Image © Adobe Stock

Is stronger-than-expected inflation now a negative for Euro exchange rates?

This could well be the case following a new set of Eurozone inflation data that showed ongoing price increases in the bloc alongside an unexpected increase in the region's unemployment rate.

"Resilient inflation and rising jobless – bad for the euro," says Jeremy Boulton, a Reuters market analyst.

Eurozone core CPI inflation rose to 5.6% year-on-year in February said Eurostat, surpassing estimates for 5.6% and December's 5.6%. CPI inflation rose 8.5% in the year to January, surpassing estimates for 8.2%, albeit coming in lower than December's 8.6%.

The region's unemployment rate meanwhile unexpectedly rose to 6.7%.

The Euro found itself at sea on the data:

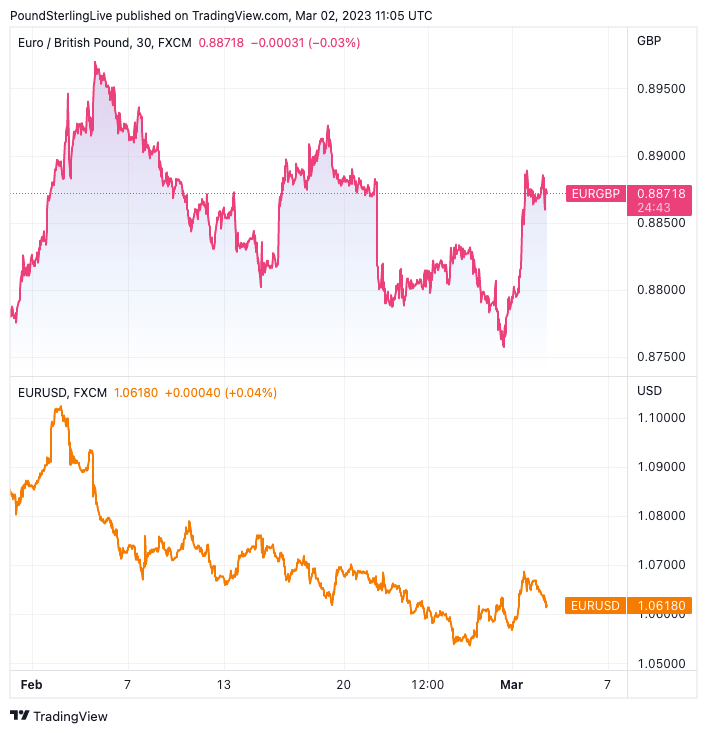

The Euro to Dollar exchange rate is now 0.702% down on the day at 1.0593, the Euro to Pound exchange rate has meanwhile relinquished earlier gains to go flat on the day to 0.8875. (Pound to Euro @ 1.1268).

Pound Sterling Live reported on March 01 the Euro rose on the back of German inflation data that was stronger than analysts were expecting.

The thinking is familiar: higher inflation will probe the European Central Bank into raising interest rates further, thus keeping Eurozone bond yields elevated which in turn creates the capital inflows that support the currency.

This was the narrative exercised on Wednesday after German inflation data followed Spain and France in printing at a stronger level than analysts were expecting, leading investors to bet on a more 'hawkish' ECB.

(It now looks increasingly the case that Wednesday's Euro strength was more a result of the market's near-euphoric response to China's strong PMI data, released earlier in the day.)

When Inflation is No Longer Supportive

It has been noted over recent months that strong inflation does not always result in a stronger currency, particularly in the case of the UK where the Pound has come under pressure despite elevated inflation levels.

Could this now be true for the Euro?

After all, if rising inflation leads to higher interest rates and deteriorating consumer strength, economic growth would inevitably come under pressure.

And if a currency's performance is ultimately a reflection of an economy's performance, then higher inflation is not necessarily a good thing.

"The FX market is more concerned about the implications of high inflation and interest rates for economic growth than it is reassured by the positive implications for carry," says Daragh Maher, Head of Research for the Americas at HSBC.

Above: EUR/GBP (top) and EUR/USD showing the Euro is no longer benefiting from the 'higher for longer' ECB interest rate story. (Consider setting a free FX rate alert here to better time your payment requirements.)

To be sure, it is stagflation that is typically cited as being unsupportive of a currency. This is a condition where inflation is elevated, unemployment is rising and the economy stalls.

Stagflationary concerns will have risen after the Eurozone's unemployment rate unexpectedly rose to 6.7% in January, whereas the market was preparing for a fall to 6.6%.

ECB President Lagarde meanwhile warned on Thursday that ECB interest-rate increases may need to continue beyond a planned half-point move in two weeks' time.

"At 0.5% month-on-month, core inflation is still growing at an annualised pace above 6%. So still nowhere near the ECB target for the moment," says Bert Colijn, Senior Economist for the Eurozone at ING Bank.

For now, it is too early to say with confidence that the Euro is set to lose altitude over fears of stagflationary conditions, as most economists still expect inflation to fall over the coming months.

(Colijn says forward-looking indicators show that the declining trend in inflation is set to continue. "March will show a much faster drop in headline inflation").

What is clear, however, is the Euro might prove less responsive to strong inflation readings and expectations for ever-higher ECB interest rates.

Therefore, further upside impetus to the currency from a now well-understood ECB interest rate story could be difficult to come by.