduced today,” note Lloyds Bank Commercial in their initial response to the August measures.

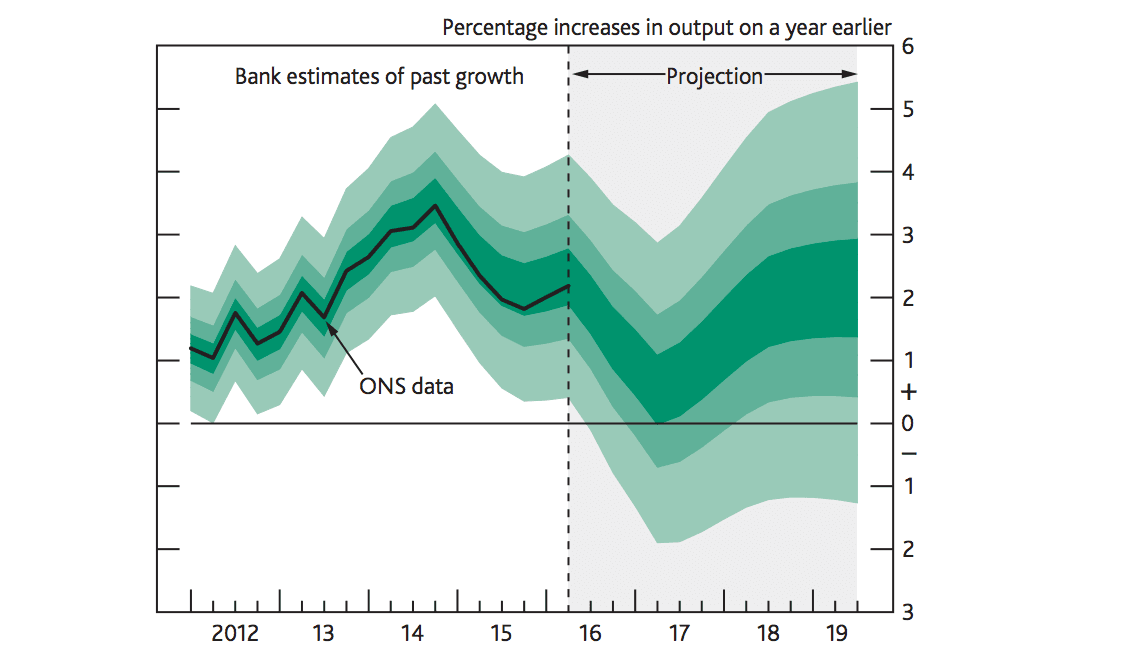

Importantly, the GDP forecasts released by the Bank confirm no UK recession is expected.

GDP growth throughout 2016 to 2018, on the MPC’s central estimates, is expected to be above post-referendum consensus expectations, and close to the recent optimistic forecasts of the IMF and NIESR, suggesting only a modest downturn.

Nevertheless, the prospect for surprises, either to the upside or downside, are notable with the Inflation Report’s GDP growth fancharts widening:

Above: The Bank of England's GDP forecasts based on assumptions that its new measures will behave according to plan. Note no recession is expected.

Despite the observation that the UK is not headed for recession it is far too early to call a bottom in Sterling.

Therefore, we find it comes as no surprise that the majority of forecasts for the UK unit point to lower values over coming months.

Yet, in line with the uptick in economic growth, a clear limit to the GBP's weakness is evident.

Latest Pound/Euro Exchange Rates

| Live: 1.1674▼ -0.01%12 Month Best:1.1828 |

*Your Bank's Retail Rate

| 1.1277 - 1.1324 |

**Independent Specialist | 1.1511 - 1.1557 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

The Best Bet: A Gradual Decline

We have become so used to volatile and whipsaw moves in GBP, since the EU referendum surprise, that we are conditioned for further rapid moves.

However, sobriety must set in at some point, and with that we should not be surprised if Sterling’s run lower is more pedestrian.

Indeed, this is the central scenario held by analysts at ING.

ING’s Viraj Patel says he is looking for a slow descent in the value of the GBP to EUR exchange rate.

“While we look for more GBP downside against EUR (3m EUR/GBP target: 0.88), we think any weakness will be orderly,” says Patel.

This implies a downside target in GBP to EUR terms at 1.1363 in three months.

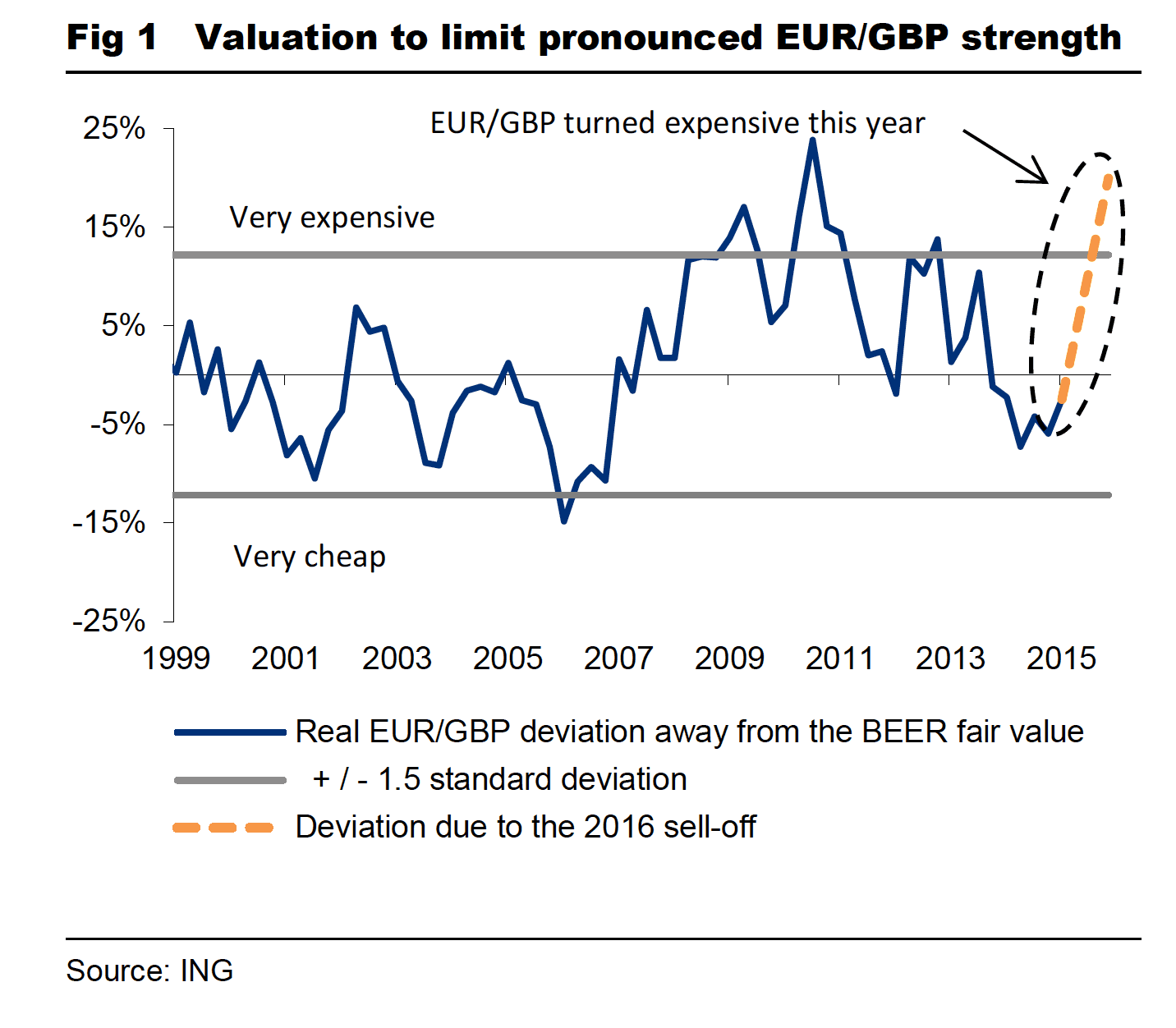

Patel notes that the Euro will be limited by already rich valuations:

The above studies imply that it will be relatively hard for the Euro to establish fresh impetus at such levels.

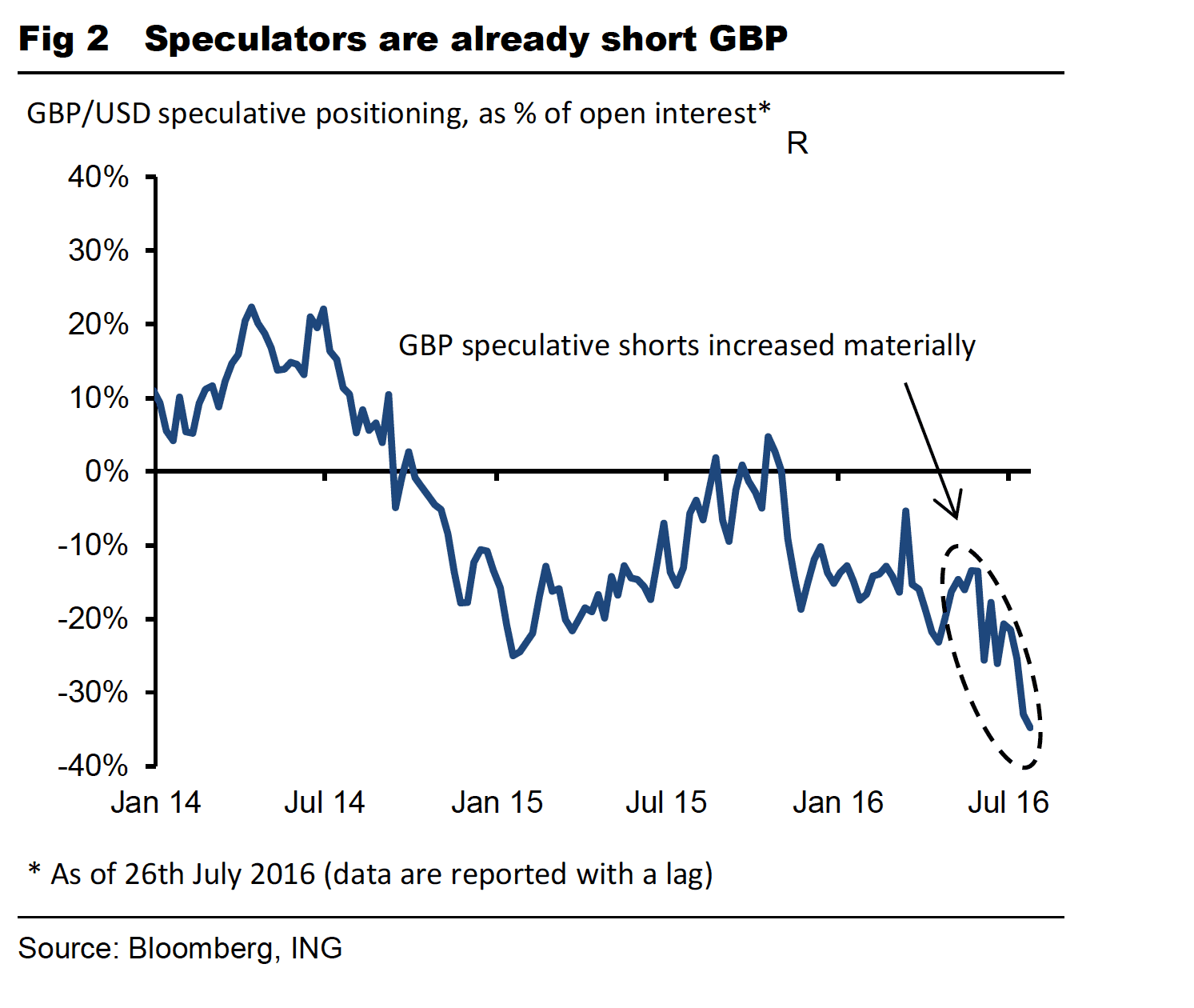

What is more, traders are already so heavily positioned against the Pound that it will be difficult to find the requisite volume of fresh market entrants to accelerate notable deterioration:

Also suggesting that we should not get overly excited by the prospect of a notably lower GBP exchange rate over coming months is Trevor Charsley, Senior Markets Advisor at AFEX.

The analyst reckons: "The logical conclusion is that we’re likely to see more Sterling weakness in the short and medium term with both GBP/USD and GBP/EUR having the potential to fall further than the lows seen immediately after the Brexit vote."

The low-to-date in the GBP/EUR is seen at 1.1594, recorded on the 6th of July.

However, other forecasters are a little more pessimistic on Sterling’s fortunes.

Over the next 3- to 12-months, Goldman Sachs say they are comfortable with their view that the slowdown in economic activity will drive the currency lower, they forecast £/$ at 1.20 and 1.25 and EUR/£ at 1.11 and 1.25 in 3- and 12-months, respectively.

Andy Scott, Economist at HiFX says:

"Against the Bank’s downwardly revised growth forecasts for growth and employment, the outlook for Sterling remains negative with risks to 1.25 versus the US Dollar and 1.10 versus the Euro."

With so much uncertainty lingering it goes without saying that the performance of the economic data over coming months will be key as to whether the pessimists are correct.

We need to know whether the initial post-referendum shock has translated into a more enduring trend, or whether it remains that - a mere shock.

The Bank’s decision to provide stimulus to the economy, by cutting interest rates, increasing its asset purchases and beginning a programme of corporate bond buying, will be welcomed by businesses suffering a decline in confidence.

However, a lot will now depend on how much heavy lifting the UK government is prepared to offer by way of fiscal stimulus.

"The Bank has gone further than simply cutting rates to stop any negative sentiment translating into a decline in business activity. While monetary policy is supportive, its capabilities appear to be stretched given rates are so low and QE has been in place for years. For this reason the government should remain poised to act if an economic slowdown still occurs over the coming months," says Lorence Nye, Economist at IPSE.

New research from Scandinavian lender Danske Bank also confirms further Euro appreciation against Pound Sterling over six months, but the limit to the strength would be reached after this timeframe.

Danske believe the BoE maintained a very dovish stance indicating a further rate cut later this year to the effective lower bound at above but close to zero.

The BoE also stressed that it can do more QE (both gilts and corporate bonds) if needed.

“We expect BoE to cut the Bank Rate by 15bp to 0.10% and to increase its buying of both gilts and corporate bonds at the November meeting,” says Danske Bank in a note to clients.

Analysts expect weak UK GDP growth, monetary policy and flows to weigh on the GBP in the coming quarters.

Danske forecast EUR/GBP to rise to 0.90 in 6M, this equates to a GBP into EUR rate at 1.110.

Longer term Danske expect EUR/GBP to stabilise to some extent given attractive valuations.

They target 0.88 in 12M, or 1.1363 in GBP/EUR terms.

GBP's Week Ahead

June’s Index of Production data forms the data event for the week starting 8th August.

The data covers the pre-Referendum period, so we don’t anticipate too much of a decline.

While markets are looking for a 0.1% decline, analysts at TD Securities see downside risks. This is notably weaker than the ONS’s +0.2% assumption in the Q2 GDP report, and could lead to a downward revision to growth that quarter.